The ECB just became the first major central bank to raise interest rates this year in response to the energy price shock from the war in the Middle East.

Today, the committee, led by Christine Lagarde, raised its deposit facility rate by 25bps to 2.25%, its first rate hike since September 2023. Even though the move was widely anticipated (65 of 67 economists surveyed by Bloomberg expected this outcome), it was the updated staff projections on inflation and growth that caught our attention, as did Lagarde’s own comments at the press conference.

It’s clear to us that the ECB have swiftly pivoted to a “go big or go home” approach to tackling the inflationary impact, and we now think the deposit rate can rise multiple times this year. Lagarde clearly did not frame today’s 25bp hike as a one-off response or an insurance hike, as we thought they might, to retain optionality further out.

Yet we believe the multiple likely hikes this year will ultimately prove to be a mistake, given the likely hit to economic growth, and could see EUR come under pressure later this summer. This leads us to add a six-month EUR/USD option structure.

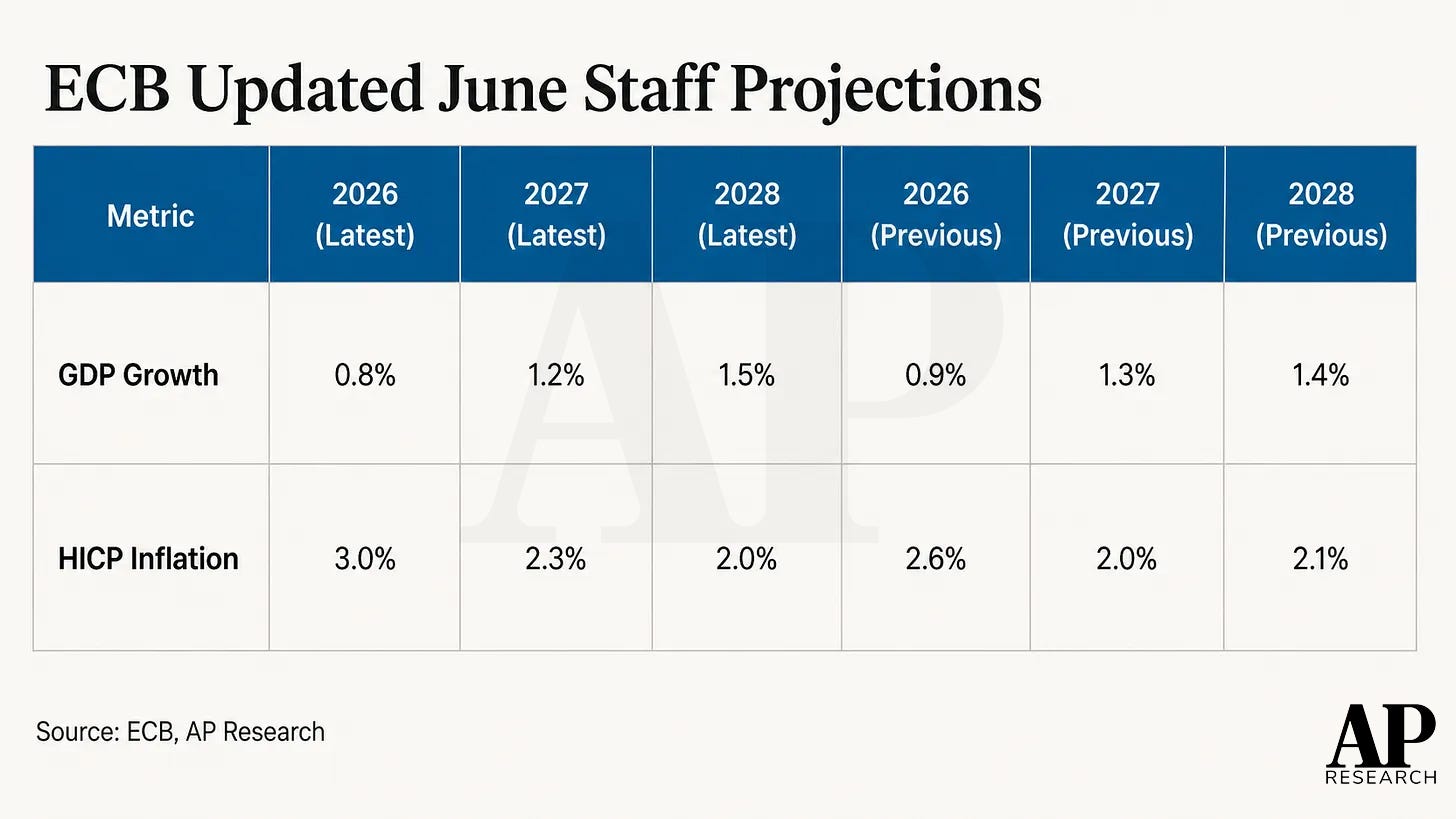

Inflation Projections Lifted…

The ECB revised its inflation forecasts significantly upward and trimmed growth expectations, as detailed below.

That makes it difficult for the ECB to sound dovish. In the baseline, inflation is not back at target until 2028, while core inflation remains above target through the entire projection period. The ECB also expects headline inflation to peak at 3.4% in Q3 and Q4 2026 and remain above 3% until early 2027, with the energy shock gradually feeding through to food, goods, and services.

