A UK Growth Stock Addition To The Portfolio

Strong results just out confirm a rosy outlook for this FTSE 100 name.

For those new to the club, we started our own Global Asset Portfolio at the start of the year due to popular demand. We’re up over 10% year-to-date, comfortably beating our benchmark.

Next week, we’ll be dropping more details on our May performance in detail. You can read our April review here.

We don’t currently share real-time updates on our transactions, although this is something we might look to launch later in the year for paid subs. However, from time to time we do like to share a particular stock we like and will add, along with more detailed reasonings on our thinking.

With that in mind, here’s one UK growth stock from the FTSE 100 that just released results that we’re keen on.

Before we get going, a friendly reminder that you can become a premium subscriber with us for just £10 a month. Aside from access to our Global Asset Portfolio, it provides you full access to our weekly articles without a paywall, including our flagship Monday trade ideas.

First… the FTSE 100

Before we get onto the specific stock, we want to explain why we’re looking in the FTSE 100 and the FTSE 250 in the first place.

We feel that the UK equity markets have been overlooked for some time and are trading at cheap valuations. Evidence of this can be seen from the amount of companies being bought out that are listed on FTSE markets.

As a snippet from a recent FT article highlights:

“The value of bids for London-listed companies this year has hit the highest level since 2018, as beaten-up share prices help entice suitors and hand the UK a role in the burgeoning recovery in global dealmaking.

London-listed groups have received more than $78bn worth of bids this year, with the majority coming from overseas buyers, according to data from Dealogic.”

While it would be frustrating to buy a stock that’s undervalued and then have it delisted due to a buyout, it’s not the end of the world. Although we aren’t investing for M&A action, any deal would represent a short-term quick buck based on a likely premium paid on the current share price.

As something to mull over for those who want to dig deeper into UK domestic companies (that mostly sit in the FTSE 250), consider this: The current price-to-earnings ratio of the FTSE 250 is 15.47, the lowest level since the start of the pandemic.

Auto Trader (LSE: AUTO)

A brief rundown:

Within the FTSE 100 sits Auto Trader. It’s a comprehensive online marketplace that facilitates the buying and selling of vehicles. It provides a platform where both individuals and dealerships can list cars, complete with detailed descriptions, photos, and videos. Listings are charged, providing a constant revenue stream.

Users can search for vehicles based on criteria such as make, model, price, and location and access valuation tools to estimate vehicle values. The site also offers vehicle history reports, financing options, and trade-in services. As a further revenue stream, the business allows adverts, and with the use of AI, it can tailor suggestions to users.

Growth of financials

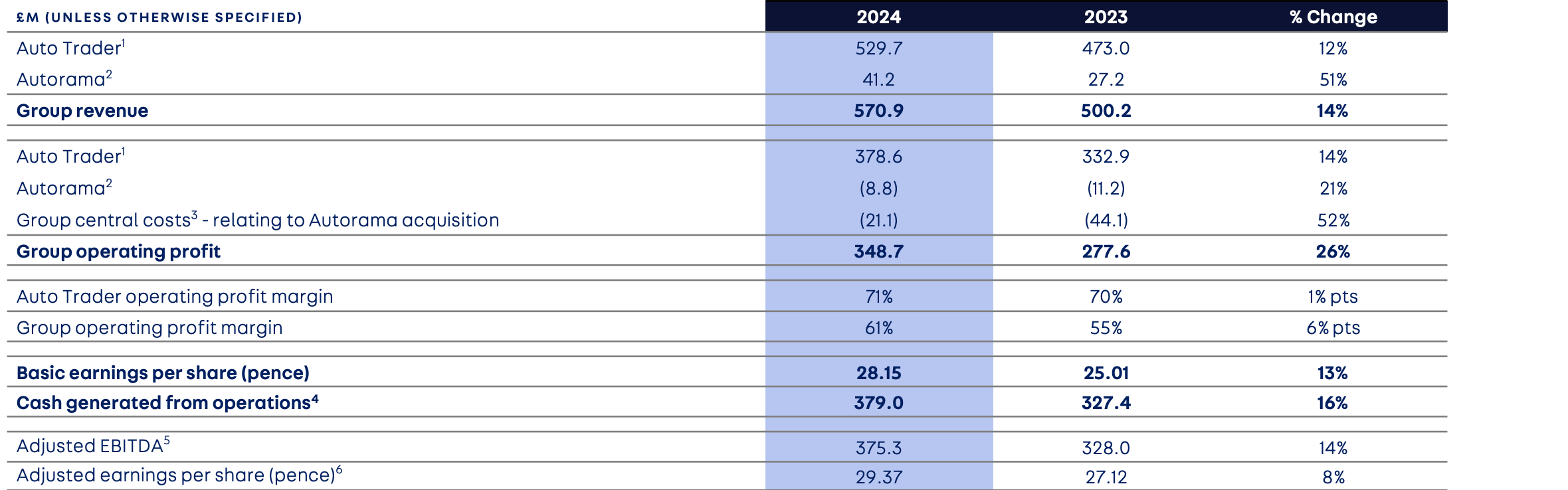

Below is a handy snippet of the growth from top-line revenue through to profit before tax from the past five years. This doesn’t include the 2023 results that came out on Thursday (more on that shortly).

On the revenue side, it’s clear that demand is there and growing. Revenue has increased from £355m in 2019 to £500m in the latest reporting year above. In the results out today, revenue hit £570m for the year just ended.

To us, revenue growth is important when looking to include a stock in a portfolio. It’s one of the cleanest ways to see if a business truly is expanding. Other measures (e.g., operating profit) can be distorted by a variety of factors.

We also flag up the low net interest charge, and the fact that it has been falling over the years. Auto Trader has relatively little debt, reporting £69.4m, which gives a debt-to-equity ratio of 0.11. We like stocks with low/manageable debt levels for a few reasons.

Firstly, given the elevated interest rate environment, high debt levels give high interest costs, eating away cash flow. Second, high debt levels are a distraction for the company, in that they are focused on managing debt rather than driving the firm forward.

Third, a lack of debt indicates the business has enough retained earnings and cash flow to alleviate the need to borrow funds. Granted, some will look to debt to support expansion. But there’s nothing wrong with growing naturally, predominately through earnings.

The latest results

The report just out gives us more reasons to like the firm. Again, let’s start with the numbers:

Almost without exception, there was strong growth year-on-year. It’s worth noting the Group figures include Autorama.

Autorama is a leading platform in the UK for leasing vehicles, particularly vans and, increasingly, cars. Established in 2004, it aggregates leasing deals from various funders and original equipment manufacturers (OEMs), providing a comprehensive selection for consumers.

Auto Trader bought the company back in 2022, and after time spent to integrate the offering, 2023 was the first year where the synergies could really be felt. The 51% jump in revenue shows the clear benefit offered here with the two firms.

We feel this integration should yield further benefits this year and next.

Next up let’s talk about the market share dominance. Over 75% of all minutes spent on automotive classified sites were spent on Auto Trader.

Cross-platform visits were up 11% to 77.5 million per month (2023: 69.6 million), while minutes were up 8% to 553 million per month (2023: 514 million minutes).