Markets are settling into an uncomfortable rhythm. Early-week optimism, hopes of de-escalation, and then giving way to late-week liquidation as the reality of a prolonged conflict in Iran feeds through to inflation, policy expectations, and positioning. Last week followed that script closely.

The S&P 500 opened with a bid, supported by tentative signs that traffic through the Strait of Hormuz could resume in some form. Crude drifted lower, with WTI briefly falling toward $94, and equities responded accordingly as dip buyers stepped back in. For a moment, the market was willing to treat the conflict as containable.

The optimism proved fragile by the midweek, with the narrative shifting decisively as attacks on energy infrastructure escalated. Iran confirmed damage to the South Pars gas field, while Qatar reported extensive disruption at a major LNG facility. Oil prices reversed sharply higher and, more importantly, the market was forced to reassess the persistence of the supply shock. At the same time, the policy backdrop turned more restrictive. Federal Reserve Chair Jerome Powell acknowledged that rate hikes had been discussed as a potential next step, with the ECB and BoE reinforcing that shift a day later. Rate-cut expectations are out of the picture, and equity outflows accelerated into the back half of the week.

By Friday, the S&P 500 had fallen to a six-month low, the Russell 2000 entered correction territory, and megacap tech traded meaningfully below recent highs. The idea that there was a “safe corner” of the equity market continued to break down, with correlations rising and diversification offering little protection.

Sector performance reflected the macro shift. Energy outperformed again as crude prices moved higher, while financials were the only other group to finish in positive territory, helped by the Fed’s proposal to ease capital requirements for large banks. In contrast, materials and consumer staples lagged as rising input costs and inflation expectations weighed on margins. The weakness in materials has been particularly notable, with the sector reversing sharply from one of the year’s strongest performers to one of the worst since the conflict began.

The broader message from positioning is changing. A market willing to fade geopolitical risk has now transitioned into one that is questioning the duration and economic impact of the shock. Sell-side desks are increasingly flagging complacency, with the risk that investors have underestimated how persistent elevated energy prices can be for both growth and inflation.

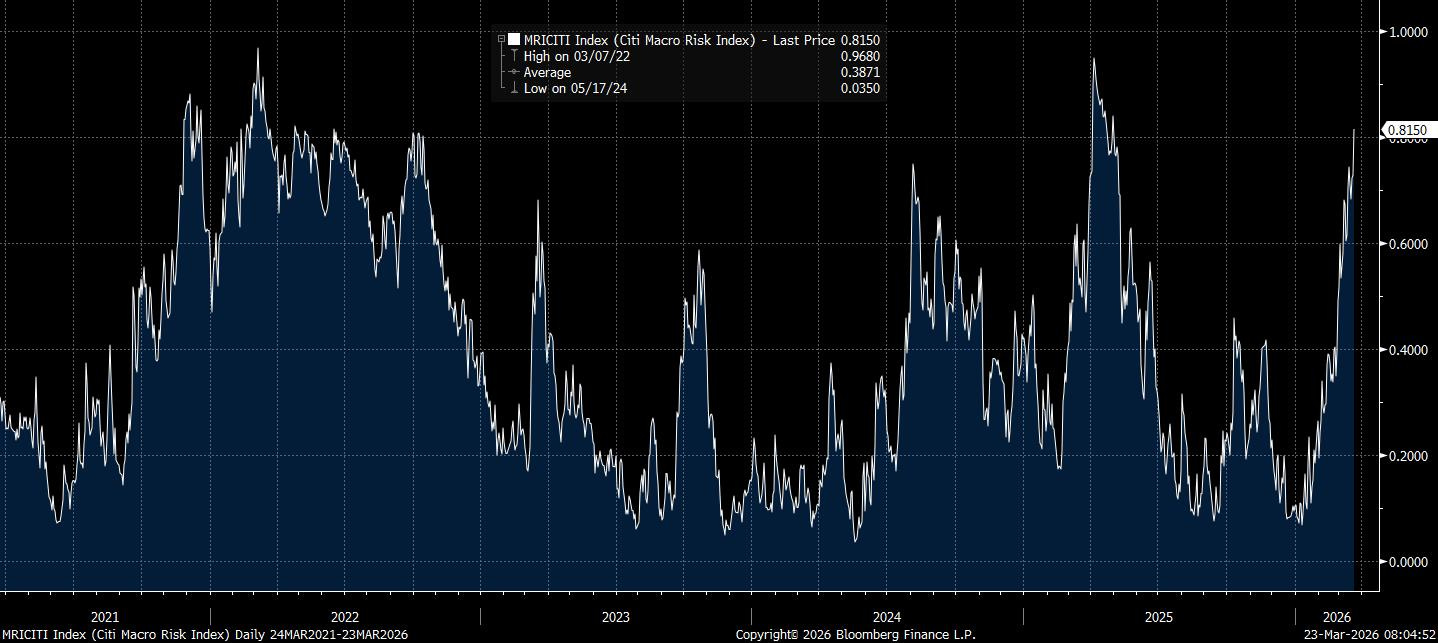

Citi’s Macro Risk Index consists of asset prices sensitive to risk (which includes credit spreads, Treasury bill-OIS spreads, basis swaps, asset swaps, VIX, etc.), and has been rising sharply, although it remains below its April 2025 high.

