Money Markets - April 2025

Equities, expectations and Eurozone initiatives.

"A fool thinks himself to be wise, but a wise man knows himself to be a fool." - Shakespeare

Welcome to AlphaPicks’ monthly market update, a rundown of global markets for the coming weeks in under ten minutes (we didn’t overrun the target this month).

Here’s what you need to know…

If you are not yet a premium subscriber to AlphaPicks, you can manage your account here.

Macro

Global markets have eased somewhat over the past two weeks after experiencing a stretch of volatility driven by political upheaval. The macroeconomic indicators still look strong, and the Federal Reserve is on track to cut interest rates later this year, while fiscal policies in Europe and China are becoming increasingly supportive.

In Germany, the passage of a significant stimulus package through parliament has marked a clear policy shift, setting the stage for economic recovery. However, in the United States, troubling signs are starting to show as consumers brace for rising unemployment and inflation, and political uncertainty is causing businesses to hesitate on investment decisions.

A key date for the markets is April 2, referred to as “Liberation Day” by Trump, when substantial tariff plans are anticipated to be unveiled. Our baseline scenario suggests that tariff uncertainties will peak in early April, after which Trump is expected to pivot towards measures that support growth.

The Fed in March held policy rates unchanged at 4.25-4.50%, as expected, and continued to signal two rate cuts in each of 2025 and 2026 (median estimate). The message from Chair Powell was that tariff inflation is seen as transitory, meaning the Fed can look through a temporary increase in prices and has scope to react to unexpected weakness. We expect the Fed to remain in a reactive stance that will be echoed by Fed speak in the coming weeks.

Recent comments indicate that many members of the Governing Council see the potential for lower policy rates, but they remain unsure whether to cut rates or hold off in April. Key factors influencing the April decision include March inflation figures (released on April 1)—particularly in the services sector—and the impact of Trump tariffs (announced on April 2).

The EU’s defence initiative, “Readiness 2030” (previously known as “ReArm Europe”), appears to be falling short of the Commission’s goal of EUR 800 billion. Signals from several countries, including France, suggest a reluctance to pursue additional national borrowing due to high debt levels and concerns about negative reactions in the bond market. We believe that collaboration on EU defence borrowing, going beyond the EUR 150 billion currently outlined in the plan, may be essential in the future.

Swap spreads have continued to rebound from the cheapening caused by the German fiscal package in early March. Looking ahead, Germany’s increasingly expansionary fiscal policy is expected to remain a structural driver of bond cheapening relative to EUR IRS in the coming quarters.

The recent rise in credit spreads may look alarming at first glance, but the broader context tells a different story. Despite the uptick, spreads remain well below levels that historically signalled significant market stress. The current Z-score of 3.3 indicates an elevated but not extreme deviation, and spreads have yet to approach the peaks seen during past periods of genuine concern. This suggests that the move is more reflective of short-term positioning or mild risk repricing rather than a fundamental deterioration in credit conditions.

Equities

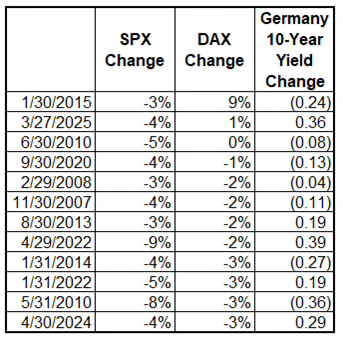

Equity fact to start off: It’s incredibly rare for the S&P 500 to decline in a month while the DAX moves higher. This has happened only three times since 2000.

U.S. Equities: Neutral Stance Amid Transition

The U.S. equity market outlook for Q2 is neutral, reflecting a transition from the Trump sentiment trade to the Trump tariff trade. Falling growth expectations and technical indicators, such as the breakdown in market leadership, suggest a cautious approach.

