Calmer Indices, Wilder Stocks

A weekly look at what matters and how to trade it. (July 13th)

SUMMARY:

- Takeaways from last week in cross-asset markets

- Thoughts and key considerations ahead of the upcoming week

- House views and expressions

A week of two halves, but the S&P 500 finished higher, as early-week geopolitical stress gave way to another late-week bid in technology.

Fresh attacks around the Strait of Hormuz and retaliatory US strikes in Iran briefly brought inflation concerns back into the conversation, pushing oil higher as a key inflation data print lies ahead this week. But equity markets proved more resilient than they looked at the start of the week, with dip buyers returning to semiconductors and communication services into Thursday and Friday.

Samsung’s disappointing earnings initially hit sentiment across the chip complex, weighing on Micron, Sandisk and the broader memory trade. That mattered because investors have become increasingly sensitive to any sign that expectations are running ahead of delivery. Yet the successful US debut of SK Hynix ADRs helped steady the sector, with the stock surging above its offering price after the largest-ever US listing by a foreign company. If Samsung provided the warning shot, SK Hynix provided the reassurance.

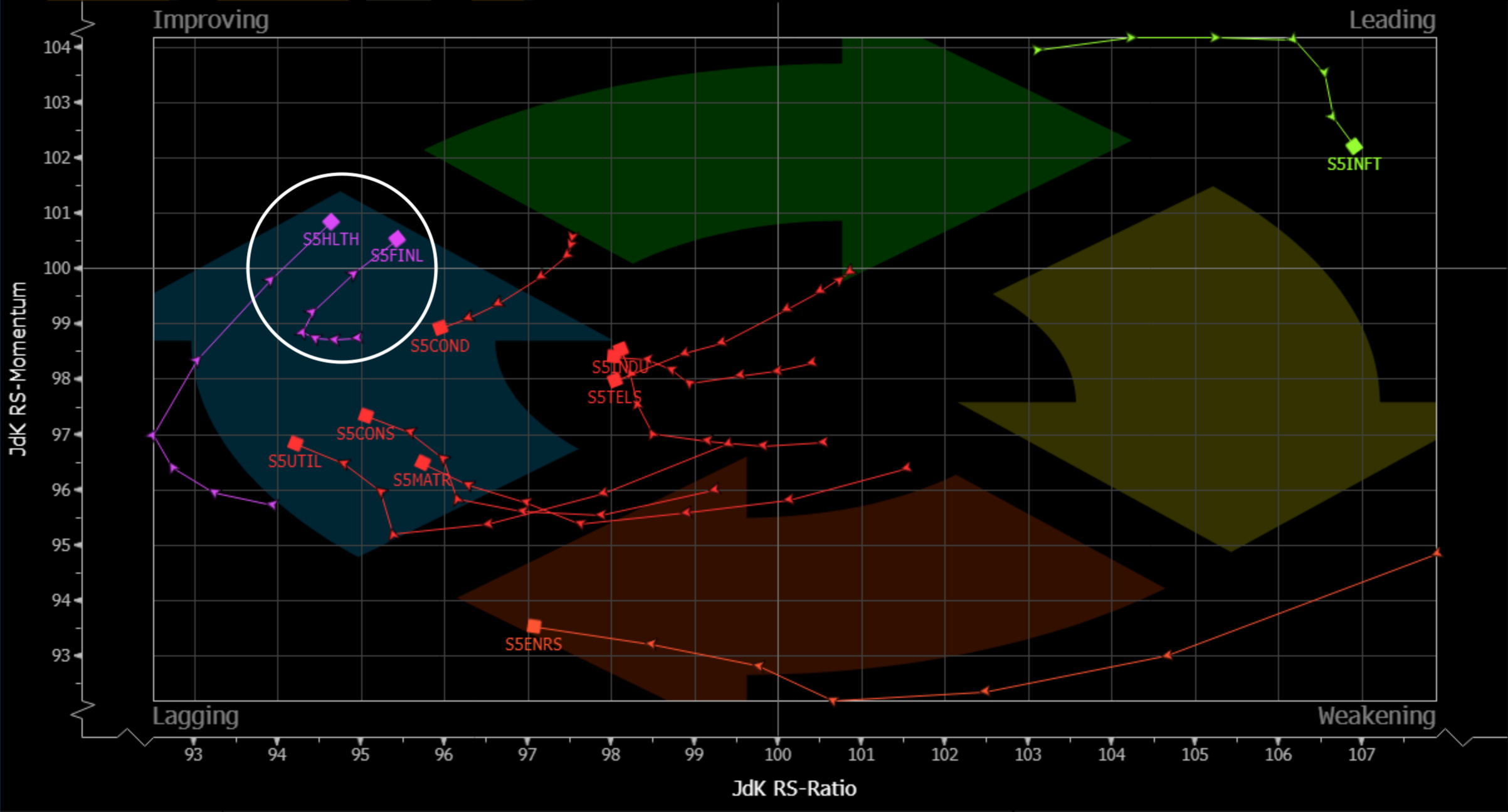

The sector rotation told a cleaner story than the index. Information technology, energy and communication services led, while materials, healthcare and staples lagged, marking a partial reversal of the recent defensive rotation, helped by evidence that the US consumer is not yet rolling over.

