FX: It's Likely To Be A Hot Summer For The Carry Trade

With USD rate pricing looking close to terminal levels, we like a carry trade but not the one you might think.

2022 was characterised by a stronger USD / higher US rates

Terminal pricing in the US likely to be reached this summer

Shorting USD in favour of EM high-yielders could offer attractive returns

Most in the market are constantly monitoring the implied interest rates for G10 central banks. From this, the repricing of expectations from data releases is causing appreciation/depreciation in the respective currency.

We feel that this is becoming a rather narrow-minded attitude and that the smart money is moving towards the second derivative of this thinking: carry trade opportunities.

The carry trade explained

A carry trade in the FX market seeks to take advantage of interest rate differentials. It involves selling the lower-yielding currency and buying the higher-yielding one.

Over a period of time, the interest rate differential provides a ‘risk-free’ profit to the investor. Combining this with the higher-yielding currency appreciating in value, the FX trade becomes a win-win. Even if the FX rate remains rangebound, the investor can still come out with a net profit.

USD: the King of carry in 2022

Over the past year, the focus has been on the US Fed leading the way in terms of rate hikes and expectations for more going forward.

This created a golden carry trade when buying USD against other currencies that weren’t on the same monetary policy path.

A great example of this was USD/JPY. Below, the chart shows the spot performance versus the differential between the UST 2yr Yield and the comparative JGB.

The correlation was very strong, and as investors benefitted from the carry either from holding cash or by putting on the spread trade via the bond market, they also made gains from the currency appreciation.

Granted, all carry trades over a calendar year don’t work out as perfectly as USD/JPY did last year, but it’s not a distant fairytale.

