Really, this week was all about macro: CPI and Kevin Warsh’s two-day testimony. With one behind us and one at half-time, we thought it best to step back from our incoming primer on equity issuance and realign our views and convictions with the latest data we have.

The Federal Reserve’s credibility problem has rarely been about finding the right words. Central bankers have no shortage of those (although if Warsh has set a precedent, he’d like to have less in the future). The harder task is convincing markets that the words describe a reaction function rather than a pre-committed strategy.

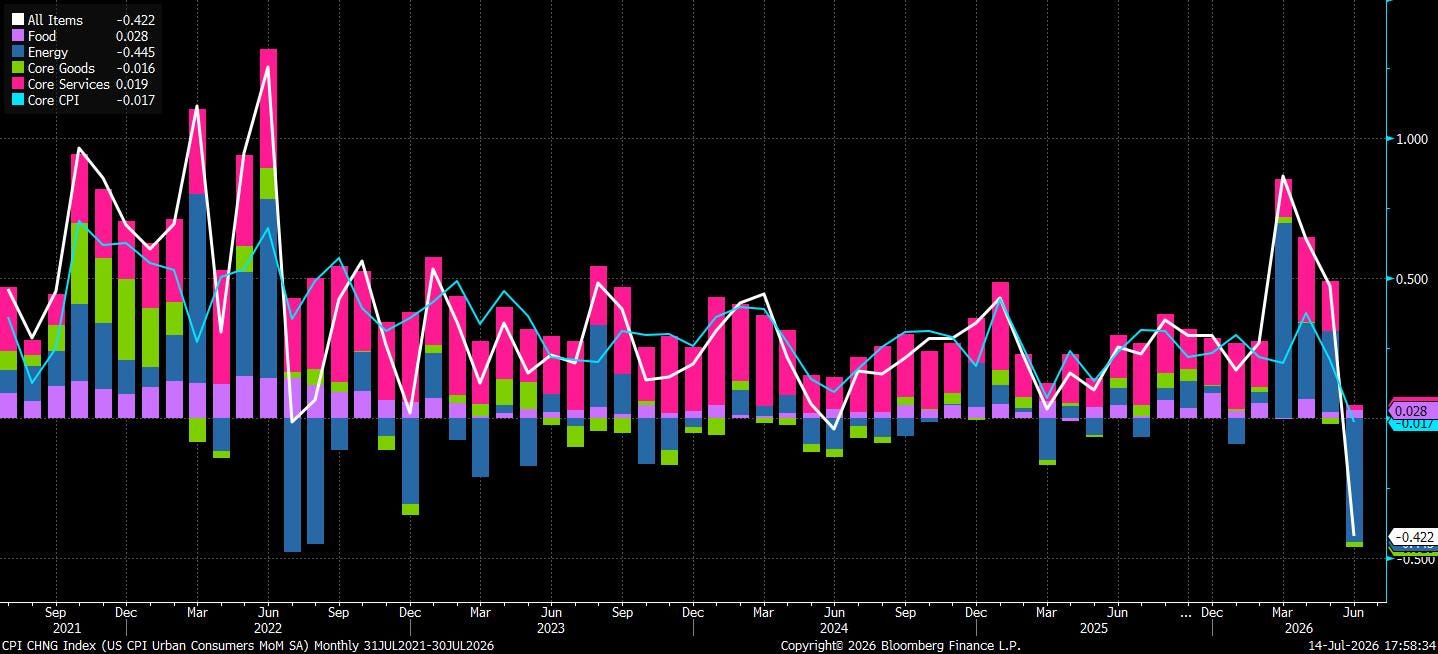

Warsh entered his congressional testimony insisting that the Fed has “no tolerance” for persistently elevated inflation. Had the CPI report landed hot, that language would have been perceived as a threat to markets, with an appropriate hawkish extension of recent moves to follow. Instead, those words arrived alongside the weakest inflation print since 2020. Headline prices fell 0.4% month-on-month against expectations for a 0.1% decline, while core CPI was unchanged rather than rising the expected 0.2%. Annual core inflation slowed to 2.6%, undershooting the 2.8% consensus.

Warsh did not have to demonstrate his inflation credentials by delivering an immediate rate hike. The data has done some of the work for him. In that sense, the credibility question received a favourable answer. Warsh can continue to present the Fed as intolerant of inflation without forcing policy tighter into a cooling price backdrop. His rhetoric looks more like a framework that is producing the desired outcome.

