Contemplating Europe

ASML earnings, French equity recovery, and a US-China revenue L/S trade.

European equities have fallen lower this week, dragged down by luxury names. Weak economic data released from China and poor earnings results also helped lower the index. China’s GDP growth rate hit a five-quarter low due to underperformance in consumer spending despite efforts to stimulate it. Retail sales experienced their slowest growth since December 2022. Expectations are that China will contribute about 8% to European companies’ revenues in 2024.

Stoxx Europe 600 is down 185bps this week after a 240bps climb in the final three days of last week.

Among the individual market movers, Burberry’s stock declined significantly following the departure of its CEO and the luxury fashion brand’s decision to suspend dividend payments. Swatch also experienced a drop in its stock price due to declining sales and profit, reflecting the impact of a slowdown led by China. Luxury giant LVMH reports earnings on Tuesday. That will be a key indication for the sector to see if recent reports are outliers or if there is more concern to be had. More on that later.

While investors are trying to navigate recent indicators key for European markets, they also face an ECB rate decision on Thursday. While a rate cut has effectively been ruled out as policymakers take time to assess the strength of lingering inflation pressures, traders will closely watch for any clues offered by President Christine Lagarde on prospects for the September meeting.

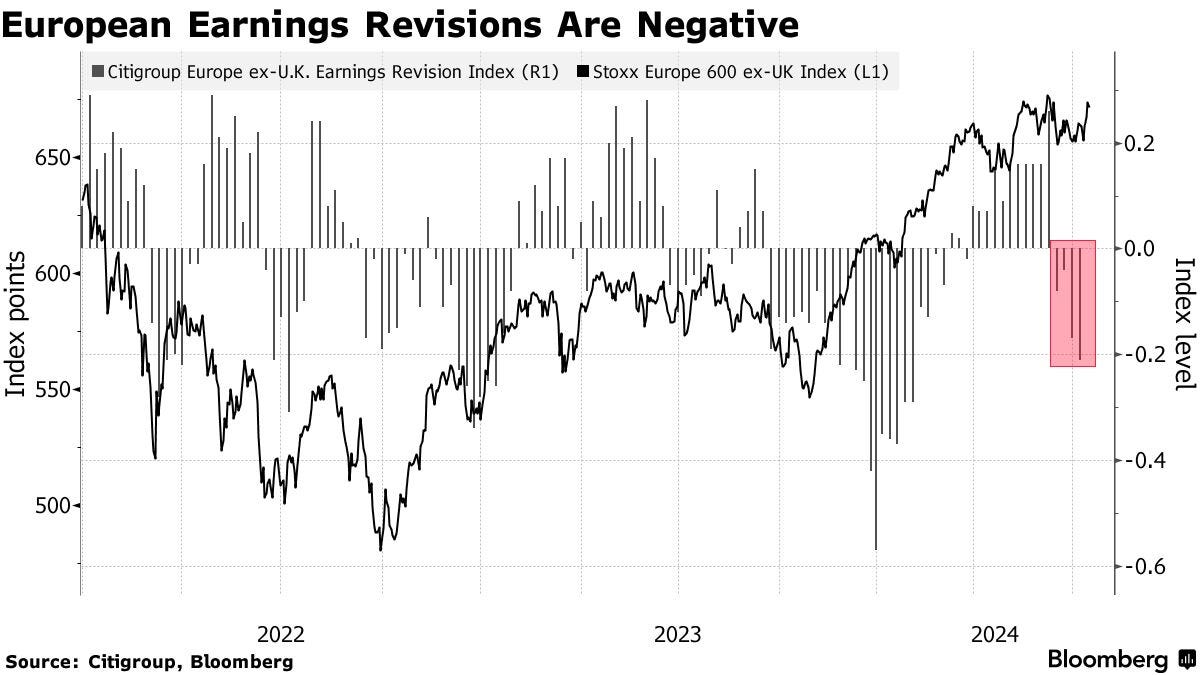

Still too soon to be overweight EZ

It may still be too early to be overweight in the euro area compared to the US. However, a combination of low expectations for the current reporting period and attractive valuations, particularly after recent declines triggered by French political uncertainty, leaves European stocks well-placed ahead of an expected pickup in earnings growth in the second half. There will likely be a better entry point to long euro names in the coming months.

In dollar terms, the Stoxx Europe 600 is lagging the S&P 500 this year by more than the average underperformance of nearly 8.5% since 2014.

A note on ASML earnings

ASML, the biggest tech company in Europe and the second biggest name, only behind Novo Nordisk, reported earnings this morning. The company beat second-quarter earnings forecasts as the world’s largest supplier of chipmaking equipment saw strong sales to China and a rise in new AI-driven bookings.

In his first results as CEO, Christophe Fouquet said ASML continues to view 2024 as a “transition year” with broadly flat performance as it prepares for a strong 2025.

“We currently see strong developments in AI, driving most of the industry recovery and growth, ahead of other market segments,” Fouquet said in a statement.

Net income of 1.6 billion euros ($1.74 billion) for the quarter ended June 30 was down 19% from a year earlier but beat the 1.41 billion expected by analysts. Revenue fell 9.5% to 6.2 billion euros but topped analyst estimates of 6.04 billion.

ASML dominates the market for lithography systems, complex tools that use lasers to help create the tiny circuitry of computer chips. Chinese chipmakers, however, face escalating US-led restrictions on ASML’s top-end gear. Instead, they have been ramping up purchases of equipment used to make older generations of chips widely used in cars and industrial applications. China accounted for 49% of ASML’s sales in the second quarter.

Bloomberg reported on Tuesday that the US is privately telling allies, including the Netherlands and Japan, that it may invoke the ‘Foreign Direct Product Rule’ to restrict products made using US technology unilaterally.

The geopolitical aspect of ASML is the focus of today’s headlines, with the stock price down 4.7% as of 8:46 BST.

Long US revenues, short China revenues

Poor spending appetite in China, the country’s intention to tax luxury goods and the likelihood that Beijing will retaliate against the European Union’s tariff hike on electric-vehicle imports are all weighing on China-dependent European stocks, the standout name being LVMH.