All Happening on the Everything Front

A weekly look at what matters and how to trade it. (March 2nd)

We are only two months into the year, and the market has already burned through multiple narratives.

The AI “scare trade” returned with force, and this time it wasn’t contained to speculative corners. A dystopian thought exercise from Citrini Research metastasised into a broad de-risking event, reinforcing a pattern that has defined 2026: anything perceived as capital-light, labour-dependent, or digitally exposed gets sold on the open. The selling was mechanical and reflexive, and by Monday’s close, it had already done its damage. IBM posted its worst day in 25 years. Payments, wealth managers, asset-light logistics — all swept into the same narrative vortex.

The more important signal was the shift in leadership.

Defensive sectors outperformed decisively. Utilities, staples and healthcare attracted capital in what looked less like a tactical rotation and more like a regime hedge. Goldman Sachs’ HALO basket (heavy assets, low obsolescence) has now outperformed capital-light peers by roughly 35% year-to-date. The market is increasingly rewarding tangible asset bases and pricing power over growth narratives tied to human or digital capital.

Even Nvidia could not arrest the drift. Strong headline numbers were met with indifference, and then outright selling. The stock trades at a multiple that would typically signal value relative to its growth profile, yet the marginal buyer is demanding proof that AI capex is durable. The burden has shifted from “how big can this get?” to “how long can this last?” When the market stops celebrating beats and starts interrogating sustainability, leadership fatigue is setting in.

Financials layered on their own stress. Private credit cracks widened, dividends were cut, redemption gates tightened, and the KBW Bank Index logged its worst drop since April’s turmoil. Credit spreads moved with it. Dimon’s “cockroaches” analogy resurfaced, and whether justified or not, the perception of latent balance-sheet risk was enough to tilt flows further defensive. The quiet storm in private markets is now visible enough to influence public ones.

Macro provided little relief. PPI printed hot, services inflation remains sticky, and Fed commentary stayed aligned with a prolonged hold. Rate-cut expectations remain clustered in September and December, but the path there looks less certain. The tariff workaround from the White House complicates the disinflation story further, reinforcing the sense that monetary policy is on pause rather than pivoting.

Cross-asset confirmation was clear. The dollar stabilised. Meanwhile, the 10-year yield breaking below 4% marked a flight-to-quality move. Bond options activity targeting sub-3.8% yields reinforced the idea that hedges are being layered.

All of last week’s events were capped by a weekend of major escalations in the Middle East. That creates the central focus for our writing and thoughts this week. So…

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“The Mechanics of Middle East Oil Risk”

“Oil Scenario Analysis”

“The Haven Bid”

“NVDA’s Changing Tone”

“EM Bears Are Extinct”

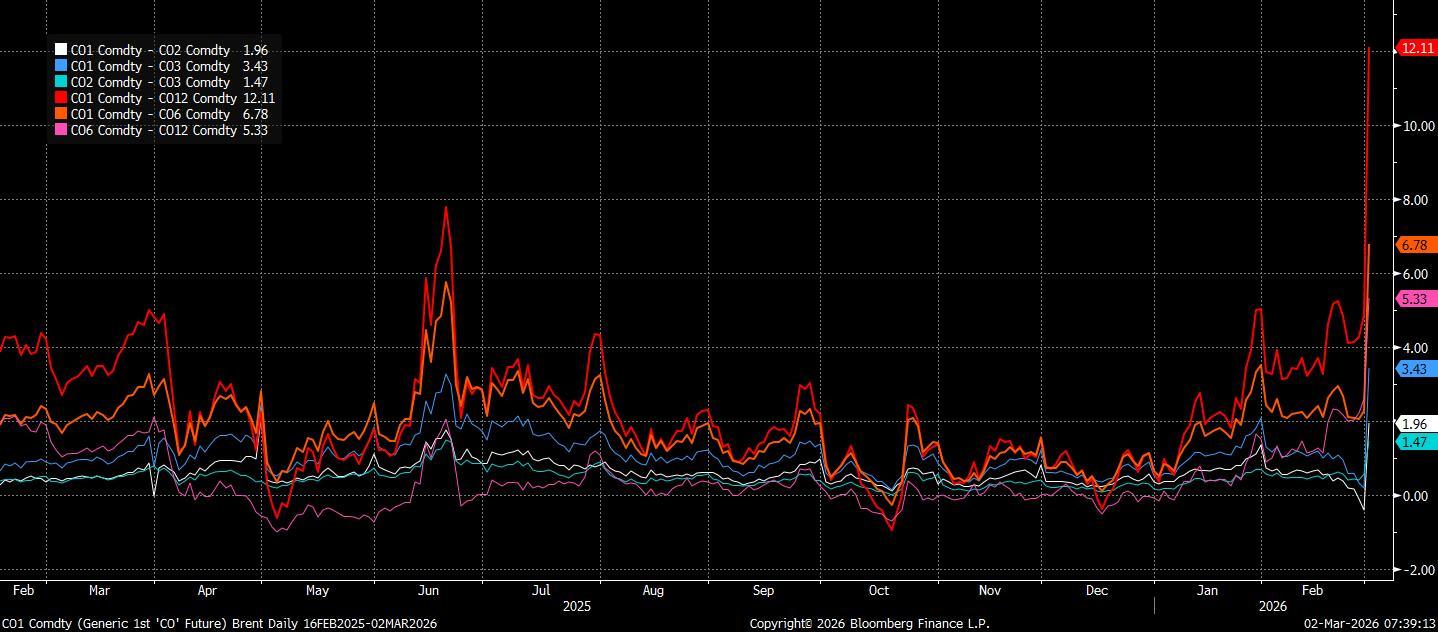

The Mechanics of Middle East Oil Risk

Geopolitics has returned to its familiar setting. The so-called Gulf of Nothing Ever Happens is once again being asked to matter for oil markets. It occasionally does. When it does, it matters quickly.

