At President Trump’s address to the nation on Wednesday, the defining feature was the absence of a coherent endgame. Despite repeated claims that the war is “nearing completion,” Trump declined to provide any clear timeline, criteria for victory, or framework for de-escalation.

This provided another Jenga-style piece removal of security with which the US economy is currently being propped up. The ongoing conflict in Iran is causing some to increase their probability of a recession. Although we wouldn’t position ourselves in the eternal optimists bucket, we believe there are several reasons why it’s still far too premature to start throwing around the R-word.

Things Are Different From 2022

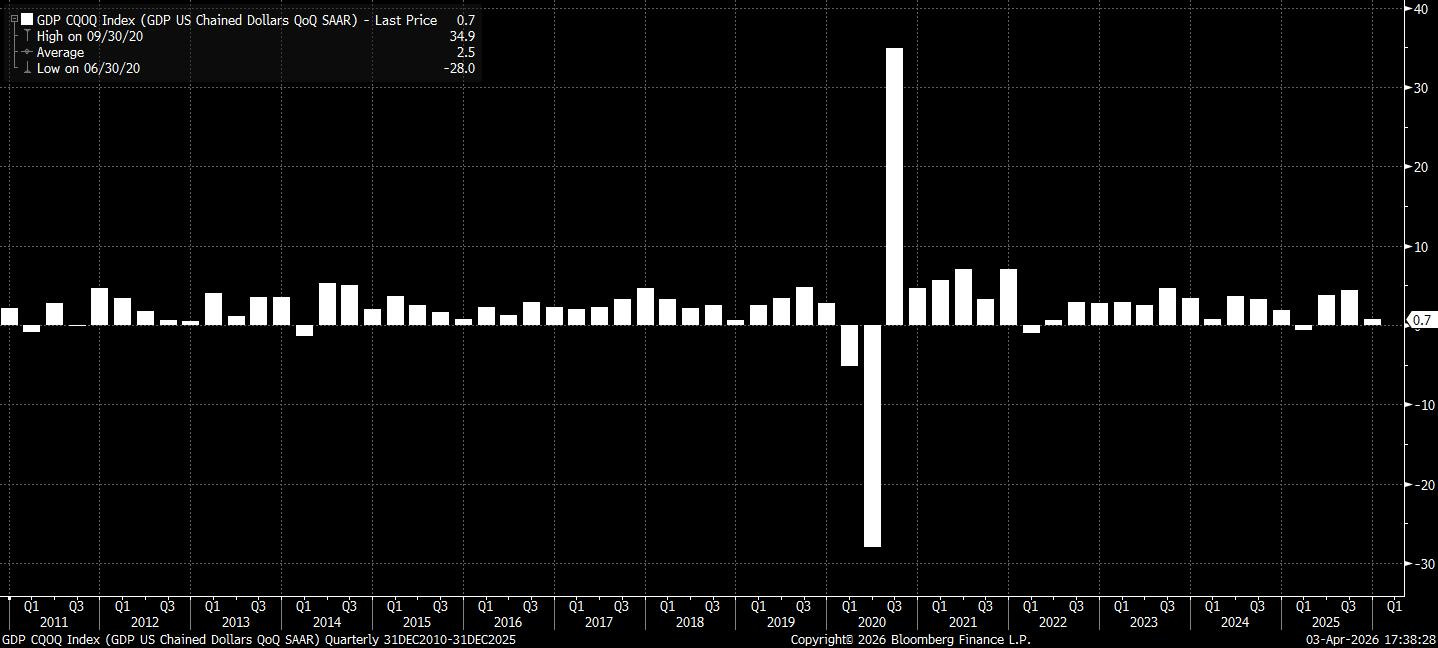

Ok, technically, the last official US recession was in 2020. However, US GDP in the first two quarters of 2022 almost triggered a technical recession and provides us with the most recent blueprint to compare to. It’s also a relevant comparison due to surface similarities around an energy shock and geopolitical uncertainty from the start of the Russia-Ukraine conflict.

However, on reflection, the current macro backdrop differs materially from the 2022 recession template. Most importantly, the inflation dynamic is far less entrenched today. In 2022, economies experienced a shock as accelerating wage growth and tight labour markets emerged from the Covid pandemic, creating the conditions for a wage–price spiral. By contrast, wage growth is now moderating and labour market sentiment has softened significantly, reducing the risk of persistent inflation and pointing instead toward a more disinflationary or even deflationary impulse.