Macro was quiet, but not irrelevant. ISM Services was in line with expectations, and the employment component moved back into expansion for the first time since February. The FOMC minutes were uneventful, which may itself be a signal of the Warsh regime. The headline snapshot below is a great reminder that even in business economics, if you put two people in a room, you’re lucky to get only three opinions.

Rates reflected the oil move more than the data. Treasury yields rose across the curve as the ceasefire in Iran frayed, although demand at the 10-year and 30-year auctions remained strong. Real money still appears comfortable buying outright yield when levels are attractive, even as options activity suggests some investors are fading the remaining hike premium for later this year. The market is no longer in a simple “higher for longer” repricing, but it also is not ready to remove the inflation-risk premium while oil remains hostage to Middle East headlines.

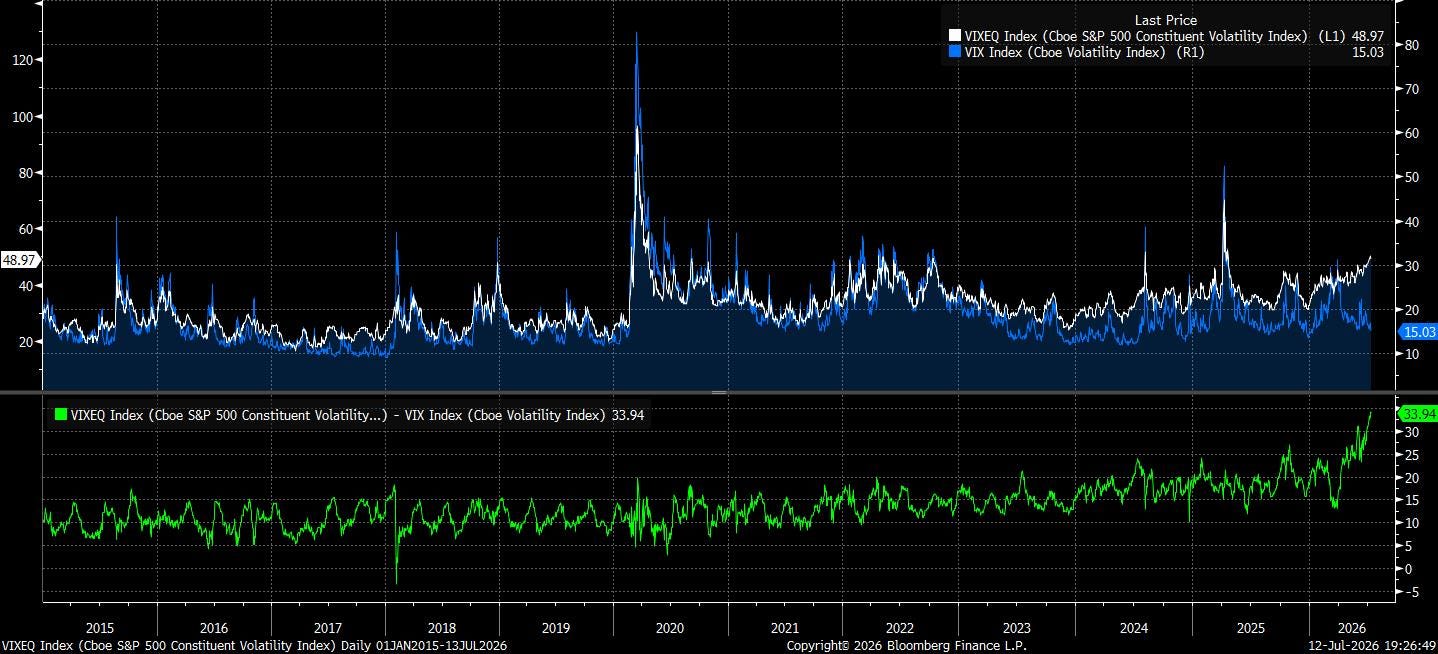

FX was quieter, though that may not last. The dollar was broadly flat, but low G10 FX volatility is starting to look vulnerable as the market becomes more data-dependent ahead of CPI, PPI, and the next Fed meeting. With forward guidance being pulled back, each inflation print has more power to reset the curve and the dollar. Low FX volatility has been driven by low market conviction, rather than low macroeconomic uncertainty.