Before turning to scenarios, it is worth discussing barrels, infrastructure, and incentives.

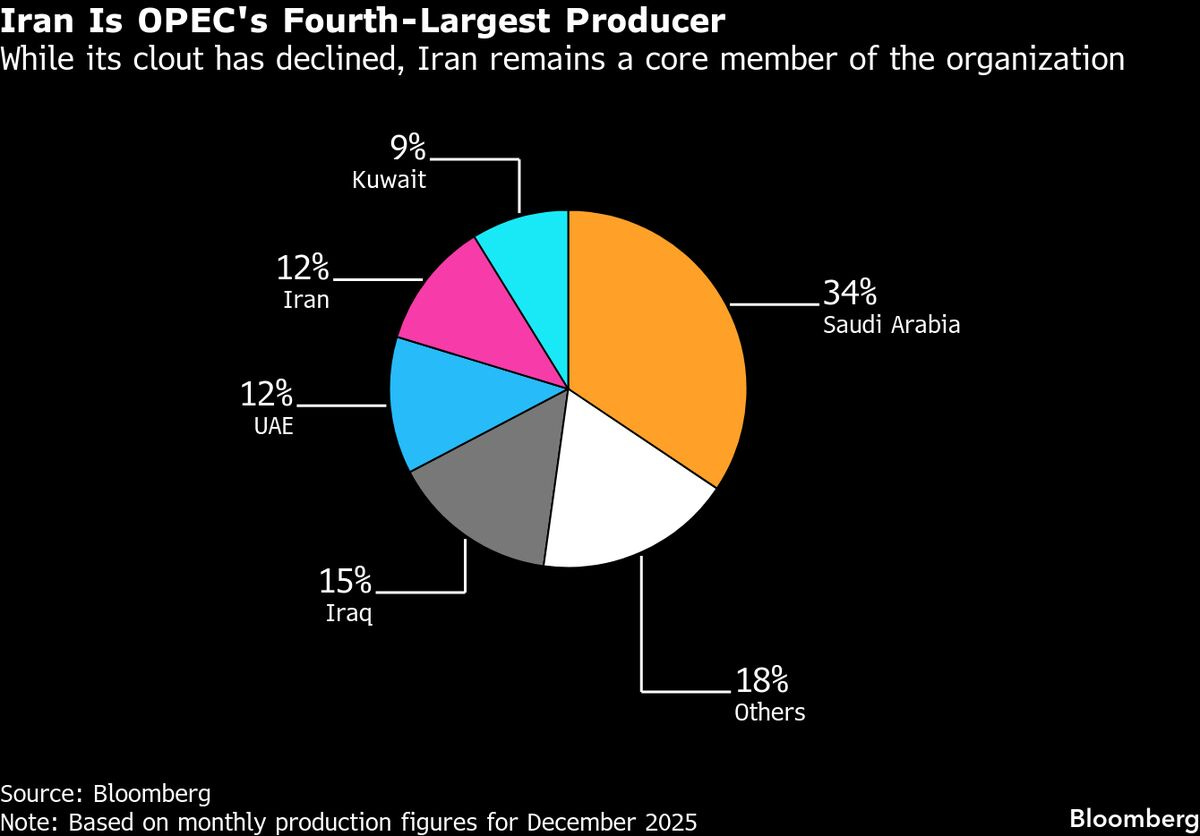

Iran’s Production Machine:

Iran currently produces roughly 3.3 million barrels per day, up from sub-2 million barrels per day in 2020, despite the persistence of sanctions.

About 90% of exports now flow to China, largely via private refiners willing to absorb sanction risk in exchange for discounted crude. The trade is sustained by a shadow fleet of ageing tankers that routinely disable transponders and operate outside conventional monitoring channels.

