A Chink in Gold's Armour

Gold is the supply for the demand for dollars, which presents a longer-term opportunity in markets.

There is a certain irony in the way gold behaves when the world actually starts to end. For decades, the gold bugs have promised that when the great conflagration finally arrives (whether in the form of a systemic banking collapse or a regional war involving a major oil producer… perhaps), gold would be the only thing left standing. Yet, as we have seen in the tumultuous weeks of March 2026, when the conflagration actually shows up, gold spends the first few rounds on the mat.

The recent drawdown in gold prices has been, in a word, violent. After a multi-year rally that seemed to defy the gravity of high real rates, the yellow metal has hit a wall of selling pressure. But to paraphrase a market adage: do not mistake a liquidity event for a change in regime. Our assessment is that the fundamental drivers of the gold bull market remain not only intact but are actually being strengthened by the very volatility that is currently depressing prices.

Sovereign Sellers

The primary question on every desk right now is why gold is falling exactly when the geopolitical risk, specifically the escalation of the Iran war, is at its zenith. That answer lies in the plumbing of global finance, not in a sudden loss of faith in gold’s value. Gold is often described as the “ultimate haven,” but in the initial stages of this crisis, it functions as the “ultimate liquidator.”

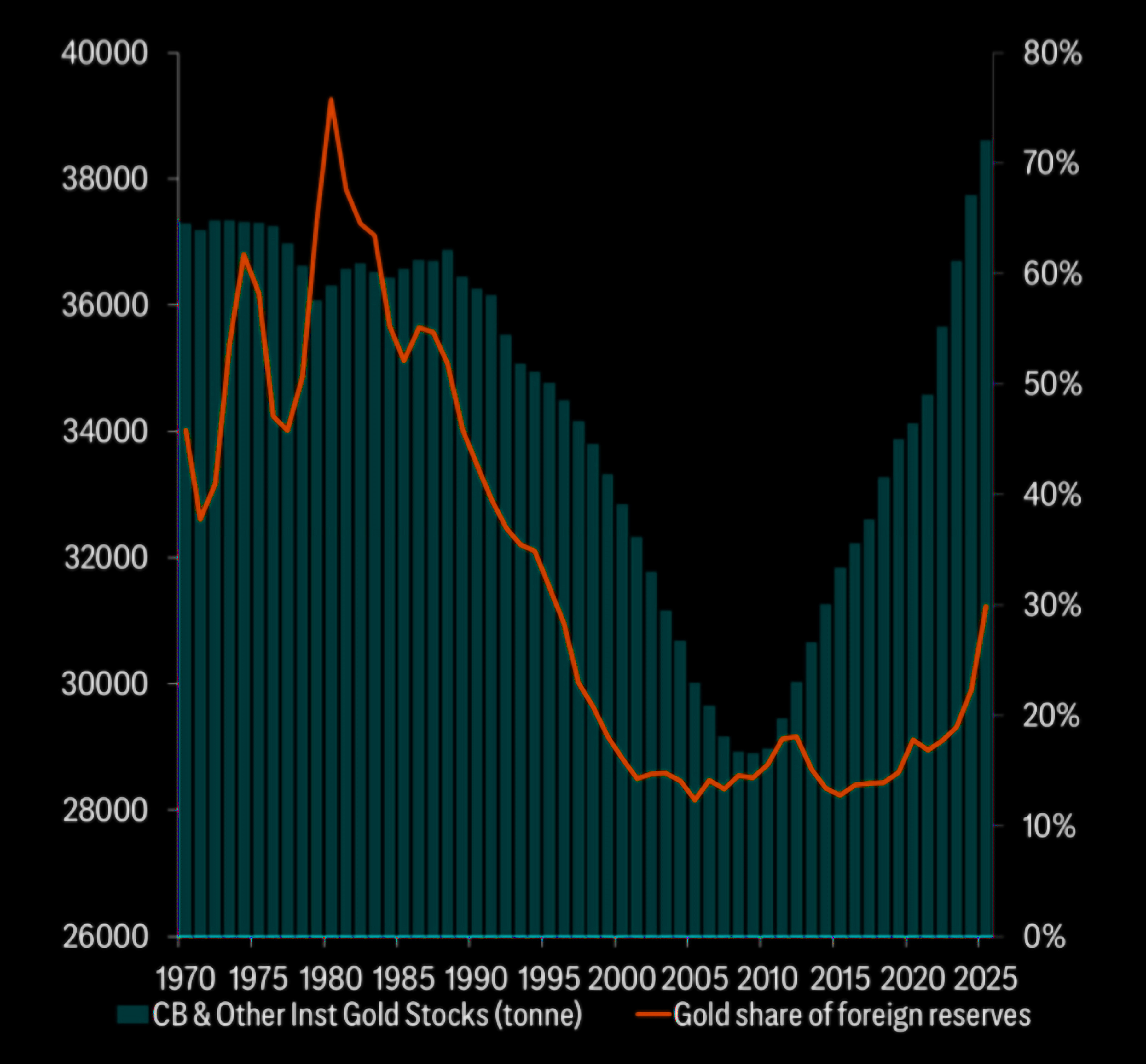

The recent selloff has been predominantly driven by the urgent liquidity needs of major sovereign actors. For several years, central banks, particularly those in emerging markets, have been the dominant source of inflows into the gold market. However, a war in the Middle East and the resulting closure of the Strait of Hormuz create a specific kind of financial stress. When oil prices spike and regional currencies come under pressure, these same sovereigns often have to de-gross their portfolios to raise immediate cash.

In the early stages of a major macro correction or a geopolitical shock, investors and sovereigns alike sell what they can, not necessarily what they want to. Because gold is a highly liquid, deep market with no counterparty risk, it is the first ATM that central banks visit when they need to defend a currency or cover margin calls on falling equity positions. These liquidity-driven moves often disregard long-term fundamentals in favour of immediate solvency. When the Strait closes, the need for dollars becomes the only game in town.