Our macro desk explored this topic in further detail and outlined their preferred vol plays.

The takeaway from last week: the market remains supported, but the sources of support are narrowing and becoming more conditional… AI still has buyers, especially where scarcity is obvious… the consumer is still spending, but not evenly… the Fed is quieter, but not easier… and the Iran risk premium has not disappeared in certain markets, even if equities are less reactive to every headline than they were earlier in the conflict.

As earnings season begins, the market’s tolerance for disappointment is likely to be far lower at the single-stock level than at the index level. That is the next phase: calmer indices, wilder stocks.

Let’s get into the guide to trades moving markets, where things stand, and where they may be heading.

“Duration Rotation”

“Ahead of CPI…”

“Summary of House Views”

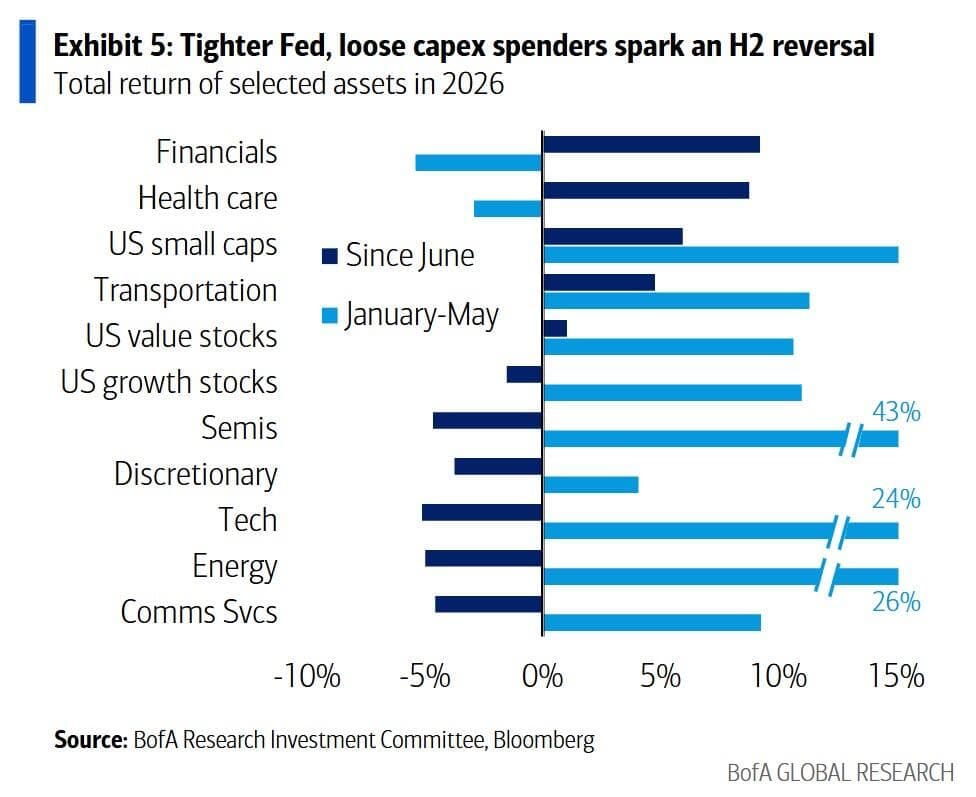

Duration Rotation

For much of the AI rally, time was treated as a free input. Investors were willing to pay today for earnings expected years into the future, confident that technological progress would eventually fill in the numbers. That bargain becomes less comfortable when the risk-free rate is rising, inflation is resurfacing, and oil is again helping to set the direction of bond yields.

This is the logic behind the emerging “duration rotation.” Equity duration is an imperfect concept, but a useful one. A company whose value depends heavily on distant cash flows is more sensitive to changes in the discount rate than one returning capital today. Technology, software, and other high-growth businesses sit at the long end of that spectrum. Banks, insurers, energy companies, and much of healthcare sit closer to the front.

The market recognises the difference. Semiconductors including Micron, Nvidia, Broadcom, and SanDisk have fallen sharply from recent highs, while banks, insurers, pharmaceutical companies, and healthcare stocks have assumed leadership. Since June, the broad pattern has been one of lower-duration sectors outperforming as higher-duration groups have lost momentum.