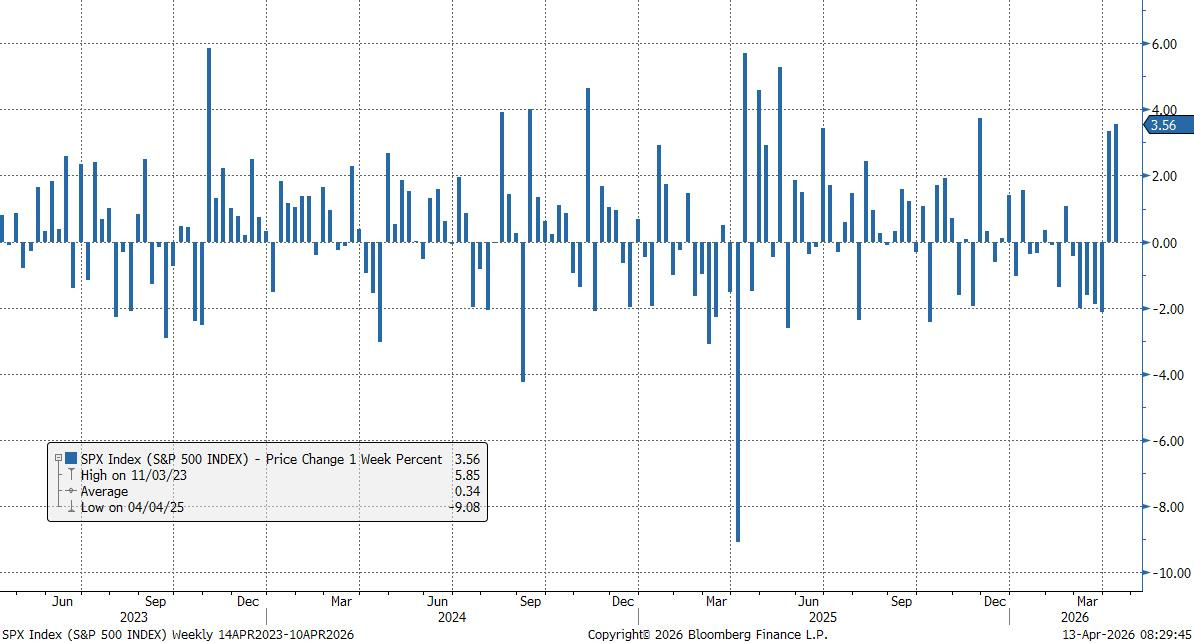

The S&P 500 posted its strongest weekly advance since November, but the tone of the move suggests relief rather than resolution. A tentative two-week ceasefire in the Middle East provided the catalyst for a sharp rebound in risk assets, yet the underlying drivers of the rally point more toward positioning and tactical flows than a durable shift in the macro backdrop.

The bulk of the gains were concentrated early in the week, as confirmation that the ceasefire was holding triggered a broad unwind of defensive positioning built during the height of the conflict. By Friday, momentum had already begun to stall ahead of scheduled US-Iran negotiations, underscoring how dependent the rally remains on incremental geopolitical progress. The price action continues to reflect a market that is trading headlines, with conviction fading as soon as the news flow turns less constructive.

Sector dynamics reinforce that interpretation. The Magnificent Seven reasserted leadership, with technology and communication services driving index-level gains, while semiconductors benefited from renewed optimism around AI-linked investment. Announcements from CoreWeave, alongside incremental demand signals from Meta, Anthropic, and Alphabet, provided a reminder that the capex cycle remains intact despite recent volatility. However, the divergence within tech remains notable. Software names continued to lag sharply as the latest wave of AI product releases revived disruption concerns, leaving the sector caught between structural growth and existential risk.

Macro signals continue to complicate the picture. Inflation data offered some near-term relief, with headline and core CPI both coming in slightly below expectations. However, forward-looking indicators paint a less benign picture. Elevated services inflation and a sharp rise in inflation expectations suggest that the second-round effects of the recent energy shock may still be ahead. At the same time, hawkish undertones in the FOMC minutes highlight that the bar for policy easing remains high, even as growth signals show signs of softening.

Across assets, the adjustment has been orderly but incomplete. The dollar weakened on the ceasefire news, retracing much of its year-to-date strength, though the persistence of a positive oil-dollar correlation points to a market still anchored in geopolitical dynamics. In rates, the move has been more muted, with the Treasury curve stabilising after an extended flattening phase. The lack of a meaningful rally in bonds, even as risk assets bounced, suggests that markets are not yet prepared to price a material shift in the policy outlook.

Taken together, last week’s rally looked like a release valve.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“No Deal to Back Up the Rally”

“Earnings Season Opens”

“From Missiles to Models”