The Banking Business Booms

U.S. banks set for boosted profits / CPI setup.

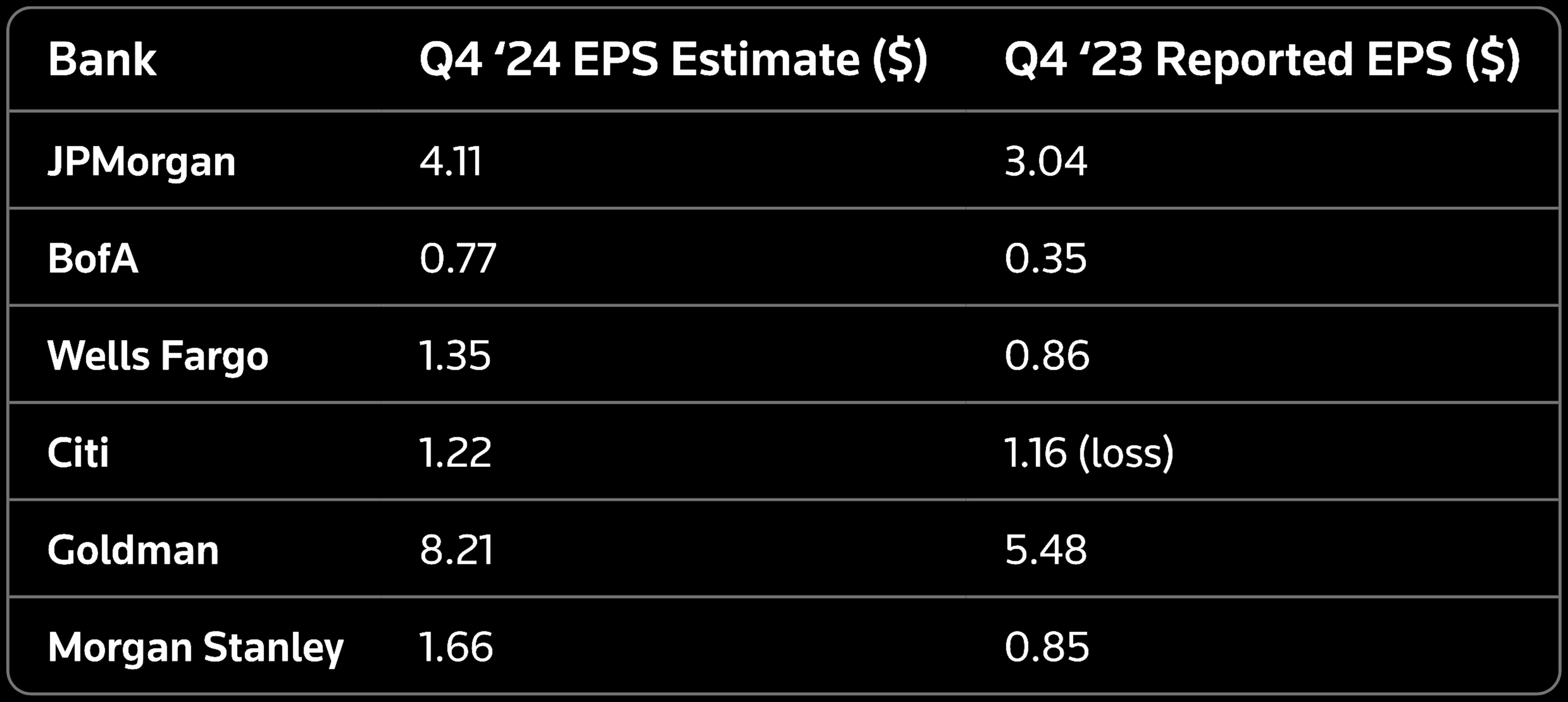

America’s biggest banks are set to post a jump in profits to $31bn for the final three months of 2024 as Donald Trump’s election victory sparked a jolt of trading activity on Wall Street, and dealmaking activity picked up.

Earnings projections for the six largest banks in the United States by assets—JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, Goldman Sachs, and Morgan Stanley—indicate a 16% increase compared to the same quarter of the previous year.

The anticipated surge in profits is attributed to increased market volatility leading up to the United States election on Nov. 5th, followed by a substantial rally in equity markets in the subsequent weeks. Citigroup and JPMorgan Chase reported late last year that elevated trading activity had significantly enhanced their revenue streams.

In regard to profit margins, banks are currently experiencing a Goldilocks situation. Financial institutions are benefiting from elevated rates at the long end of the yield curve while simultaneously managing to reduce deposit costs in response to the Federal Reserve’s rate cuts.

Investment banking fees are projected to have increased by nearly 30% for the major six banks, reaching approximately $8.4bn. This uptick can be attributed to corporate borrowers capitalising on a decline in interest rates during the autumn to issue debt. A buoyant stock market has stimulated additional equity offerings and a modest resurgence in mergers and acquisitions.

This period marked the most successful three-month span for investment bankers in three years.

Positive Prospects In 2025

We could note that these investment banking fees remain approximately 50% lower than the $13bn that the banks generated per quarter in 2021, a time characterised by a surge in deals amid the pandemic. With deregulations to come under the President-elect, there is plenty of room for these revenues to continue to grow in the year ahead.

Reduced regulatory requirements for banks themselves may allow them to take on more risk or boost shareholder payouts through buybacks or dividends, both of which would boost investor returns.

All these prospects mean the banks have a lot to deliver relative to expectations. Earnings may not be a problem this quarter, but they may serve as headwinds in future quarters.

Ahead of the earnings kick-off later today, we are positive about the Q1 outlook for bank performance, and with the inauguration just a few days away, there presents an opportunity for some upside returns for stocks, buoyed by optimism about the year to come.