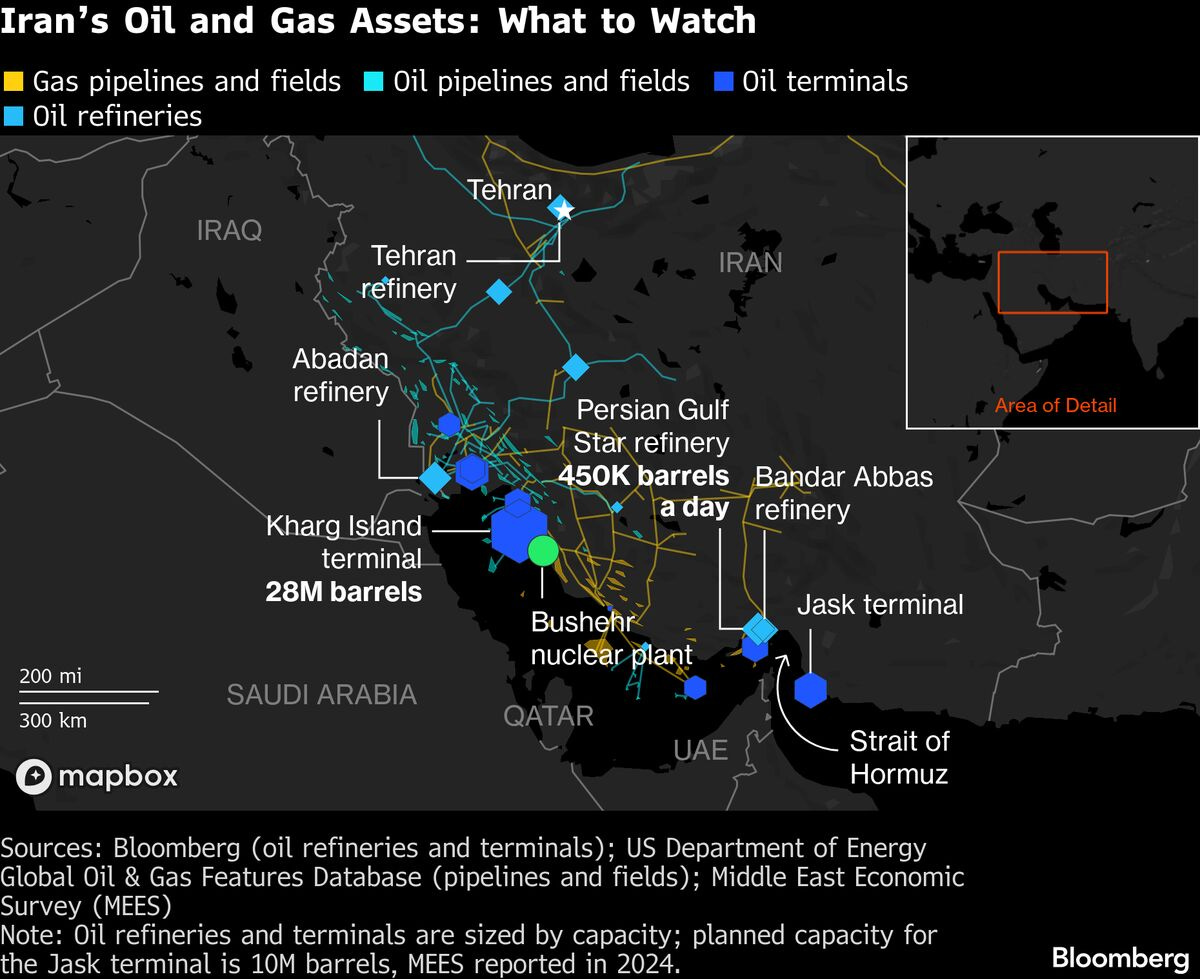

Domestically, refining capacity is anchored by the century-old Abadan refinery (capacity >500 kb/d), alongside major complexes at Bandar Abbas and Persian Gulf Star, the latter geared toward condensate processing. Tehran itself hosts an additional refinery, underscoring that Iran’s system is geographically diversified rather than concentrated in a single node.

Exports, however, are concentrated.

Kharg Island Is the Real Fulcrum:

Nearly all seaborne Iranian crude moves through Kharg Island, the country’s primary export terminal in the northern Gulf. The facility includes multiple loading berths, offshore mooring points, and storage capacity measured in the tens of millions of barrels, with throughput exceeding 2 million barrels per day in recent years.

That concentration creates efficiency and vulnerability for Iran.

Weekend reports of an explosion on the island (notably without confirmation of damage to export infrastructure) highlight the distinction markets must make between events and disruptions. Oil only reacts to the latter.

Iran has reportedly accelerated tanker loadings in recent weeks, echoing behaviour observed ahead of last year’s hostilities. Barrels on water are harder to target than barrels in tanks.

