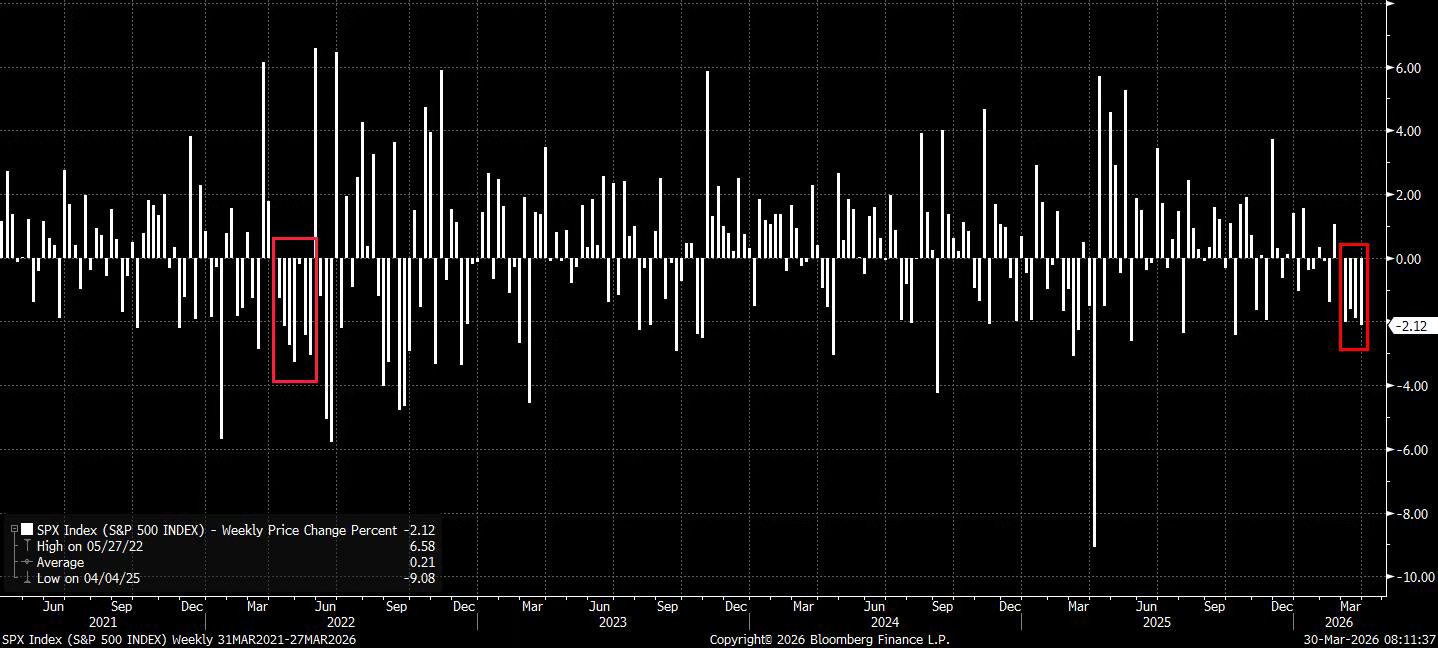

The war in the Middle East has now evolved into a sustained drawdown, with US equities posting a fifth consecutive weekly decline as the war in Iran continues to bleed into the macro backdrop. It is the longest losing streak in four years.

Early-week optimism proved fleeting. Hopes for a diplomatic off-ramp and a temporary reprieve in oil prices supported a modest bid on Monday, but conviction remained shallow. By midweek, now-familiar uncertainty intensified, energy prices firmed, and markets confronted the implications of a more persistent shock. Selling accelerated into the latter part of the week, leaving the S&P 500 at its lowest level since August and within striking distance of a technical correction. No one is willing to hold risk over the weekend.

Technology remains the epicenter of weakness. The sector is contending with a dual headwind: geopolitical risk and a growing reassessment of AI-driven valuations. Reports around Anthropic’s latest model and efficiency breakthroughs from Google have added to concerns that the competitive landscape is shifting faster than expected, weighing on semiconductors, cybersecurity, and broader software.

By contrast, the leadership is narrow. Energy continues to outperform as crude prices remain elevated, extending its run of relative strength and marking yet another record for the sector. Defensive areas such as consumer staples and utilities have also started to find a bid, reflecting a more traditional late-cycle posture as investors rotate toward balance sheet resilience and pricing power.

Positioning and sentiment are beginning to shift alongside price action. The early phase of the conflict was characterised by a willingness to fade the move, anchored in expectations of a quick resolution. That assumption is now being challenged. Sell-side desks are increasingly flagging the risk of complacency, with a growing recognition that elevated energy prices, if sustained, will have a more material impact on both growth and inflation than currently priced. The debate has moved from whether to buy the dip to whether the market is entering a more protracted adjustment phase.

