3% Is The New 2%

And that isn't a bad thing for the markets.

It’s a week where US inflation data takes the spotlight. So far, so good.

US producer prices rose less than forecast in July. This signals the first decline in services costs this year amid an ongoing moderation in inflationary pressures.

The producer price index (PPI) for final demand increased 0.1% from a month earlier. The median forecast in a Bloomberg survey of economists called for a 0.2% gain. Compared with a year ago, the PPI rose 2.2%.

The PPI excluding the volatile food and energy categories was unchanged in July from the prior month, the tamest reading in four months. The core PPI rose 2.4% from a year ago.

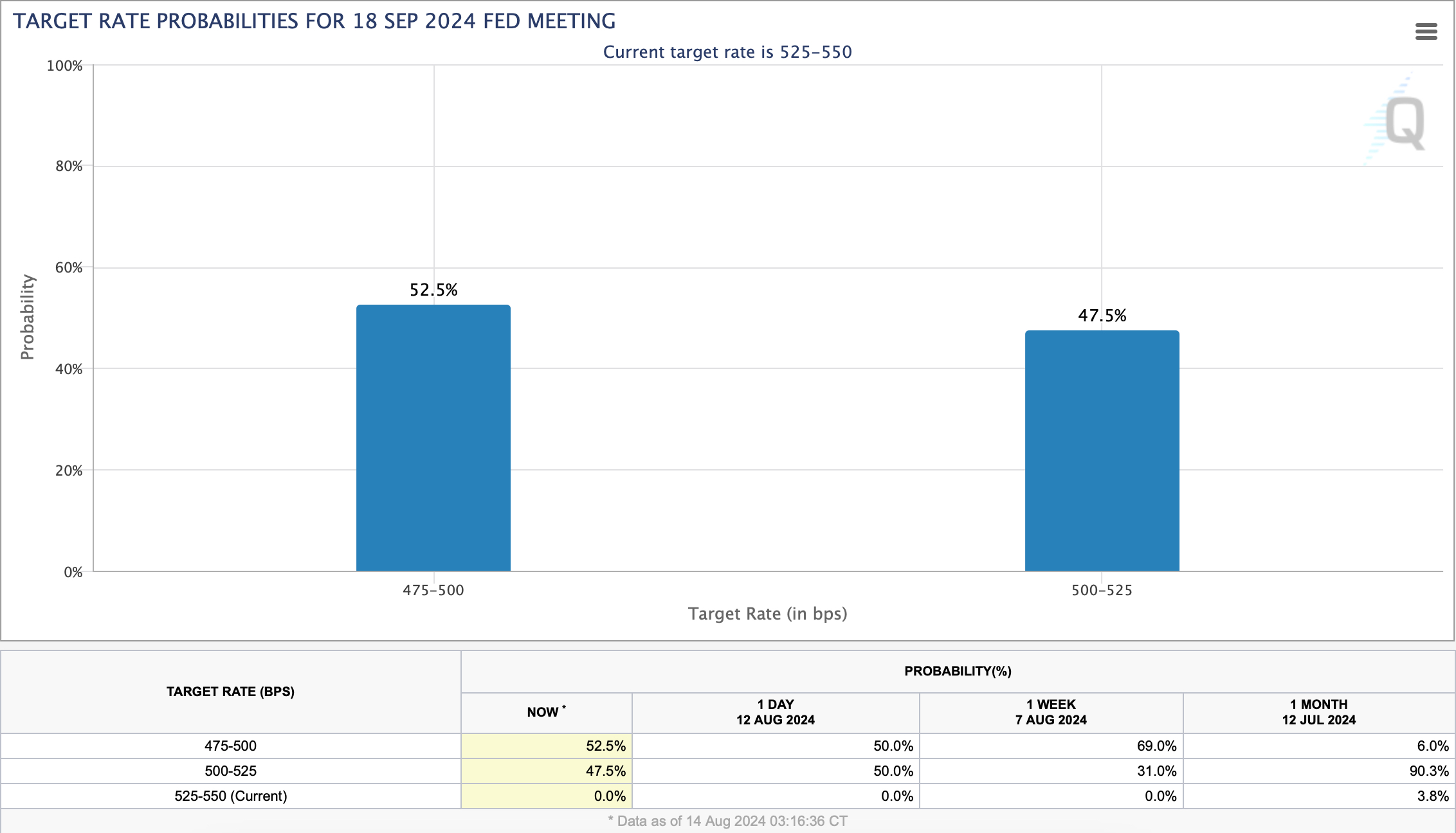

Stock-index futures and Treasuries rose in the trading session that followed the report. Traders marginally pushed up the odds of a half-point rate cut in September. See the current price versus that of one day ago in the chart below.

The categories in the PPI report used to calculate the Fed’s preferred inflation measure, the personal consumption expenditures price index (PCE), showed overall subdued trends.

Specifically, physician care costs and airfares decreased, while the cost of hospital outpatient care remained unchanged. Prices for portfolio management services increased by 2.3%.

July PCE price gauge will be released on August 30th.

Now For CPI

The closely watched CPI figures will be released later today. While labour market talk has taken the headlines over the last week and a bit, inflation still matters… maybe more than anything.

We can visualise this by looking at the Russell 2000 index, which is one of the most prone to inflation data. The biggest price swings have come on data releases, with the exception of the latest move down due to labour market concerns.

Inflation numbers primarily impact the stock market because of their effect on interest rates. The Fed’s 5.25-5.50% rates are in place to cool inflation, which rallied to 9.1% in 2022.

Lower rates mean that future profits can be discounted at a lower rate. Higher rates are the opposite.

For much of the time that rates have been at their peak, the conversation has been about the Fed cutting when inflation was under control—not cutting too soon or leaving rates overly restrictive. The labour market and growth had been strong and, therefore, never served as much concern in the conversation.

Now, there is a tight balance between bringing rates down to help the labour market and making sure inflation doesn’t spike in the future.

If you haven’t seen already—or maybe you’re new around here—our full articles are available for premium readers, along with a weekly rundown of our ideas for the week ahead, released every Monday. You can access a trial here.

The Rates Higher Low (3 Is The New 2)

Rates markets are expecting a quick decline through to the end of 2025. However, they expect rates to flatten out at a higher level than in recent years.