Things will be different this year

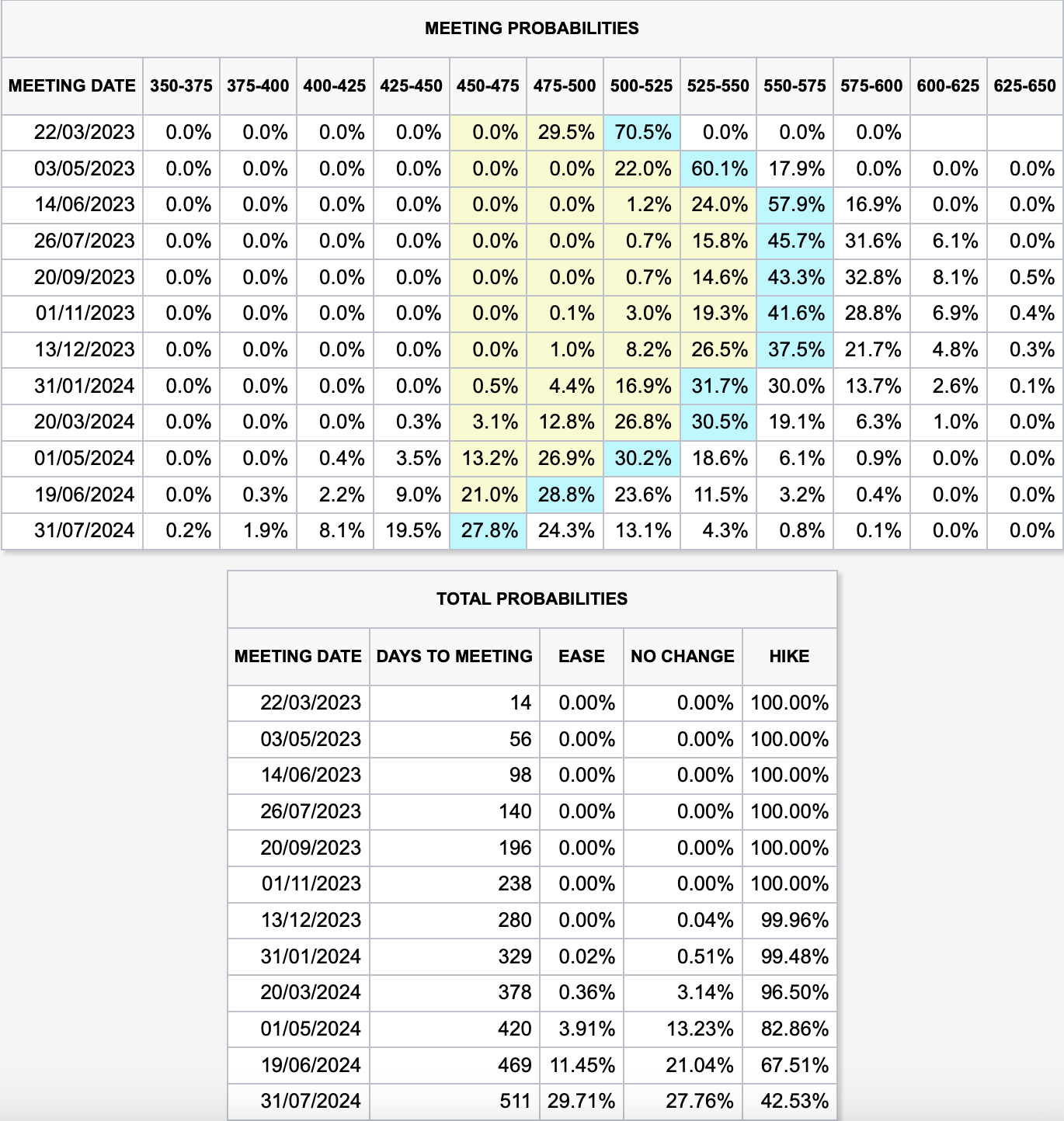

Is there still time to buy USD for a carry trade? Technically yes, but the days of this idea are numbered. The reason for this is that we think the US will reach a terminal rate by the summer. From this point onwards, we see limited potential for this to shift higher, with it likely going to stay around the 5.50-5.75% banding through to the end of the year. Market probabilities supporting this are shown below (data as of Wednesday):

On the other hand, there are a host of nations that are still behind the curve, certainly when compared to the US. So the potential for the inverse of 2022 performance is very high.

Isn’t this already priced in? We don’t think so. For example, we like being long EUR as we feel there is plenty of room for terminal pricing (currently at circa 4%) to move higher in the coming months (towards 4.50%).

Absolute versus relative carry

But we can sense what you’re thinking. If we take a neutral view and assume a 5.75% rate for the US, doesn’t it still make sense to buy USD and sell JPY this year? No.

At an absolute level, you’ll still pick up a positive carry on the interest rates. But this could all be eroded by the FX movements. This is because, at a relative level, the carry is shrinking.

We widely expect the Japanese to abandon yield curve control later this spring when the new Governor takes control. As a result, we feel the US-JAP differential will shrink rapidly, with JPY strength into the summer.

Therefore, we think it will be a hot summer for the carry trade, but not as you might assume.

The carry trades for the summer

Our play is to short USD in the coming months, with the aim that that leg of the trade will either have neutral rate pricing or even move slightly lower.

On the long end of the trade, we like to look to the EM space, for example, BRL.

The below chart shows that the USD/BRL carry has shrunk in recent months but is still at a very healthy level of 9%. If we combine this with our view of a weaker USD as rates peak, the benefit of a win-win from both the rate pick-up and the FX movement could be significant.

Again, we stress that we prefer to play this with USD on the short side, more so than traditional low-yielders. Shorting JPY or CHF doesn’t sit well with us, and we’re happy to sacrifice some of the carry here to have our short USD thesis on the table.

The usual disclaimer

Getting long on emerging market currency carries an elevated level of risk. Interest rates may be high, but that isn’t stopping the Turkish Lira from getting pounded. Being selective on where to target is key. We like Brazil structurally (DM us if you want more reasoning), but there are other places to find value as well.

theeditor@alphapicks.co.uk

Our Twitter account posts quick, informative tweets and data throughout the week. We also join live trading spaces, which you can listen to. So please drop us a follow and turn notifications on to stay up to date.