Lean Mass, Fat Margins

GLP-1s are reshaping medicine.

GLP-1s have moved fast. In just two years, they’ve gone from specialist prescriptions to dinner party conversation.

Ozempic and Wegovy aren’t just drugs; they’re cultural phenomena, reshaping everything from pharma earnings to airline baggage loads. But while the market is still digesting their potential, the clinical picture is starting to evolve.

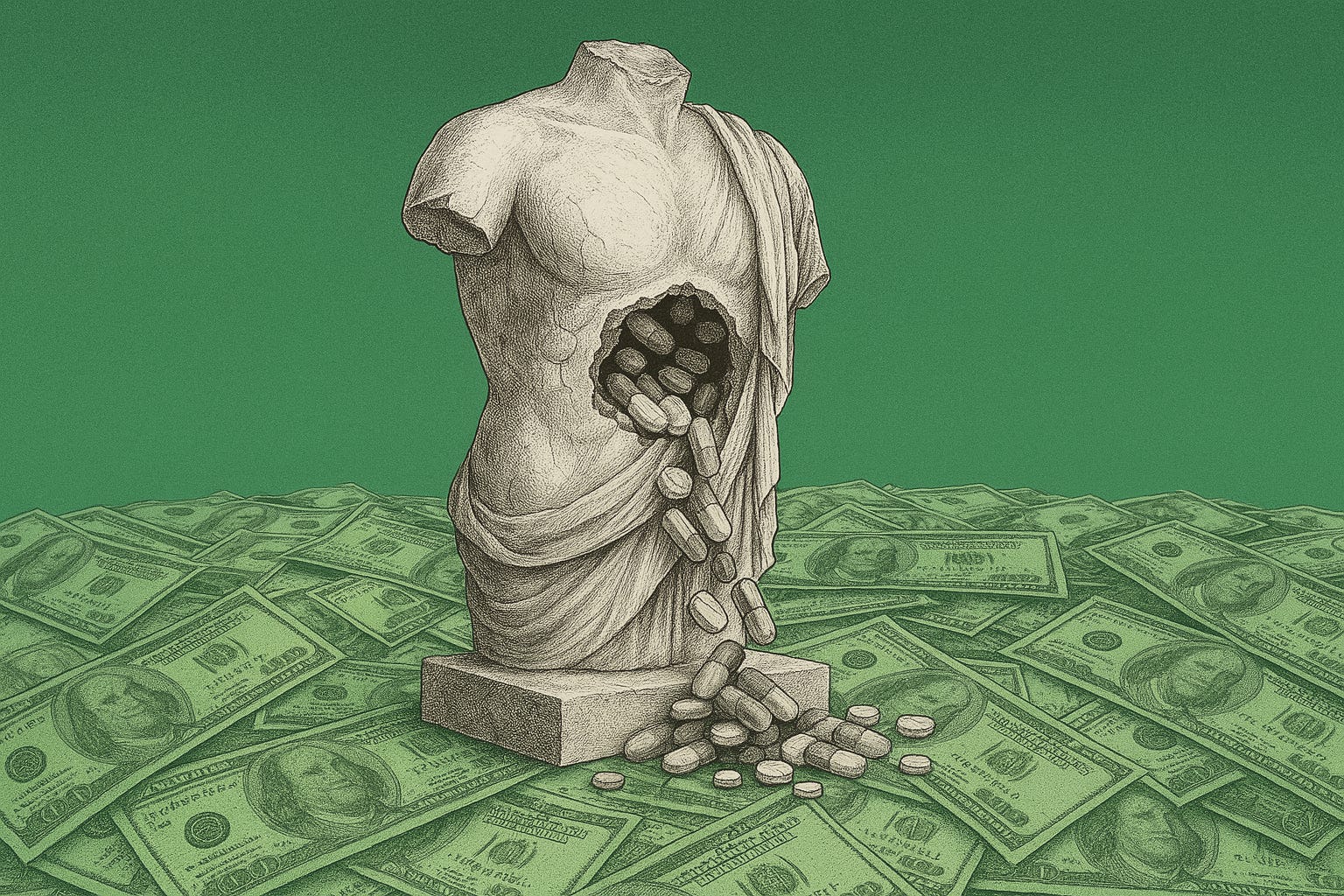

The drugs work—dramatically so. But they don’t just trim fat. They cut muscle, too. Quietly, that tradeoff is becoming one of the most important questions in obesity medicine: can we get the weight loss without sacrificing strength, function, or long-term health?

