Money Markets - October 2024

Fed easing, China bazooka, Trump/Harris up ahead.

“Attention is the rarest and purest form of generosity.”

Simone Weil

Welcome to AlphaPicks’ monthly market update - a rundown of global markets for the coming weeks in under ten minutes…

This month, our guest contributor is:

Alyosha, an independent commodity trader and member of COMEX/NYMEX for over four decades. He writes at market vibes.

Macro

September had a disproportionate amount of weight placed on the US Fed meeting, with the announcement and press conference on Wed 18th showing that the committee decided to start monetary policy easing with a jumbo 50bps cut.

Even though some thought that the decision for 50bps over 25bps could spark some concern amongst investors and cause a sharp reaction in both equities and fixed income, it was actually taken as a positive. The cut was seen to be a stimulant for demand which could help to engineer a soft landing.

Indeed, investors appeared to be reassured by Powell’s comments:

“I don’t see anything in the economy right now that suggests that the likelihood of a recession, sorry, of a downturn, is elevated. You see growth at a solid rate. You see inflation coming down. You see a labor market that’s still at very solid levels. So, I don’t really see that now.”

Once the meeting had been digested overnight on Wednesday, Asian markets kicked off a broad based equity market rally which continued for the rest of the month. US Treasury yields fell as many eyed up further imminent cuts that tie in with the updated Fed dot plots.

The other key stimulant to risk appetite was stimulus from China to end the month. A broad based package including rate cuts and other measures helped to push the Hang Seng index to the best weekly gain since 1998. The CSI 300 closed the last week of the month up over 15%, the best gain since 2008.

Despite this rosy macro backdrop to finish September, there’s still plenty of caution to note for October.

As our friend JJ flags up in his Commod section below, oil is in a real pickle and being influenced by a variety of factors (none of them bullish for the near term outlook).

Staying in commodities, precious metal prices continue to surge, with silver now outperforming gold in percentage gain terms YTD. Part of the rally can be attributed to the lower opportunity cost with US rate cuts. However it’s rational to think that some of the gains is down to investors diversifying exposure and even actively looking to allocate to these safe havens ahead of Q4 event risks.

The Fed don’t meet in October, but the host of key data releases during the month mean that implied pricing for the November meeting will help to dictate flow.

A big question for investors to consider for October is that if 50bps does get priced in for November (given that the dot plots only shows a cumulative 50bps for the rest of the year), would that act to spook the market? There surely comes a point whereby people would start to get a little uncomfortable with what the pace of easing would assume about the health of the economy.

As for other macro points to watch out for in the month ahead, we flag up the slightly surprising victory at the end of September for the new Japanese PM, Shigeru Ishiba. Known as not being a fan of Abeonomics, or a devalued Yen, as well as being a China hawk and wanting the BoJ to normalise monetary policy, there could be a lot of fireworks to watch out here for USDJPY, Nikkei 225 and other related assets in coming weeks.

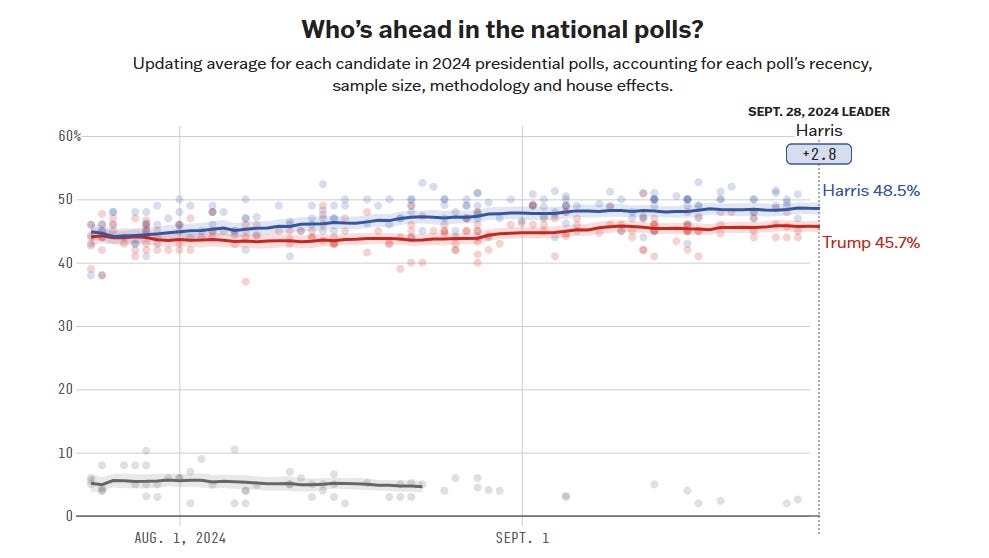

Finally, even though the US Presidential election just falls into November, positioning will definitely be taken up over the course of October. We flag up some of the implications for this in FX and equities, but needless to say that it’s worth staying reactive to polls, interviews and policy chatter in coming weeks to see if the winning chances for either party start to meaningfully diverge.

Commodities

By JJ (Alyosha)

The most important thing happening in commodities today is happening in oil. OPEC is coming undone because diverse sources of energy are converging in usage and price everywhere. Coal, wind, solar, LNG, natural gas, Hydro, and nukes compete with refined oil products.

The marketplace is weeding out the weak, not so much by sector per se, but by the weakest player within each. In oil, that means lower prices challenging producers with high break-even costs. In OPEC, that means undercutting for market share.

Refining margins have been low and falling for over a year because crude prices are too high due to OPEC policy. Demand for refined products has been flat, and product prices have declined. The chart below is the notional NYMEX spot heating oil crack spread indicating the relative value of distillate to a barrel of crude. Crude has no value unless it is refined. Wholesale gasoline prices traded $1.90 last week, 30% lower than their highs in 2005.

War, politics, and climate dogma have never been aligned because oil was subject to abusive pricing and economically prohibitive development. Technology has finally changed the risk profile of E&P. In the tight oil regions, new wells can be found, funded and brought to market in months instead of years.

One must ask, are strategic reserves even necessary? Wars in the Middle East do more harm to the cartel than they do to consumer nations. When Gaza broke out, oil went down. The game in crude oil now is reliable service at competitive prices in the same way consumers choose a local gas station, price and service.

As for coal, If China and India keep building coal-fired utilities, coal will be available.

Wind seems to be the weakest long-term solution. Solar has wood to chop but the highest potential for innovation. Hydro is free power but limited. Nukes have come a long way, Baby (golf clap Mr. Gates). America is the largest producer of crude oil in the world. I don’t see that changing for a very long time.

To join AlphaPicks as a premium reader, you can manage your subscription here.

Equities

We leave September with a risk-on equity front. The Fed is easing monetary policy, aligning with similar actions of the ECB and BoE, and China is going full ‘bazooka’ and stimulating multiple areas of their economy. The spillover from these tailwinds has equities rallying.