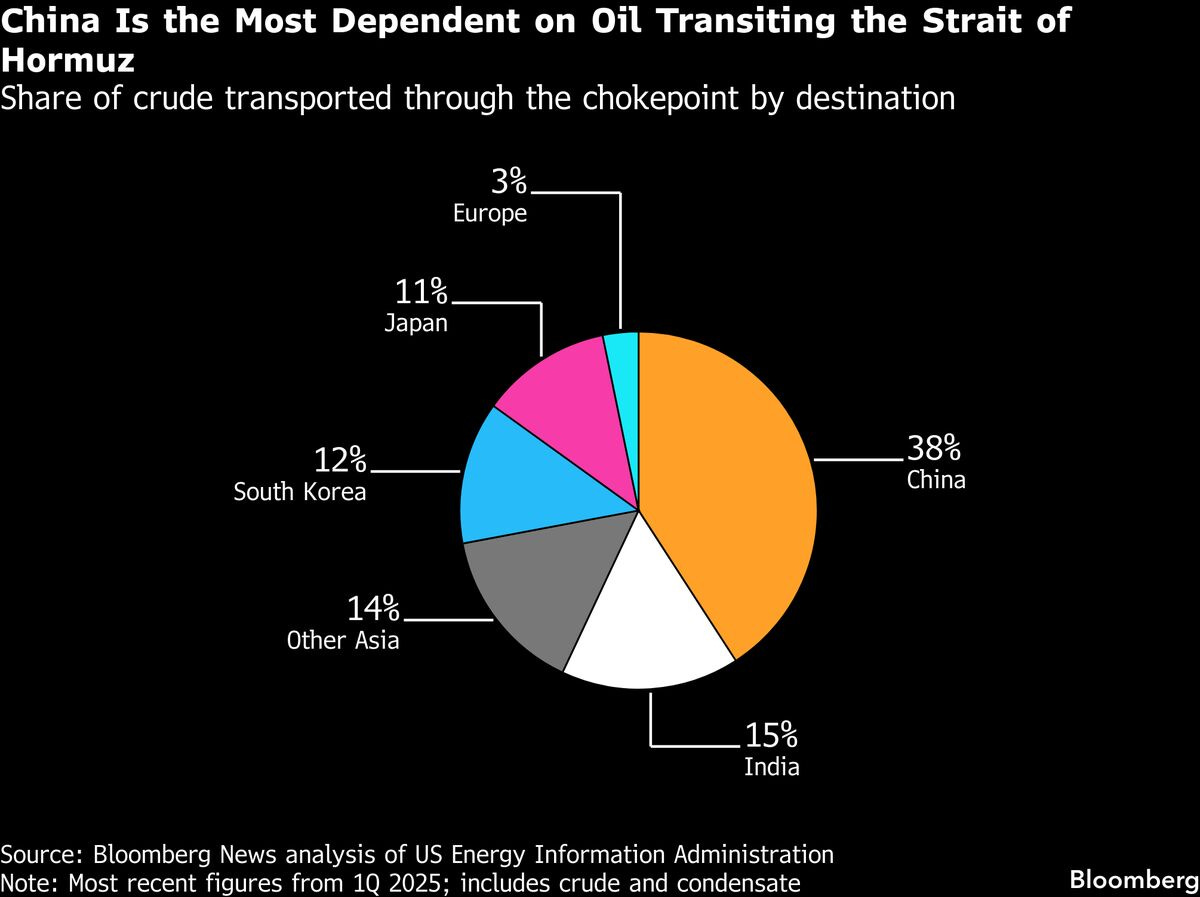

The Strait of Hormuz Threat:

On February 1, Tehran signalled that it could close the Strait of Hormuz, the transit corridor for a substantial share of global crude and refined product flows, as well as Qatar’s LNG exports.

This remains the market’s nightmare scenario, but it is historically unprecedented.

Even partial disruption would matter. Saudi Arabia and the UAE have limited pipeline capacity that bypasses the strait, but it is not enough to offset a full closure. A sustained blockage would constitute a genuine supply shock.

Yet most analysts judge that Iran could not maintain such a closure for long against international naval pressure. Accordingly, the more plausible playbook consists of disruption rather than a full shutdown of oil passageways:

Harassment of shipping

GPS jamming (nearly 1,000 vessels per day experienced interference during last year’s conflict)

Selective infrastructure strikes, as seen in the 2019 Abqaiq attack that temporarily removed ~7% of global supply

Sea mines are another long-threatened option for deterring shipping

These tactics raise insurance costs, slow flows, and inject risk premia without triggering outright war.

Iran must also calibrate escalation against its relationship with China, its primary crude customer and diplomatic shield at the UN. Actions that materially threaten Gulf exports would run directly counter to Beijing’s energy security interests.

But the Market Has Already Run This Drill

The price response during last year’s conflict provides a useful template. Brent spiked above $80, its largest rally in more than three years, only to retrace once it became clear that physical infrastructure remained intact.

By the end of 2025, macro concerns about oversupply had pushed crude roughly 18% lower year-on-year, reinforcing the idea that structural balances still dominate episodic geopolitical risk.

And yet, despite that bearish backdrop, prices have risen ~19% this year, in part reflecting renewed fears of US-Iran confrontation. The geopolitical premium is back, but remains contingent.

A useful empirical rule of thumb comes from historical analysis: A 1% reduction in supply has tended to produce roughly a 4% increase in prices.

This elasticity explains why markets react violently to even small probabilities of disruption, and why rallies fade quickly when flows remain uninterrupted.

The Reality

The current situation is less about whether tensions exist (hint, they always do) and more about whether they translate into measurable supply loss.

But because the infrastructure is concentrated and spare capacity is finite, traders cannot afford to ignore it either. The region does not need to explode to move prices; it just needs to possess the possibility that it might.

