High Fashion, Low Conviction

Why we're still sitting on our hands.

Last summer, we wrote about Luxury’s Problematic Pricing, flagging how focusing on attracting an ultra-wealthy clientele has caused a problem: the neglect of the middle class, a significant revenue generator.

As it turns out, this was only one of the problems that have shaken the luxury space. Earnings this week from giants LVMH and Hermès helped to paint a more detailed picture of the issues experienced in the sector in recent months.

But with LVMH stock down almost 40% in a year and luxury index benchmarks down double-digits, more reasonable valuations are causing some fund managers to conclude that we’re close to the bottom for some luxury names.

“2025 has started off with a bit of turbulence”

At the company’s AGM meeting on Thursday, CEO Bernard Arnault commented on the rocky road to begin the year.

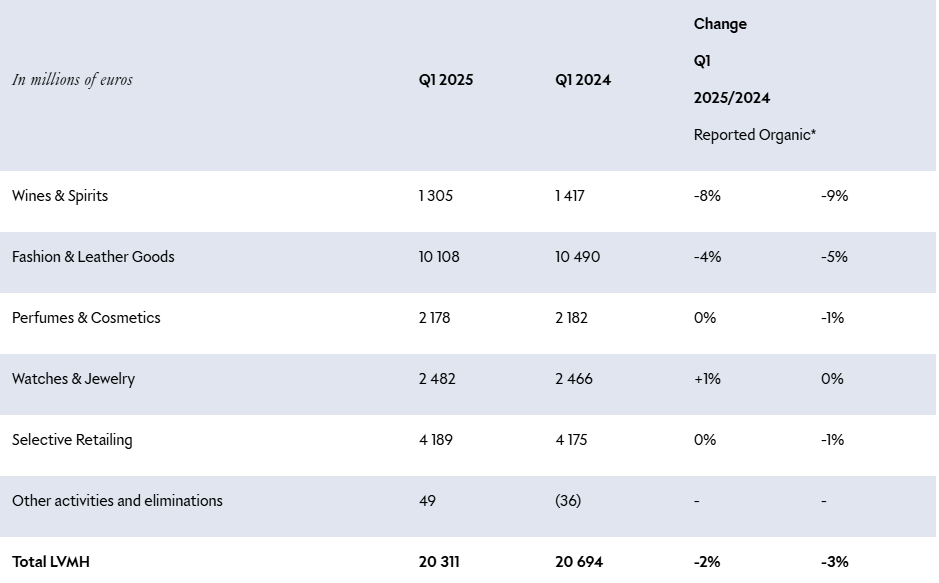

The business posted a 3% decline in revenue to €20.3 billion, missing analyst expectations of a 2% increase. At a product level, sales in fashion and leather goods, which include brands like Louis Vuitton and Dior, fell by 5%. Dior was notably impacted by slower creative transitions. At a regional level, sales in Asia (ex Japan) dropped 11%, while the U.S. market saw a 3% decline.

In wine and spirits, the division experienced a 9% decrease in sales, attributed to weaker demand in both the U.S. and China.

One key factor raised by Arnault was the economic uncertainty and pending impact of tarrifs, which he belives weighed on demand during the quarter. This was also flagged by Hermès, with the CFO noting that prices in the US will increase as of the start of May in order to fully compensate the impact of the new tariffs on the EU. Interestingly, he said the company hasn’t noticed a perceptible change in US demand trends in April.

Let’s face it, if tariffs do go ahead, both firms will be negatively impacted, although you can argue that glum investors have priced in this worst-case scenario in recent weeks.

The exposure is non-trivial. Over 20% of revenue for both companies comes from the U.S., while most production remains France-based. This isn’t just about finished goods crossing borders. Supply chains are global (exotic leathers, custom hardware, branded packaging), and tariffs can bleed into cost structures long before the product hits the shelf.

Chinese Slowdown

Both companies saw a slowdown in Asia. This region (including China) accounts for 48% of global sales for Hermès, and 30% for LVMH.

Chinese consumers have pulled back. Store traffic is lighter, and conversion rates are lower. A weaker property market, a higher benchmark comparison YoY, and rising pricing uncertainty tied to U.S. tariffs all contributed. But the downtrend didn’t start in Q1 2025. As Bain’s recent chart shows, this has been building since 2024. Tariff risk just accelerated what was already in motion.

That said, context matters.

Chinese luxury spending hasn’t disappeared—it’s been displaced. As travel restrictions eased, more consumers began shopping abroad. Price differentials between regions, particularly Japan, have pulled spending out of mainland stores and into duty-free zones and boutiques abroad. Domestic weakness doesn’t always mean global demand is falling. It can just mean it’s moved.

This is a key point to note especially when taking a high level view of if we’re close to a bottom for the sector. Hermès’ overall sales for the quarter rose by 7.2% YoY. This was not an earnings release that saw global demand fall. Hermès sales actually grew in all regions, DESPITE a slowdown in China.