Relief rallies are back, but conviction is still lacking. After five consecutive weeks of losses, US equities finally broke the streak, though the recovery owed more to positioning than a shift in the underlying narrative.

This week, our market wrap has been jointly composed in collaboration with Macro Charts. You’ll notice some of his trademark charts and thoughts interspersed through the article. For anyone unfamiliar with his work, you can access a free trial of his Substack content here.

Last week was effectively decided in a two-day window. Tuesday and Wednesday delivered the entirety of the S&P 500’s 3.4% gain, as headlines pointed to a potential de-escalation in the Iran conflict. That was enough to trigger a sharp unwind in bearish positioning, with short covering across hedge funds, CTAs, and systematic strategies driving a broad-based squeeze. Flows from pension rebalancing and quarter-end dynamics added fuel, turning what might have been a modest bounce into a more aggressive rally. By Thursday, the move had already begun to lose momentum. President Donald Trump’s renewed hardline stance on Iran briefly knocked sentiment before dip buyers stepped in, leaving the index marginally higher into the close.

Goldman Sachs and JPMorgan desks both pointed to the bounce being led by an unwind of extreme positioning, rather than a sudden change in investor sentiment.

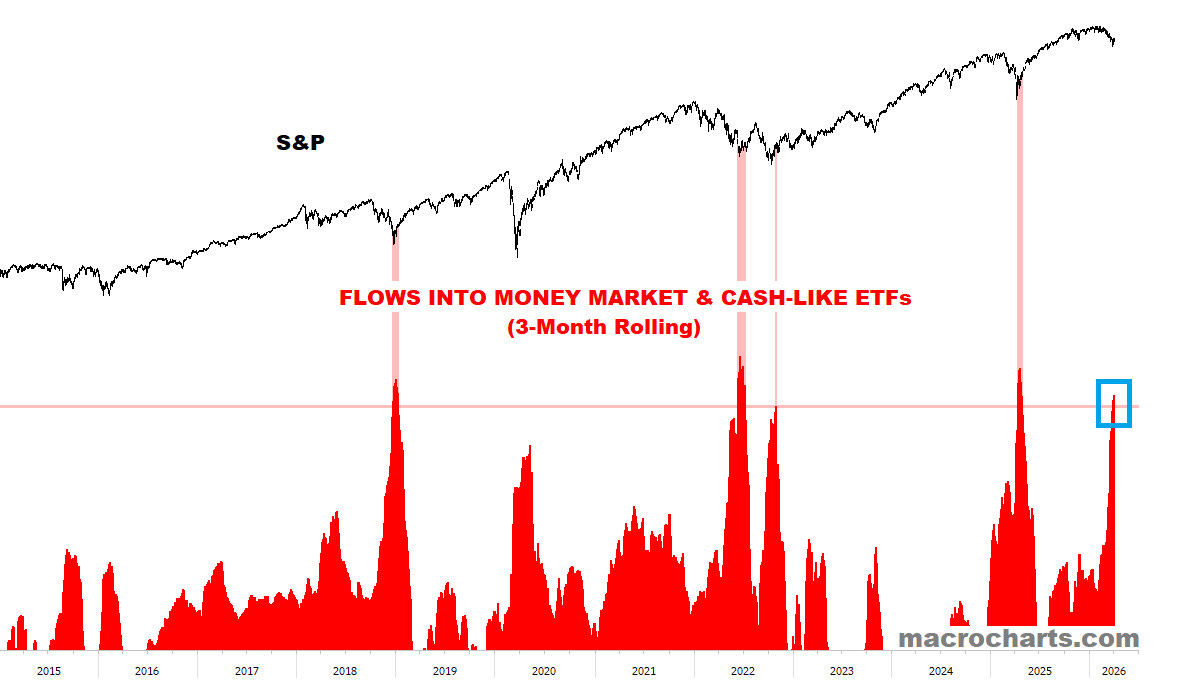

Investors are in one of the biggest “rushes to cash” in history:

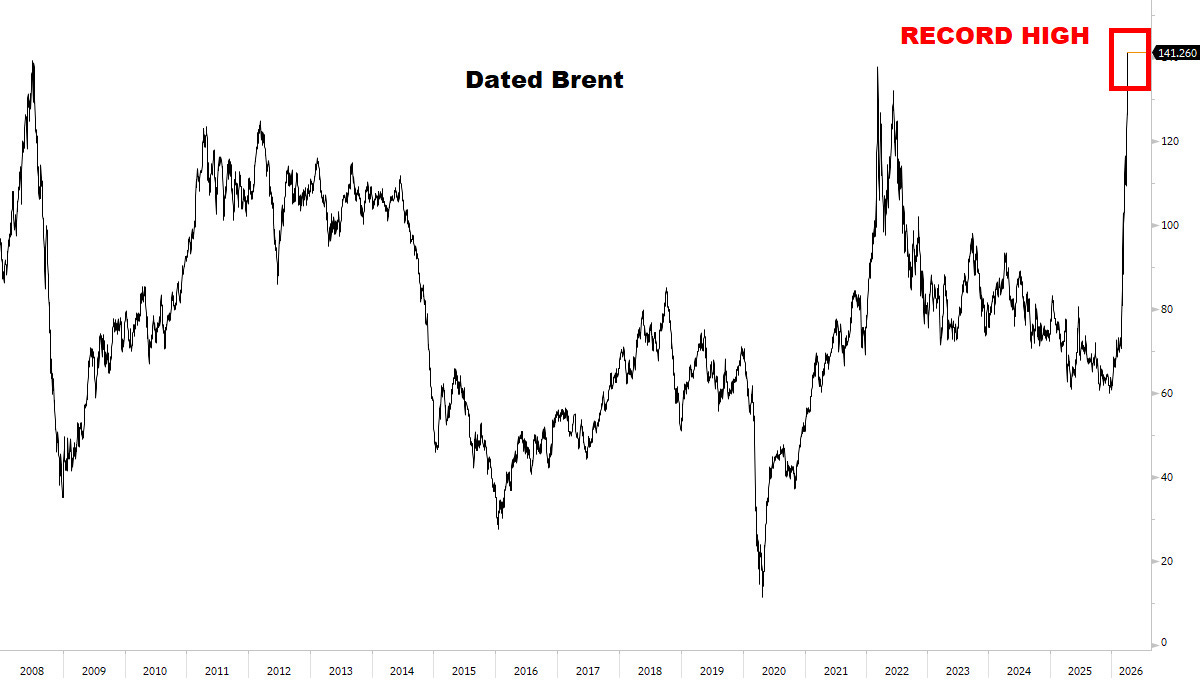

Semiconductor and tech hardware stocks led gains, not on improved fundamentals, but as positioning snapped back. Energy (the market’s leadership cohort for much of the past month) lagged sharply despite brent breaking to multi-year highs, a sign that the trade had become crowded and vulnerable to profit-taking.

Private credit continues to cast a shadow over financials, with Blue Owl limiting redemptions across two funds after a surge in withdrawal requests. The move reinforces the broader theme of tightening liquidity within the space, and the knock-on effect was visible across listed asset managers. Consumer staples, typically a defensive refuge, also showed signs of strain, with mixed performance reflecting uncertainty around both input costs and corporate activity.