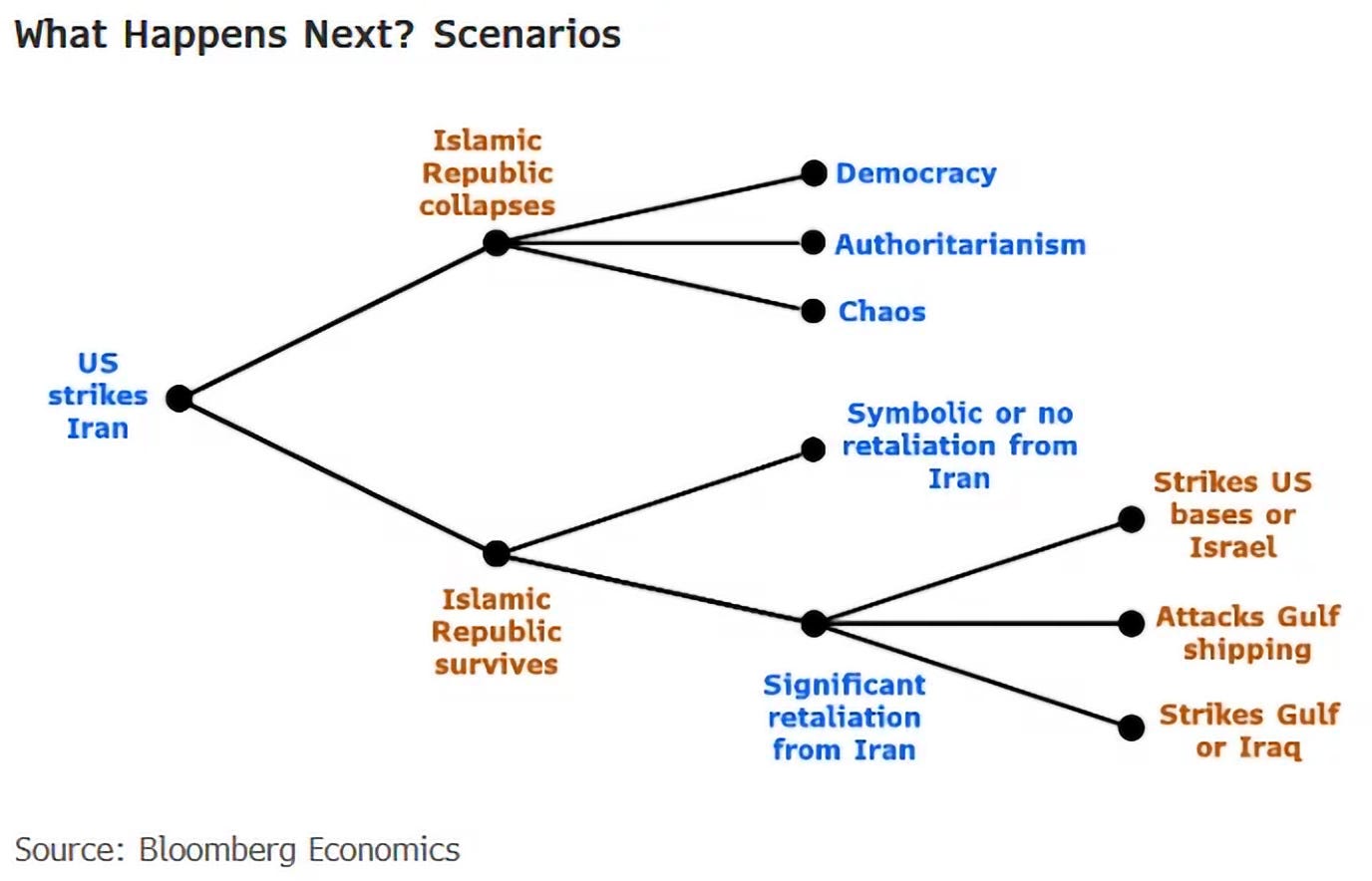

Oil Scenario Analysis

Distilling thoughts into actionable ideas is ultimately where the money is made. We believe the US won’t leave Iran until a new regime (that’s friendly towards the US) is in place. We also believe it’s not in any of the allies’ interests to see this as a drawn-out conflict, so we struggle to see it continuing beyond the next 4-6 weeks.

On that outcome, oil will trade lower, as the risk premium currently implied evaporates and supply comes back online without any constraints.

Such a move lower likely coincides with lower implied volatility in the options space. Therefore, simply buying a put option leaves someone exposed to volatility decay. We like to take this off the table via a CL put spread on M6.

Buy CLM6 1.5x Lev Put Spread

Buy $65 strike 1x Put and sell $60 1.5x strike Put for corresponding May expiry for an upfront cost of $0.85, for a max payoff of circa 5.5:1. Downside kicks in at circa $51.50. Loss capped at premium paid for spot > $65

As was experienced with the whipsaw price action last year, when a similar scenario looked likely to play out, trying to trade this view via spot simply doesn’t work.

The tail risk of a survival of the regime, along with significant retaliation from the nation, can’t be ignored.