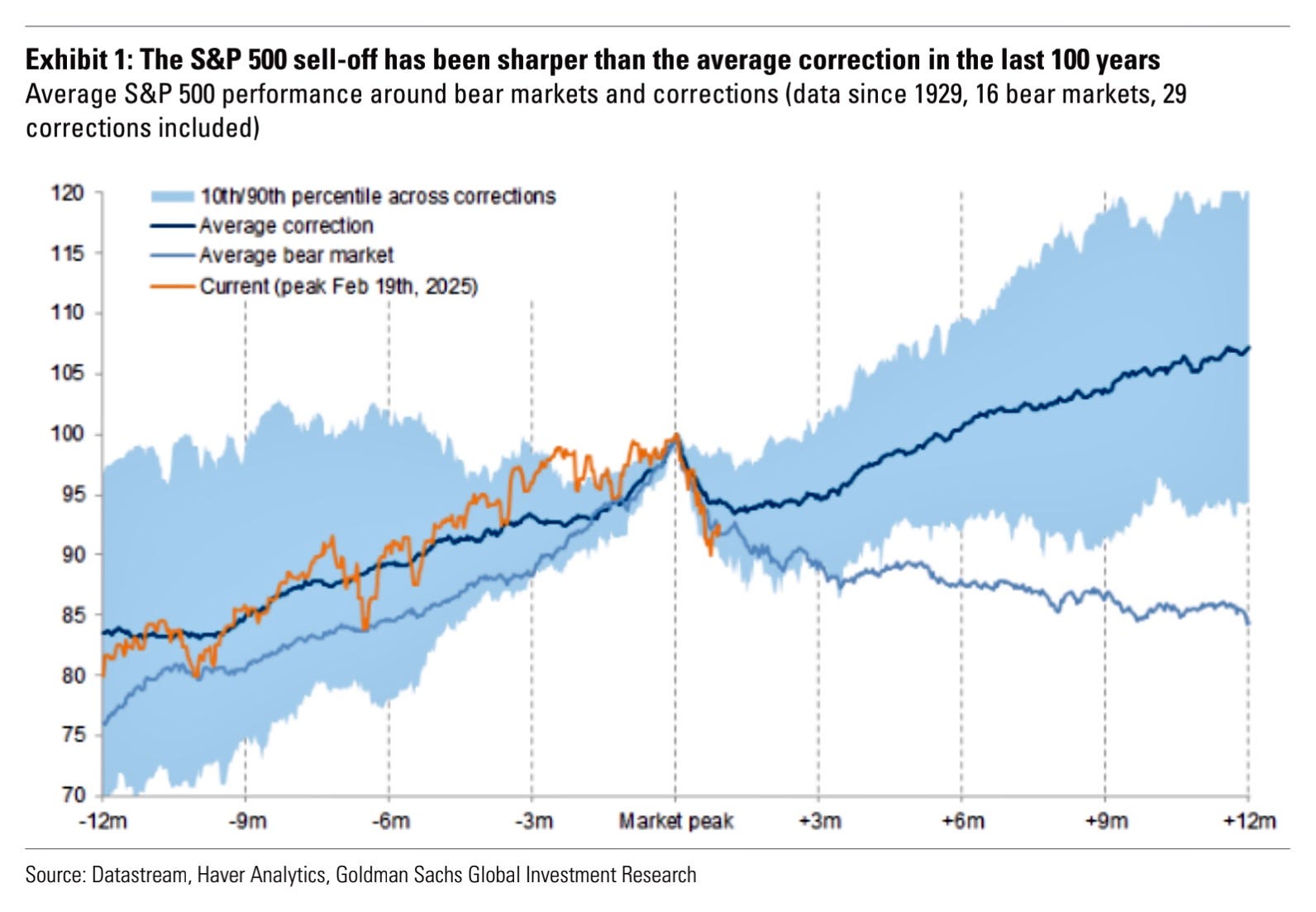

The S&P 500 correction we experienced through March 10th was one of the fastest corrections on record. Equity risks from here are cut both ways. While some tariff impact is priced, markets may underestimate the full outcome if US corporates feel the heat. That said, a more benign scenario (phased, less aggressive tariffs) could offer a better buying opportunity after the dust settles than getting very long into the tariff decisions.

China: Optimism Despite Tariff Risks

In contrast, the outlook for Chinese equities remains positive. U.S. exceptionalism appears to be on hold, and technological advancements in AI and large language models bolster China’s growth narrative. Despite mixed economic data earlier in the year, the bottoming out of the credit impulse and resilient A-share performance indicate underlying strength. However, the risk of further tariffs or non-tariff constraints remains a wildcard. An agreement between Trump and Xi could catalyse further outperformance.

Japan: Underweight Due to External Risks

The Japanese equity market faces multiple headwinds, including the potential for tariffs, a global growth slowdown, and yen appreciation from a more aggressive Bank of Japan stance. Year-to-date, Japan has shown resilience against U.S. market sell-offs, but the outlook remains tepid. The auto sector, crucial for Japan's economy, is particularly vulnerable to global tariffs. While strong corporate earnings and share buybacks highlight corporate health, upside potential remains limited in the short term.

European Equities: Momentum with Caution

European markets have been among the best performers year-to-date, buoyed by improved fiscal policies in Germany, defence spending, and shifting capital flows amid concerns over the U.S. economic outlook. However, the economic data remains mixed, with hard data lagging behind soft data improvements. The key factors influencing Europe’s future performance include the allocation of the EU defence budget and the unification of industrial strategy. With the tariff announcement looming, a neutral stance is prudent until clearer signals emerge post-event.

Tactical Over Reactive

The upcoming tariff decisions on April 2nd will test market resilience and policy expectations. Maintaining a neutral stance in U.S. equities allows for flexibility in responding to market developments. Meanwhile, optimism in China and cautious positioning in Europe reflect a nuanced approach to regional market dynamics. Investors should prepare for volatility but remain poised to capitalise on opportunities once the post-announcement landscape becomes clearer.

We posted a deep dive into equity thoughts in the week, which can be found below.

FX

The bulk of the price action on the US dollar came in the first few trading days of the month, as the chart below highlights. The move lower was correlated to the general risk-off sentiment that spread through the market. Some might wonder why this negatively impacted the greenback, given the fact that it’s traditionally perceived as a safe haven during unpredictable times.

There are two main reasons why this was not the case this time around…