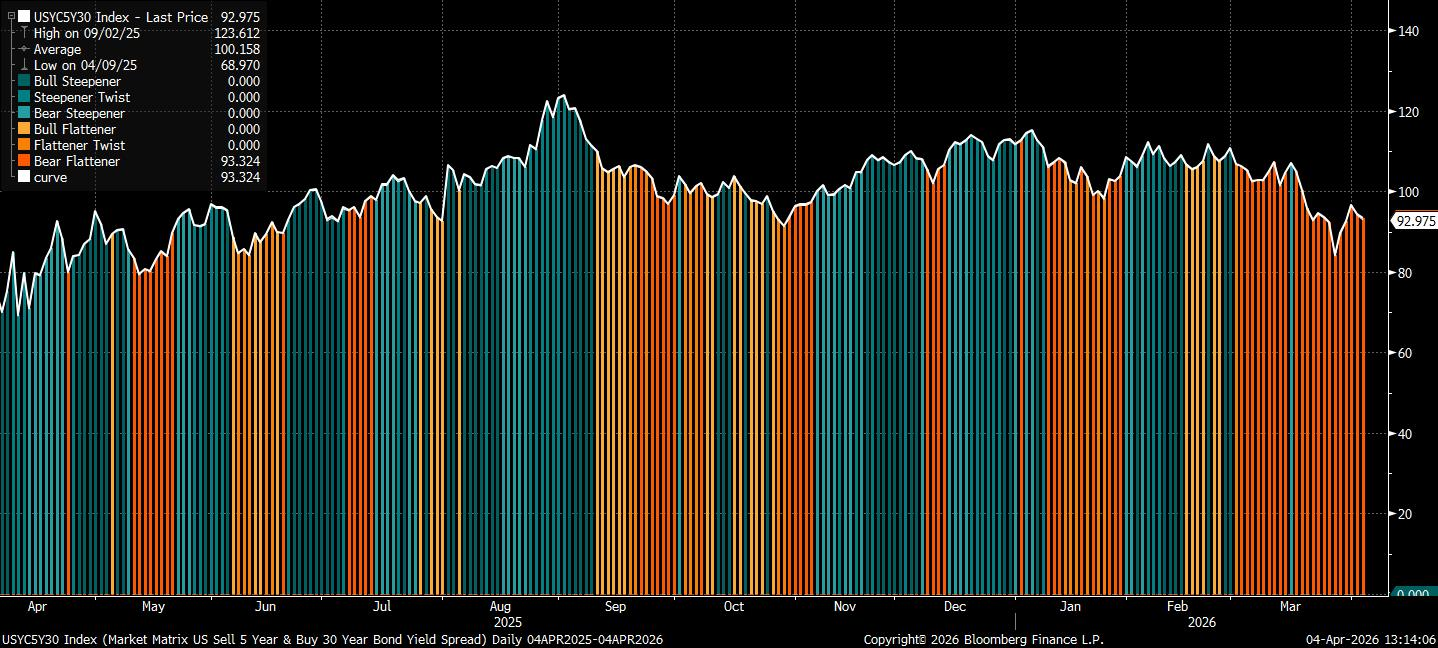

The dollar softened modestly on the week, but broader dynamics remain intact. In rates, there was a partial reversal of the aggressive flattening seen in recent weeks, with 5s30s steepening modestly as growth concerns begin to challenge the inflation narrative at the margin. Options markets are beginning to reflect that tension, with positioning suggesting a growing appetite for downside yield moves even as inflation risks persist.

Markets are oscillating between two competing forces: the hope of de-escalation and the reality of a macro environment that has already tightened materially. The fact that a modest improvement in headlines can trigger such a sharp squeeze speaks to how extended positioning had become. But without a sustained shift in either geopolitics or inflation dynamics, rallies are likely to remain fragile. For now, this looks like a reset in positioning rather than a reset in trend.