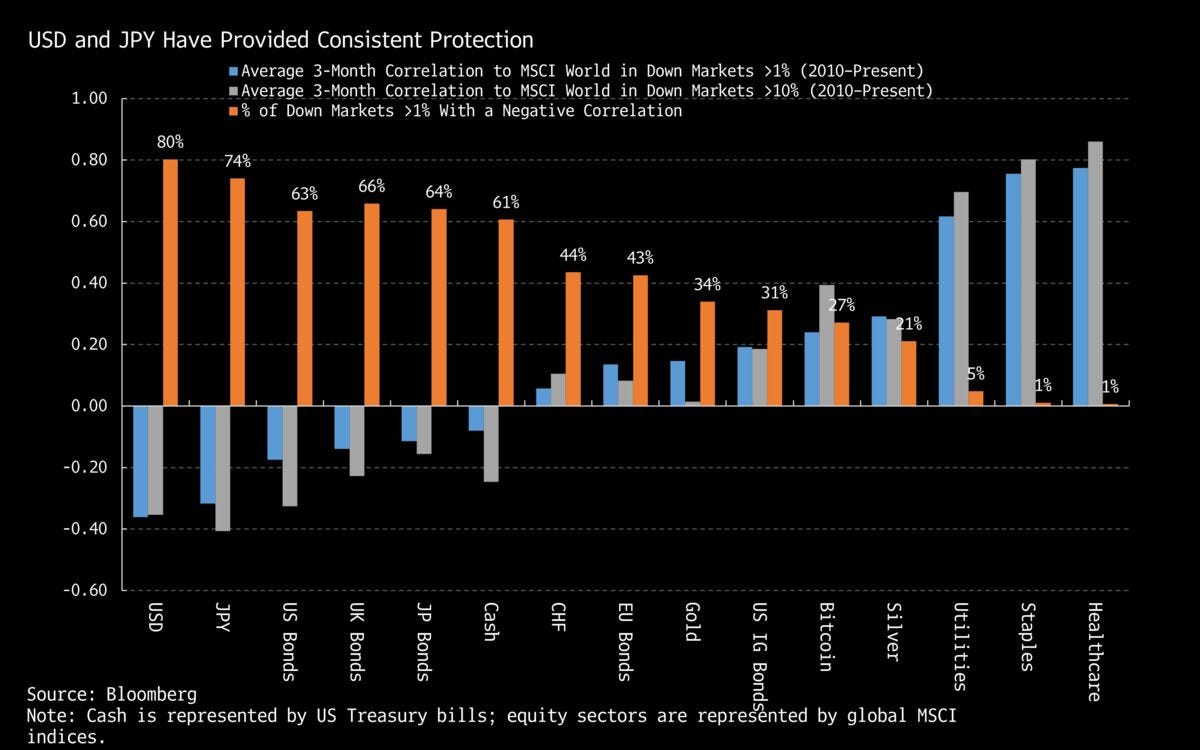

The Haven Bid

There is no such thing as a perfect shelter in a sustained Middle East conflict. Markets can reprice everything when geopolitics turns structural rather than episodic. The question is not which asset is immune, but which one fails the least.

On that score, the dollar still looks difficult to dislodge, even with its recent struggles.

Predictions of its decline have become a regular feature of market commentary, yet when judged against the practical criteria of a haven (negative correlation to risk assets, deep liquidity, perceived store of value, and institutional credibility), no rival quite matches it. Gold has history but lacks stability. The yen has tradition but no longer offers policy independence. The euro offers size, though not unity. The renminbi offers neither convertibility nor trust.

The present shock also carries an inflationary signature. Reports that Iran is obstructing transit through the Strait of Hormuz threaten a material energy supply disruption. Even with OPEC+ pledging modest production increases, the risk premium in oil is unlikely to vanish quickly. This is classic cost-push inflation: a supply constraint rather than an overheating demand cycle.

Here the US enjoys a structural advantage it did not possess in previous Middle Eastern crises. The shift from net energy importer to exporter subtly alters the macro transmission mechanism. Higher oil prices deteriorate the terms of trade for Japan, the euro area and the UK, all large energy importers. For the US, the effect is more ambiguous and potentially supportive at the margin.

Because commodities are priced in dollars, any appreciation of the currency mechanically intensifies the shock for importing economies. The stronger the dollar, the more acute the squeeze abroad.

From a growth perspective, the US slowdown is therefore likely to be milder than that faced by its peers. That in turn grants the Federal Reserve more room to remain vigilant against inflation. With fiscal policy still expansionary and monetary conditions not overtly restrictive, the hurdle for rapid easing rises. In that environment, Treasuries struggle to rally convincingly while the dollar benefits from relative policy firmness.

Real assets deserve mention. Gold and broader commodities traditionally provide protection in inflationary episodes. Yet their volatility is not trivial, and after sharp advances they tend to invite profit-taking precisely when investors most desire stability. A hedge that demands strong nerves is not a universal haven.

Which brings us back to the dollar. It may not be loved, but in moments of stress, markets rarely vote with affection. They vote for liquidity, institutional depth and relative resilience. On those measures, the greenback remains ahead — not flawless, merely first among imperfect alternatives.

NVDA’s Changing Tone

AI is an overarching market theme, but one that ebbs and flows within our guide to themes moving markets week to week.

Nvidia reported, and in a changing tone from recent years, markets barely budged. Perhaps because Nvidia’s guidance is just the other side of the story markets already know well: $650 billion in capital expenditure.

The other consideration we have is less about Nvidia itself and more about what its success implies for the rest of the ecosystem. Strong Nvidia results once acted as a clean read-through for the broader AI trade. “NVDA guides higher = Reward the AI trade.” A question we’ve asked ourselves recently is, “Does NVDA’s success fuel the downside concerns of AI, such as that happening in the software selloff right now?”

A lacklustre response to earnings last week may be an indication that the process has changed, and a stronger Nvidia means more disruption concerns for markets.

Yet, turning to the positive takeaways from the results, Huang pushed back on concerns about the sustainability of AI spending, arguing that customers are already making money from their newly acquired computing power. At the same time, the CFO, Colette Kress, alleviated concerns about the supply chain, noting that the company has supply commitments to fulfil orders well into 2027.

The only concern, one that hands over the entire industry and not Nvidia alone, is related to a memory shortage. Costs are surging from a supply that cannot meet the demands of the AI buildout, but Huang reported that it had supply visibility into 2027 and that its prized mid-70s gross profit margin would be maintained.

The results validated what markets already assumed and gave no downside risks, leaving positioning unchanged rather than forcing a new leg of the trade.