The scenario analysis strengthens the point. In the milder scenario, oil normalises faster, inflation undershoots the 2% target in 2027 and 2028, and growth recovers more robustly. But that is essentially the “everything calms down quickly” case. The more policy-relevant risks sit in the adverse and severe scenarios. In the adverse scenario, HICP inflation runs at 3.3% in 2026, 3.0% in 2027 and 2.3% in 2028, with core inflation peaking at 2.7% in 2027. In the severe scenario, headline inflation reaches 4.0% in 2026 and 5.3% in 2027, while core inflation rises to 3.8% in 2027 as energy costs feed into domestic prices and wages.

So even though Lagarde did not pre-commit to further hikes, the updated inflation figures clearly shifted the burden of proof. With inflation revised higher, core inflation above target through 2028, and adverse scenarios indicating a meaningful risk of second-round effects, the GC has effectively told markets that today’s hike won’t fix all of that and, therefore, more tightening is needed.

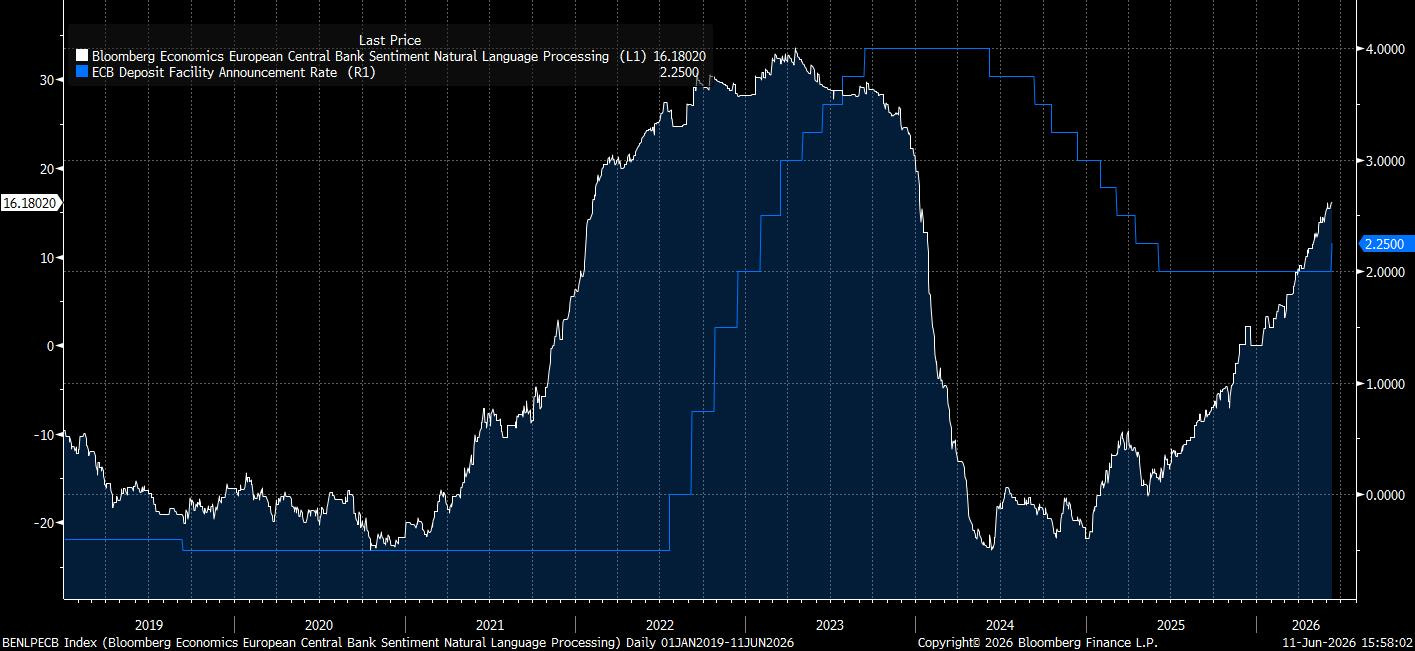

It’s not even just our perception here, as the ECBspeak Index continues to climb.

The extent of any further tightening wasn’t specified, with Lagarde saying there would be no preset rate path. The neutral rate wasn’t discussed either, but consensus is that it’s around the 2.50-2.75% range, which would suggest at least two further hikes this year. Arguably, in order to materially provide an impact to dampen the inflationary pressure, we’d say it needs to be at least at the neutral range, if not higher.

…But Growth Downgraded

The problem as we see it lies in the health of the economy, which will only be put under further pressure from monetary policy tightening.

The ECB now sees eurozone GDP growth at just 0.8% this year and 1.2% next year, both lower than previously expected. That is not recessionary, but it is hardly an economy with much spare capacity to absorb additional tightening. The central bank is raising rates into an economy already being squeezed by higher energy costs, weaker consumer confidence, slower household spending and pressure on exporters.

If the inflation problem was being driven by excessive domestic demand, we’d be less concerned. But it’s not. It is being driven by an external energy shock.

There’s also concern that although higher interest rates can cool demand and lean against second-round effects, they cannot produce more oil, reopen supply routes or remove the geopolitical risk premium from energy markets. What’s to say that the base rate needs to go higher still in 2027 if we don’t get a conflict resolution in H2?

The central bank statement concluded it could no longer wait out the shock, prioritising price stability over economic momentum. That’s all well on paper, but markets aren’t stupid when assessing longer-term implications.