Money Markets - November 2024

Elections, easing and end-of-year run-up.

“The difference between insanity and genius is measured only by success and failure”

- Masashi Kishimoto

Welcome to AlphaPicks’ monthly market update - a rundown of global markets for the coming weeks in under ten minutes (sort of).

This month, our guest contributor is Ebrahim Rahbari (@ebconomist), an independent strategist and economist. Previously, he was the Chief FX Strategist and Global Head of FX Analysis at Citi.

Macro

by Ebrahim Rahbari

There are macro issues galore into year-end. I want to focus on i) the trends in October, ii) how to trade the US election and iii) market drivers into year-end.

US vs The Rest

Three major developments drove asset prices in October: 1) US economic resilience, 2) US outperformance vs RoW and 3) markets pricing higher odds of a Trump election victory. But performance, notably the US Dollar rally and the sell-off in fixed income and related assets, such as JPY, needs to be seen against its starting point: up to mid-September, markets priced a sharp Fed rate cutting cycle amid recession concerns and a proactively dovish Fed, while investors were heavily positioned in JPY and short USD.

How to Trade The US Election

My long-held view has been that this is the Republican party’s election to lose, informed by the broader context illustrated in the Gallup survey, early voting trends, and swing state polling. I discussed many election-related questions here and here.

But at this point, I think Trump trades no longer offer attractive risk-reward into the election, which is different from markets fully pricing a Trump victory/ Republican sweep. That is because i) markets have increasingly priced a Trump victory and ii) there is a plausible path to a Harris victory in Pennsylvania via ‘Never Trumpers’, the ‘Puerto Rico effect’ and broader Democrat turnout efforts, which could also imply (slight) delays in election clarity.

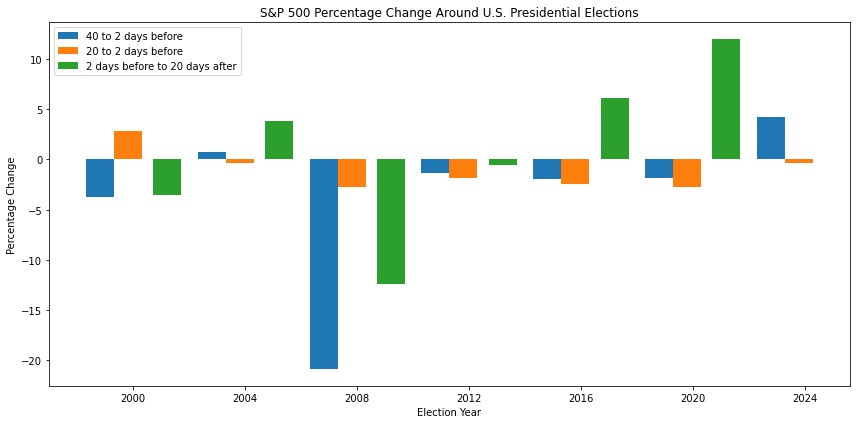

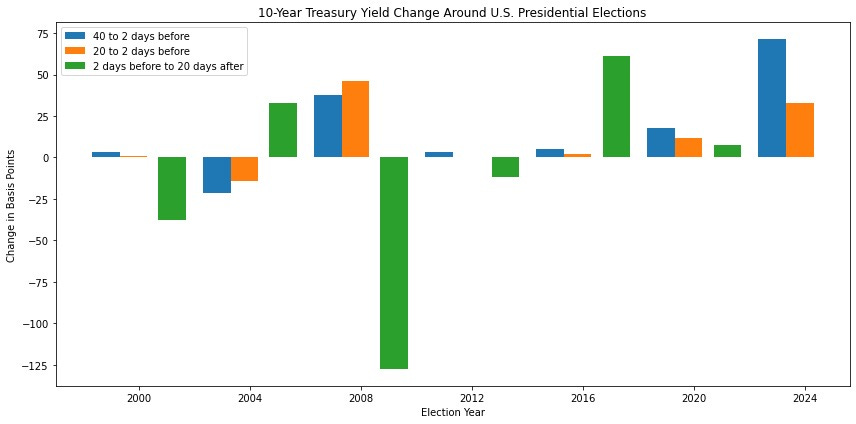

For now, my approach to trading the election focuses on owning the ‘election risk premium’, which historically paid off on average. Typically, US elections would see a risk premium in risk assets, with US equities typically slightly down 1-2 months into the election and strongly up afterwards. Given the focus on fiscal risks, the risk premium this time around is in rates (& -sensitive assets) and tariff-sensitive FX.

Thematically, owning the risk premium for this election, therefore, aligns more with ‘Harris trades’, which makes sense because investors appear to have mainly hedged against ‘Trump outcomes.’ My preferred way to express this view is to sell out-of-the-money (OTM) optionality to higher US yields around the wider election window, given high US rates and high rates volatility.

But it makes sense to keep some powder dry, given that the election outcome will have directional impact on many assets, and historically, it’s often been possible to trade the election result afterwards. There are many scenarios to consider, but two examples include buying US equities in a Trump victory with orderly rates (e.g. via divided government) or patiently buying a dip on a Harris win.

What’s Next?

Beyond the election outcome, macro markets will trade i) US macro, ii) momentum and iii) year-ahead positioning into year-end, alongside many idiosyncratic themes. The key remains the US rates trajectory. I lean towards at least a speed bump in 10-year yields between the current 4.38% and 4.50%, in line with the above views and the latest payroll report lowering the bar again for a December Fed cut. But it’s not clear if it’d be more than a brief relapse given benign US macro trends that could shorten the Fed easing cycle.

Last week’s data took excitement out for the ECB & Fed and paves the way for likely 25bp cuts for each in December. That was made up in excitement in the UK – I see the risk-reward of a combined 31bp of cuts priced for Nov & Dec as attractive to receive, despite the volatility around last week’s Budget.

Currently, I expect investors to start positioning in November for 2025 with a positive mindset, including looking for cheap upside in risk assets – including upside for EM equities, particularly under a Harris victory. Yen upside also appeals even though the timing of entry and cross-currency depend on the election outcome.

If you want to become a premium subscriber and access every article, you can manage your account here.

Equities

By AlphaPicks

For the first part of November, U.S. equity markets will be noisy. However, come November 11th, the U.S. will have a new President and the Federal Reserve will have (most likely) reduced their rates by 25bps and given some comments on their thoughts (note that they are currently in a blackout period).