That question is spawning a new leg of the GLP-1 trade. A handful of companies are now targeting the muscle-preservation problem directly, aiming to pair GLP-1s with agents that protect or even promote lean muscle growth. It’s early, but the implications are large. This may be where the real differentiation begins and where the next round of alpha emerges.

The Rise of GLP-1s

In just a few short years, GLP-1 receptor agonists have transformed from niche diabetes treatments into the defining pharmaceutical category of the decade. Drugs like Ozempic, Wegovy, and Zepbound are not just tools to manage obesity, but economic juggernauts, driving hundreds of billions in market capitalisation and reshaping public health narratives in the process.

The mechanisms are well understood: appetite suppression, slowed gastric emptying, improved glycemic control. For patients, the results are nothing short of dramatic. Sustained weight loss north of 15–20% is now achievable with pharmacological support alone, numbers once thought impossible without surgery.

Capital markets have responded accordingly. Novo Nordisk and Eli Lilly have become the new royalty of global pharma. Yet this surge in efficacy has brought with it an unintended side effect, and it may shape the next frontier of obesity drug development.

The Hidden Cost: Muscle Loss and the Road to Muscle-Preserving Obesity Therapies

Beneath the excitement, clinicians and researchers have flagged a consistent concern: GLP-1 therapies do not discriminate between fat and lean tissue. Studies show that up to 40% of weight lost on these drugs can come from lean mass—particularly troubling given muscle’s role in metabolic health, physical function, and ageing.

Enter the next phase: therapies designed not just to induce weight loss, but to do so while preserving or even increasing muscle mass. Recent trials, such as the ECO 2025 study, suggest that pairing GLP-1/GIP agonists like tirzepatide with resistance training and adequate protein can mitigate some of this loss. But pharmaceutical companies are now moving toward a more aggressive solution: combining GLP-1s with agents that directly preserve or enhance muscle.

Leading that charge are myostatin inhibitors, biologics that block the protein responsible for limiting muscle growth. In preclinical trials, agents like bimagrumab and trevogrumab have shown potential to not only halt muscle loss but reverse it. If GLP-1s were the first revolution in weight loss, these combination therapies may spark the second.

The stakes are high: the obesity drug market is projected to exceed $130bn by 2030. And as the efficacy bar rises, so too does the complexity of what “best-in-class” really means.

The Fall of Regeneron

It’s against this backdrop that Regeneron finds itself at a critical juncture. Once a biotech darling with a pristine track record and deep R&D bench, Regeneron’s stock was down almost 60% from recent highs—a correction unmatched in the company’s history.

The market’s concerns are understandable. Eylea, Regeneron’s flagship anti-VEGF therapy, is facing biosimilar competition and a slower-than-expected ramp in its high-dose formulation, Eylea HD. The FDA’s complete response letters delayed its rollout, causing confusion around sales trajectories and sparking investor flight.

Meanwhile, the company suffered a high-profile Phase 3 failure with itepekimab in COPD, losing 18% in a single session. Combine that with a broader biopharma sell-off, concerns over US drug pricing policy, and the rise of GLP-1-driven narratives elsewhere, and you have the perfect storm.

But the drawdown may be deceiving.

The Case for a Regeneron Revival

For those willing to look beyond the headlines, Regeneron’s foundation is as strong as ever. Dupixent, its IL-4/IL-13 blockbuster with Sanofi, is now the fourth-best-selling drug in the world, with 2024 revenues of $14bn and more growth ahead. Libtayo has crossed blockbuster status, and the company remains a leader in immuno-oncology innovation.