Final Quarter Themes & Ideas

Market musings on upcoming and ongoing events.

If you’re from the UK or have ever spent time here, you’ll know the feeling of days quickly getting shorter as we approach the final months of the year. The odd sunny days come by and give a false sense of optimism that they will stay, only for us to be let down as the afternoon showers approach and the grey clouds reemerge.

Alongside the seasonal changes underway are the events at play in the markets that traders and investors will have to navigate over the coming quarter (yes, we had to bring the conversation back around to finance. Apologies if you would have preferred some autumnal writing from the AP team). Middle East tensions are on the rise, global monetary policy has shifted into its next chapter, and elections—with their subsequent volatility—are rapidly approaching.

It feels right to share some musings on global assets and suggest some ideas and themes that the team will be following over the coming months. Geopolitical positioning, pain trades, currency shifts and stock picking are on the agenda.

To access full articles and research, manage your account here.

GeoPol

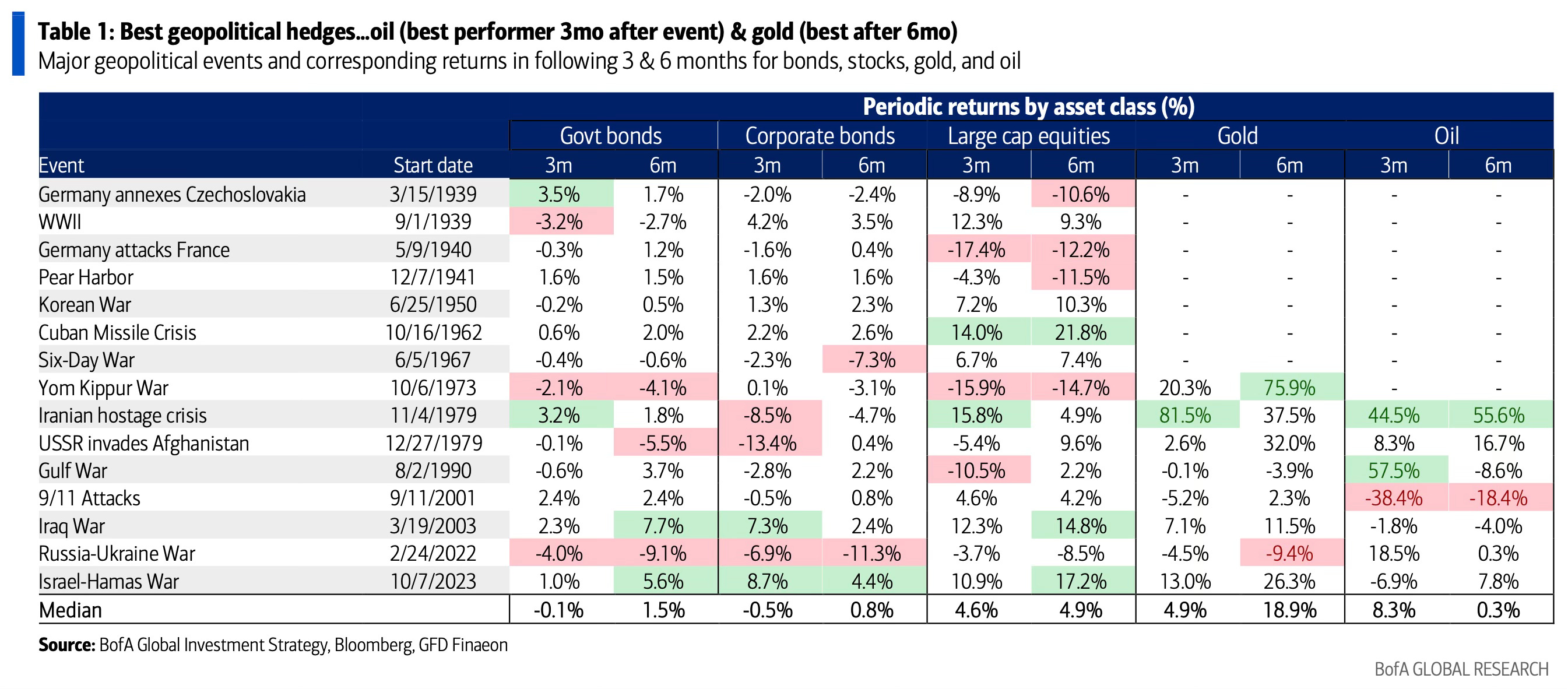

Investors are getting long oil. That’s understandable. Oil and gold often serve as geopolitical hedges. In fact, across different asset classes, oil has the highest three-month return, averaging 8.3% over the last seven major conflict outbreaks.

For the time being, at least, current geopolitical risks aren’t having a significant impact on global growth. So, the positive macro data outweighs the impact and pushes risk assets higher. Knee-jerk reactions lower have been buyable dips across many conflict outbreaks. Monetary and fiscal policy will counteract any adverse impact on consumer and business sentiment. U.S. markets’ high exposure to the technology and defence sectors, along with its energy independence (unlike Europe and Asia), is another reason why they tend to be unaffected by conflicts.

Because of their heavier reliance on energy elsewhere, European and Asian markets feel the hit of rising oil prices more than their counterparts across the pond. That means international equities serve as the biggest relative winners from lower geopolitical risk premia. Keep that in mind over the coming months.

Takeaway: Oil can rally if conflicts persist (note that prior to the escalation, we were bearish), but it won’t serve as a headwind for risk assets.