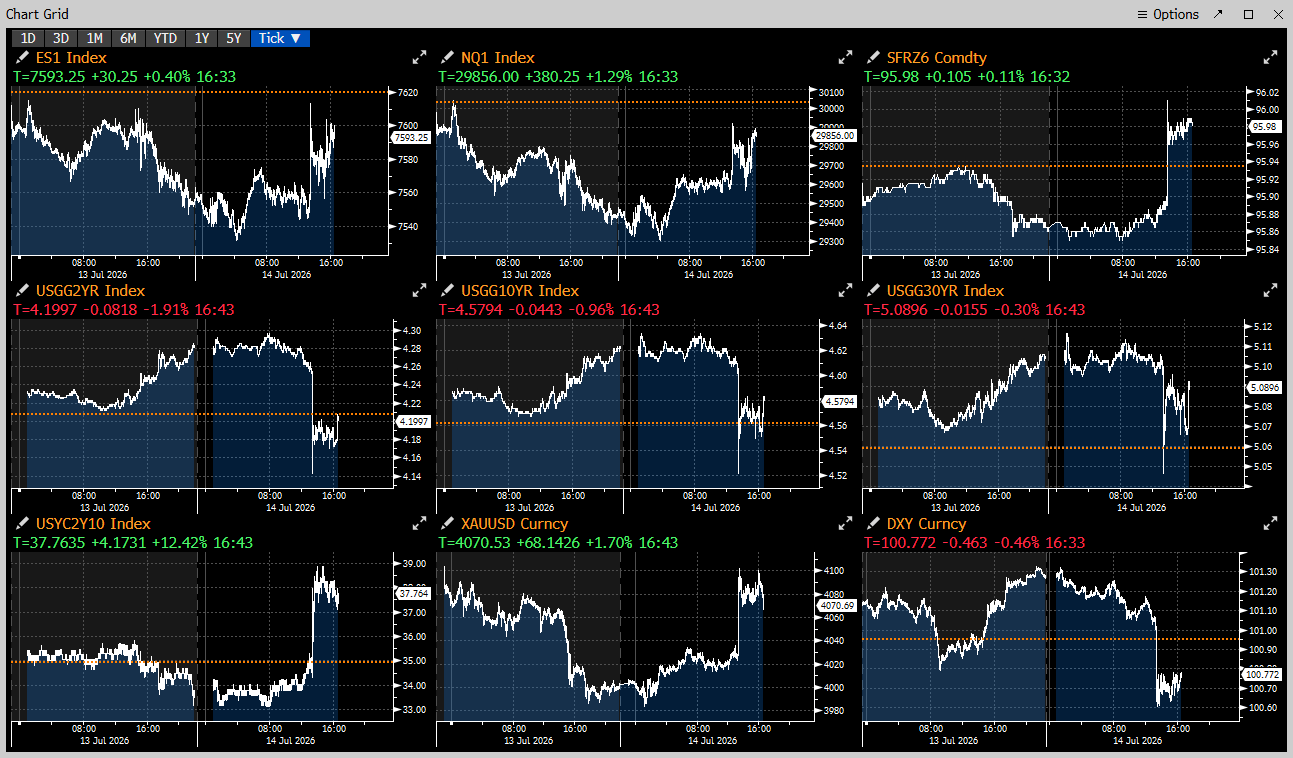

The two-year Treasury yield fell about 10bps, July hike pricing fell back, and the expected timing of the next move was pushed back towards the autumn.

The most effective inflation hawk is sometimes the one who does not need to hike. If households and companies believe the central bank will respond when necessary, inflation expectations can moderate before the response itself arrives. The “Maradona theory of interest rates,” as Mervyn King once said. Tuesday’s report therefore strengthened Warsh’s hand, giving him permission to sound hawkish while remaining patient.

(For those looking for added context to this theory, Mervyn King coined it in 2005, comparing monetary policy with Diego Maradona running virtually straight through the England defence because defenders moved in anticipation of where they thought he would go. King’s point was that markets react to what they expect the central bank to do. Those expected future rate changes can influence spending and inflation even when the official policy rate moves relatively little. He described this as the monetary-policy framework “doing the work” through expectations. An interesting economic insight and incredibly well timed, given Wednesday’s game…)

Yet, one benign report cannot settle an inflation debate. Credibility is not earned by a singular win, but by how the Fed responds when the next uncomfortable number arrives. Oil is rising again, underlying measures of sticky inflation remain above target, and the economy is not obviously weak enough to rule out another inflation wave.

Warsh has passed the first test, but more difficult ones are likely still ahead. In the spirit of the ongoing World Cup… it’s Warsh 1 - 0 Inflation as the ref calls for the first hydration break.

The Disinflation Engine

The immediate temptation is to dismiss the report as an energy story… the market bear and the rates hawk might do just so. Motor fuel did much of the work in pulling headline CPI lower, reflecting the retreat in prices following the earlier easing in geopolitical tensions. That component is volatile and may reverse quickly now that oil has moved higher again.

Shelter inflation rose just 0.1% on the month. Core services excluding energy were flat. Price pressures moderated across a broad range of goods and services, with several major categories making a negative contribution. Services inflation posted its smallest contribution since the early months of the pandemic.

The report was unusually soft, which raises the more important question:

Why?

Part of the answer may be that the consumer is increasingly unwilling, or unable, to absorb further price increases. Real wage growth has been weak for several months, the labour market is losing momentum, and businesses are finding it harder to pass costs through without sacrificing volumes. Inflation is cooling partly because demand is becoming more price-sensitive.

The post-pandemic period brought excess savings, strong employment, and rising asset prices… all contributing to why households could look past repeated increases in the cost of living. That cushion is now thin. This is healthy from an inflation perspective, although less bullish for nominal growth. The economy may enter a phase in which slower demand performs some of the work that monetary tightening previously had to do.

Call that the less celebratory reading of Tuesday’s report.

Our broad view remains that inflation is not out of control. Shelter is moderating, goods disinflation has returned, and consumers are becoming more resistant to price increases. The risk of a renewed wage-price spiral has fallen meaningfully.

The path back to target will still be uneven. June benefited from a large energy reversal, while oil has since moved higher on renewed geopolitical tensions. If sustained, that will feed back into petrol, transportation and distribution costs, making the next few prints firmer. Of course, the higher oil rises, the more incentivised DJT will be to diminish tensions in the ME.

A rebound in headline inflation would not necessarily invalidate Tuesday’s message. The key distinction is between an energy-driven bounce and a broader reacceleration across shelter and labour-intensive services.

Our central case remains for headline inflation to rise from June’s unusually soft reading while core inflation trends lower more gradually. That leaves room for recurring inflation scares, but not another inflation crisis. The report changes the timing of the Fed’s next move more than the destination.

What does this mean for our cross-asset views? A softer inflation print changes the near-term policy path, but its implications extend beyond the next Fed meeting. From the shape of the Treasury curve to the outlook for gold and the durability of the equity rally, the more important question is where the market has already moved too far, and where the best asymmetries now sit.