Policy settings also start from a fundamentally different place. Central banks entered 2022 well behind the curve, with rates deeply below neutral and forced into aggressive catch-up tightening (Powell might never live down his “transitory” comment from that time). Today, policy rates are already closer to neutral, with the Fed well into its easing cycle.

Finally, the labour and technology backdrop introduces a new asymmetry. Whereas 2022 was defined by labour scarcity, today’s environment is increasingly shaped by concerns around AI-driven labour displacement, contributing to weaker employment expectations and dampening wage pressures. Taken together, the current cycle lacks the key ingredients that drove the stagflationary shock in 2022.

Granted, this doesn’t excuse the worries about US vulnerability to growth downside, but it’s unlikely to result from a 2022 repeat of persistent inflation.

Current Indicators

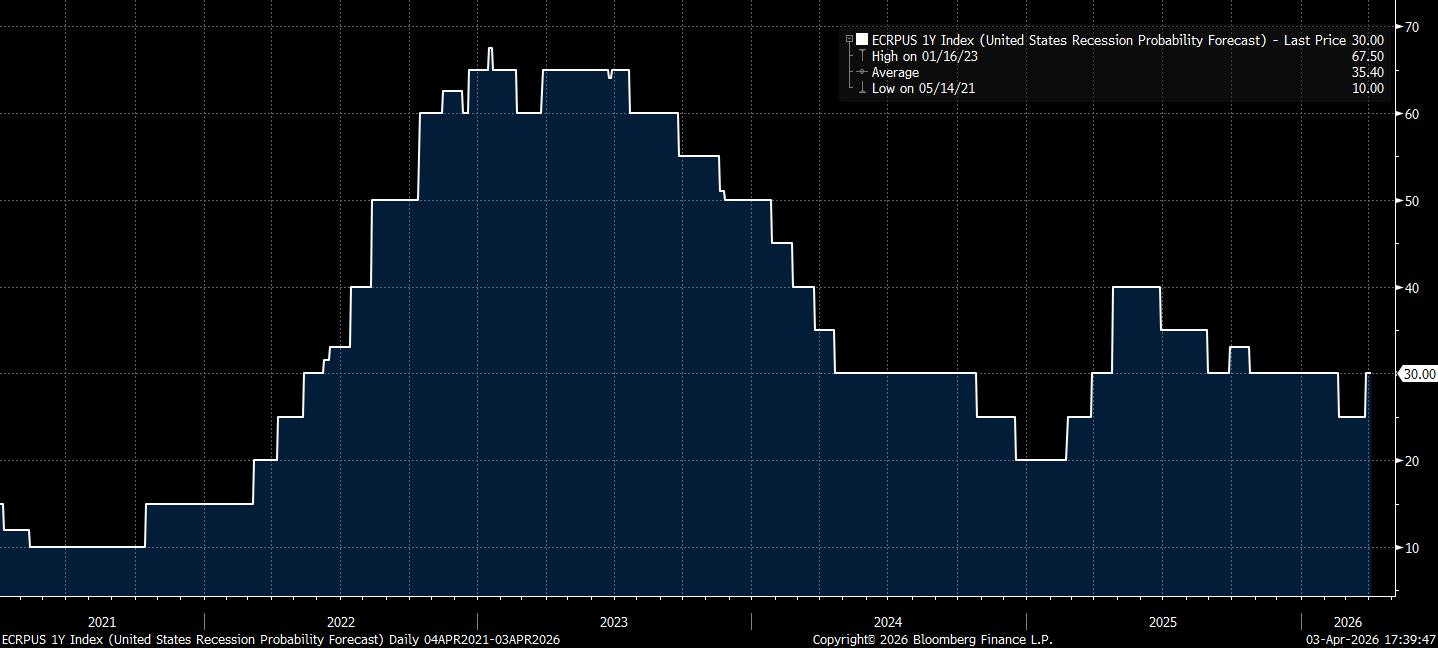

There’s no exact science in determining which metric is the best when trying to predict a recession. Yet even if we take a spread of some of the most widely used or vouched-for, the probability still appears to lack any significance:

Bloomberg median forecasted probability of recession in 2026 (%):