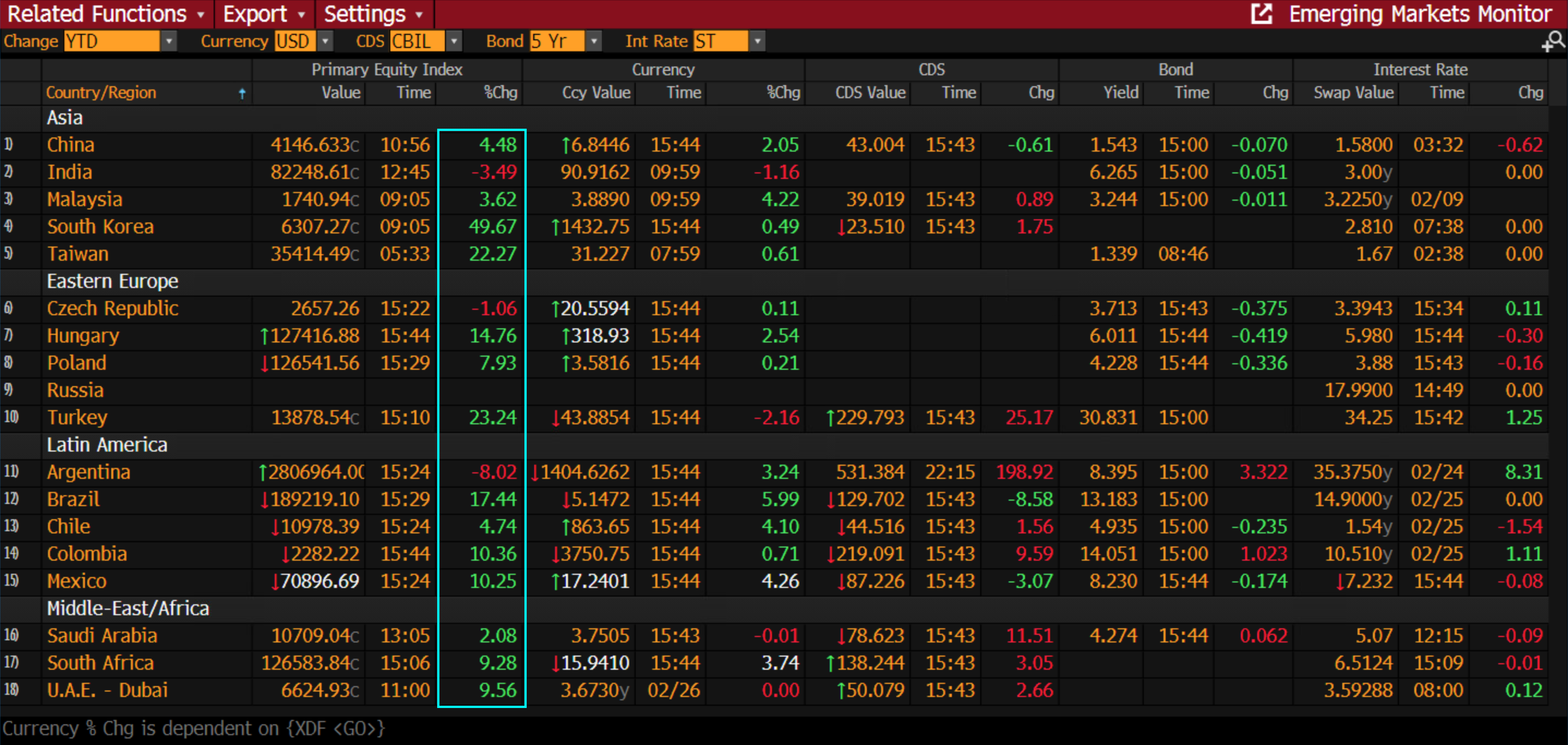

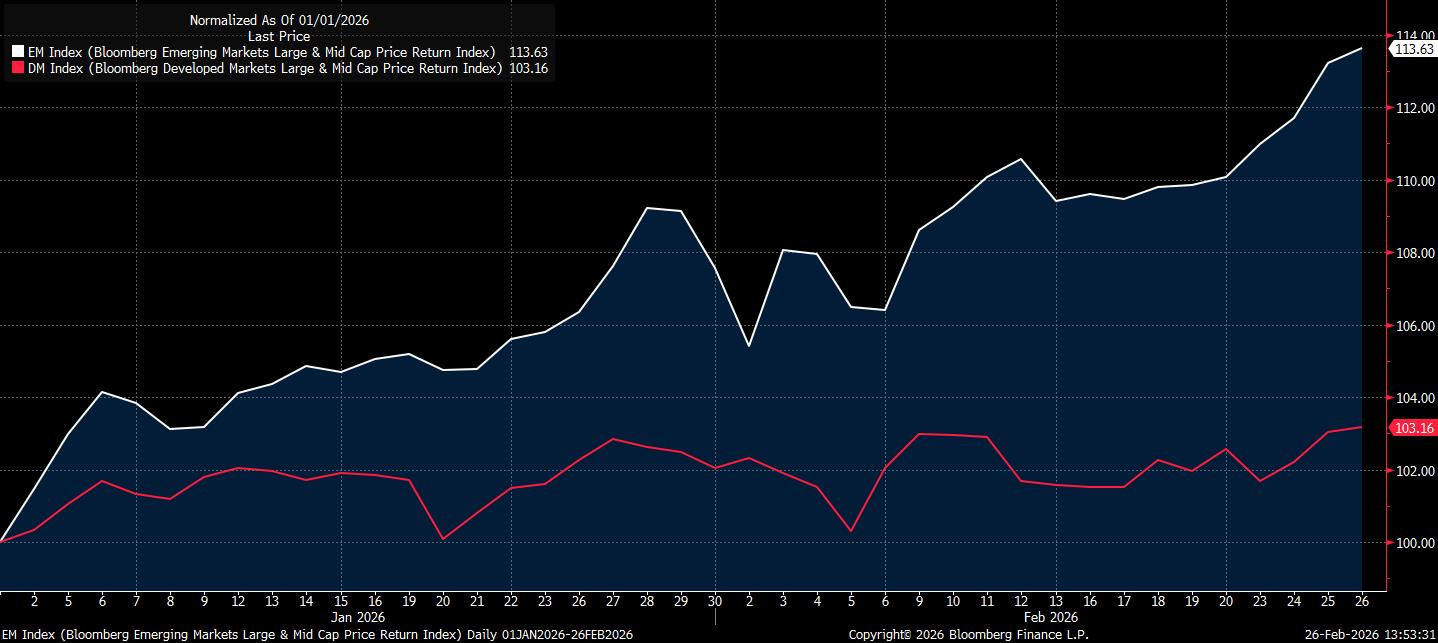

EM Bears Are Extinct

Emerging Markets have continued their standout start to 2026, and are worth a few comments as an update.

EMs started the year as a consensus trade, with money managers betting that a multi-year cycle of investment inflows is underway. Up 14% against DM’s 3% YTD return, it’s fair to say so far, so good on that bet.

The move reflects policy uncertainty and a widening US fiscal deficit that has prompted investors to diversify away from dollar exposure, while Japan and Germany have also increased spending, lifting yields across the board.

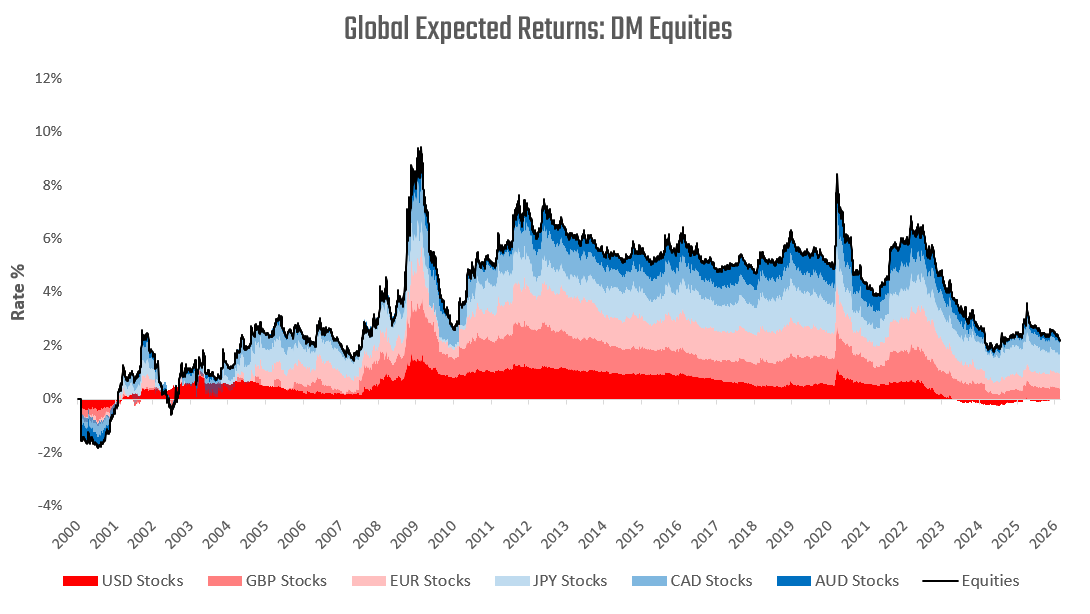

Consider also the chart below (courtesy of Prometheus Research). The excess returns relative to local cash rates for DM equities, while still positive, are well below more attractive historical levels.