Macro signals are reinforcing that shift. Inflation-sensitive data is beginning to pick up, with import prices surprising to the upside and providing an early indication of pass-through effects. Fed communication has remained firmly cautious, with the balance of risks tilting away from easing and, at the margin, reopening the possibility of further tightening should inflation pressures persist. Rate markets have responded accordingly, with expectations for cuts continuing to be pared back and tail-risk hedging around hikes starting to re-emerge.

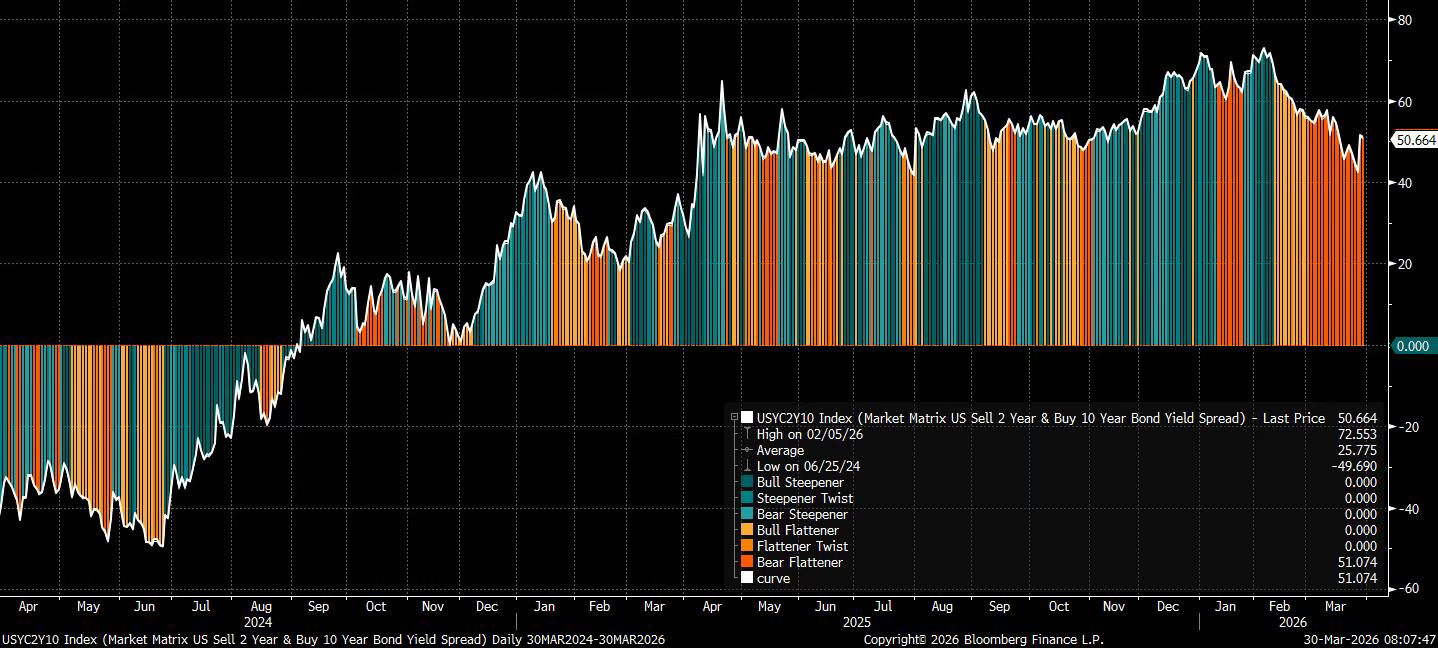

Across assets, the US dollar has resumed its grind higher, supported by rising front-end yields and persistent geopolitical demand. The curve continued to flatten, with weak auction demand highlighting investor reluctance to add duration at current levels. Options markets are beginning to reflect a shift in regime as well, with positioning increasingly skewed toward protection against further policy tightening.

The key takeaway is that markets are trading a change in conditions. The combination of elevated energy prices, tighter financial conditions, and diminishing policy flexibility is creating a more fragile equilibrium for risk assets.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“Far More Reactive to Relief”

“OECD Flags Risks to Inflation”

“Safe Jobs, Hard Problem (NFP Preview)”

“China’s Decoupling from Oil Risk”

Far More Reactive to Relief

After a bruising month that has pushed the Nasdaq into correction territory and dragged the S&P 500 close behind, the question is no longer whether the news flow is bad, but whether that bad news is already reflected in positioning.