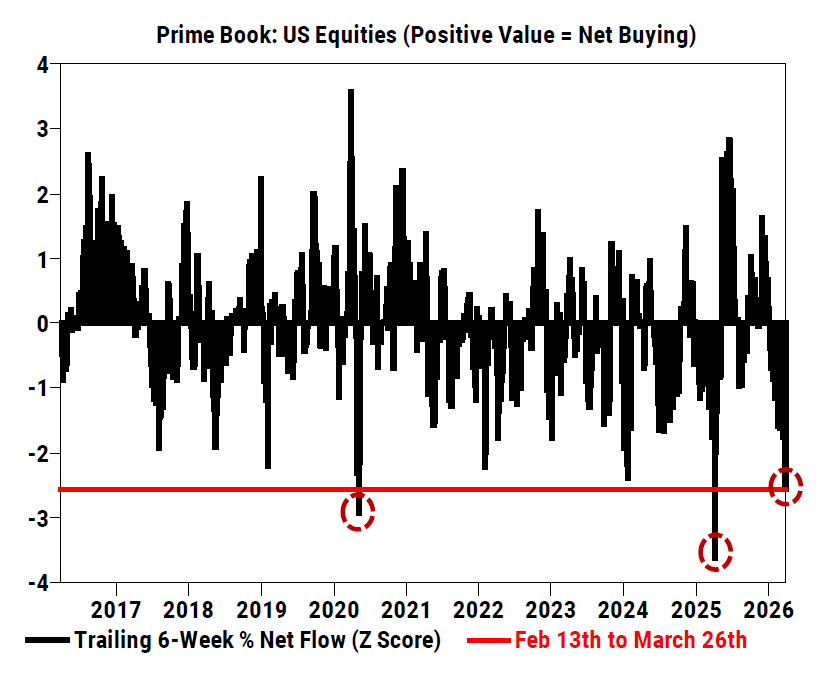

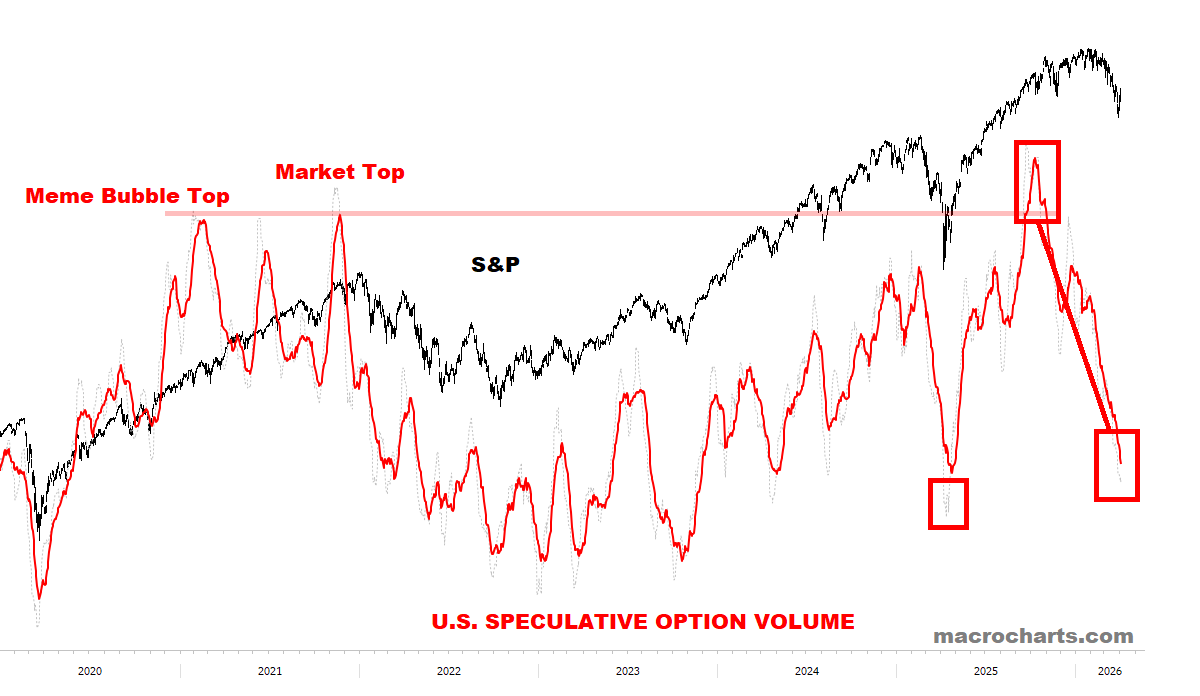

From the visuals that Macro Charts is observing, speculative ‘animal spirits’ have collapsed since October — but are still declining and could go lower. Buy signals are pending:

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“NFP: Strong Headline, Softer Reality”

“Energy Shock Hits CPI”

“Oil’s Physical Air Pocket”

NFP: Strong Headline, Softer Reality

US job growth rebounded in March, with nonfarm payrolls rising by 178,000 (vs 60k expected) and the unemployment rate edging down from 4.4% to 4.3%. In fact, the headline figure was the highest in almost 18 months.

The boost was supported by broad-based hiring, led by healthcare, alongside gains in construction and transport. Manufacturing activity also staged a recovery, with the strongest hiring since the end of 2023.

| A guest post by

|