“US equities have experienced a multi-year valuation expansion concentrated in a narrow group of high-growth, high-duration technology companies. As valuations rise, forward earnings yields compress mechanically, reducing embedded expected returns even if growth expectations remain strong.” — Prometheus Research

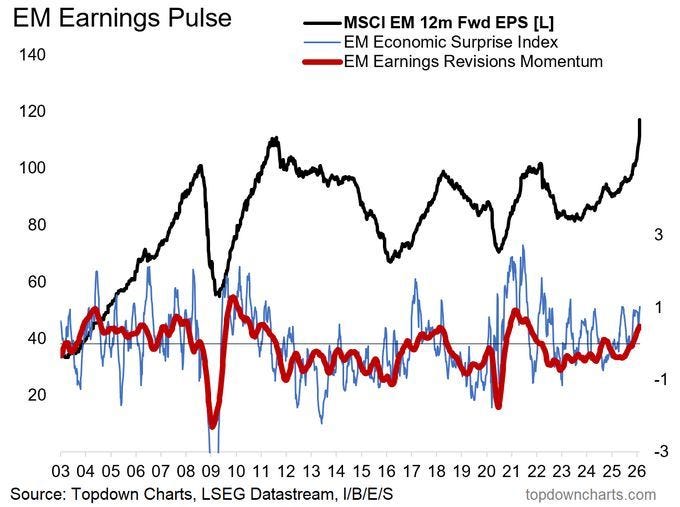

Central to the upside catalysts for EMs is earnings momentum. Profits are reviving, particularly in the emerging world, and there is solid confidence that this will continue. In such circumstances, the downside for markets is limited:

That wraps up our comments for today. With a busy, ever-changing week ahead of us, we’ll be active in the commentary and updates to our thinking, either through the Substack chat or via a few market memos.

AP

oh yeh? name all the happenings