Policy is reinforcing that move. The Fed held rates unchanged, but the signal from the meeting was clearly hawkish. The bar for cuts has risen materially, with policymakers emphasising inflation risks and even entertaining the possibility of further tightening. Markets responded by aggressively repricing the front end, with Fed funds futures briefly pricing tightening scenarios and OIS stripping out much of the easing expected just weeks ago.

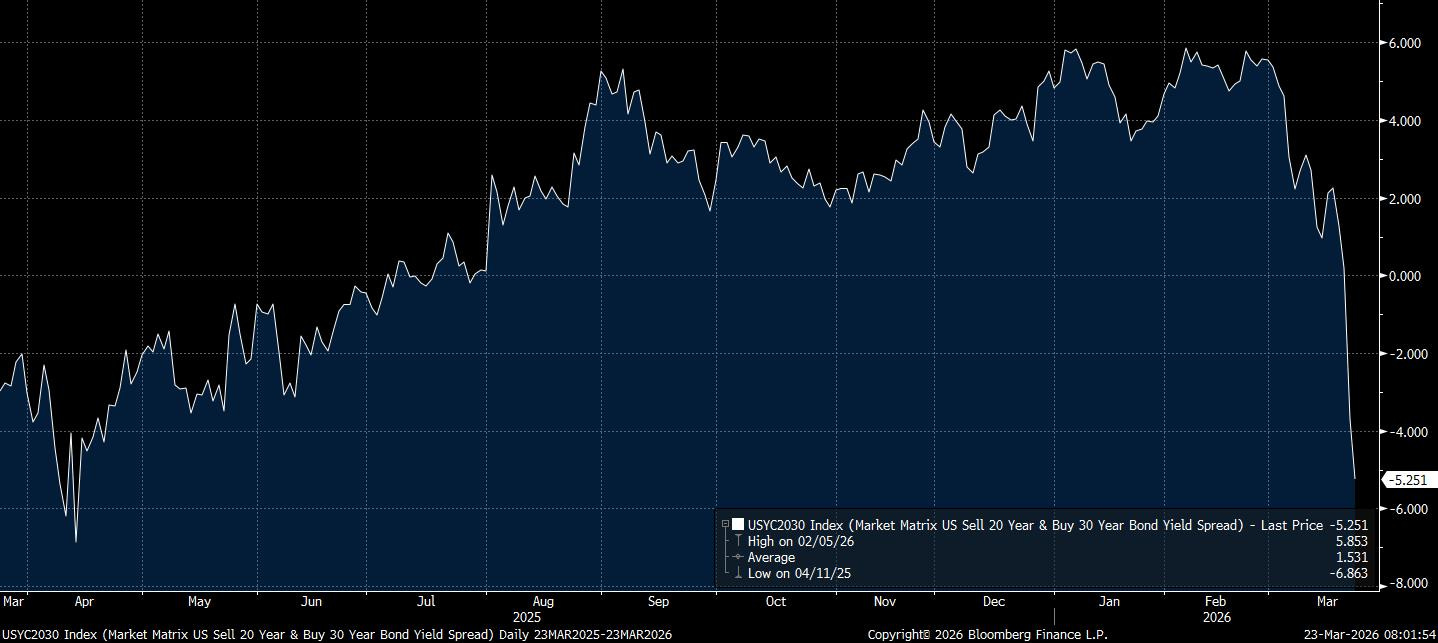

Across assets, the adjustment has been consistent. The US dollar ended the week softer but remains structurally supported, particularly as global central banks move in a similarly hawkish direction. In rates, the curve flattening intensified, with evidence of position unwinds and a broader recalibration of rate expectations. The inversion in longer-dated segments such as 20s30s highlights how much of the adjustment is now being driven by inflation risk rather than growth optimism.

Energy prices, policy constraints, and geopolitical uncertainty are feeding into each other, leaving equities in a position where rallies struggle to hold and downside moves build gradually. Until there is clarity on either the trajectory of the conflict or the path of inflation, the pattern of early optimism and late-week selling looks less like noise and more like the defining feature of this phase.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading. Following last week, the focus remains very much in the rates and FX space.

“Gilts Get Renewed Headaches”

“Sell the Liquid Winner”

“The Underlying Dynamics Pushing USD/JPY Higher”

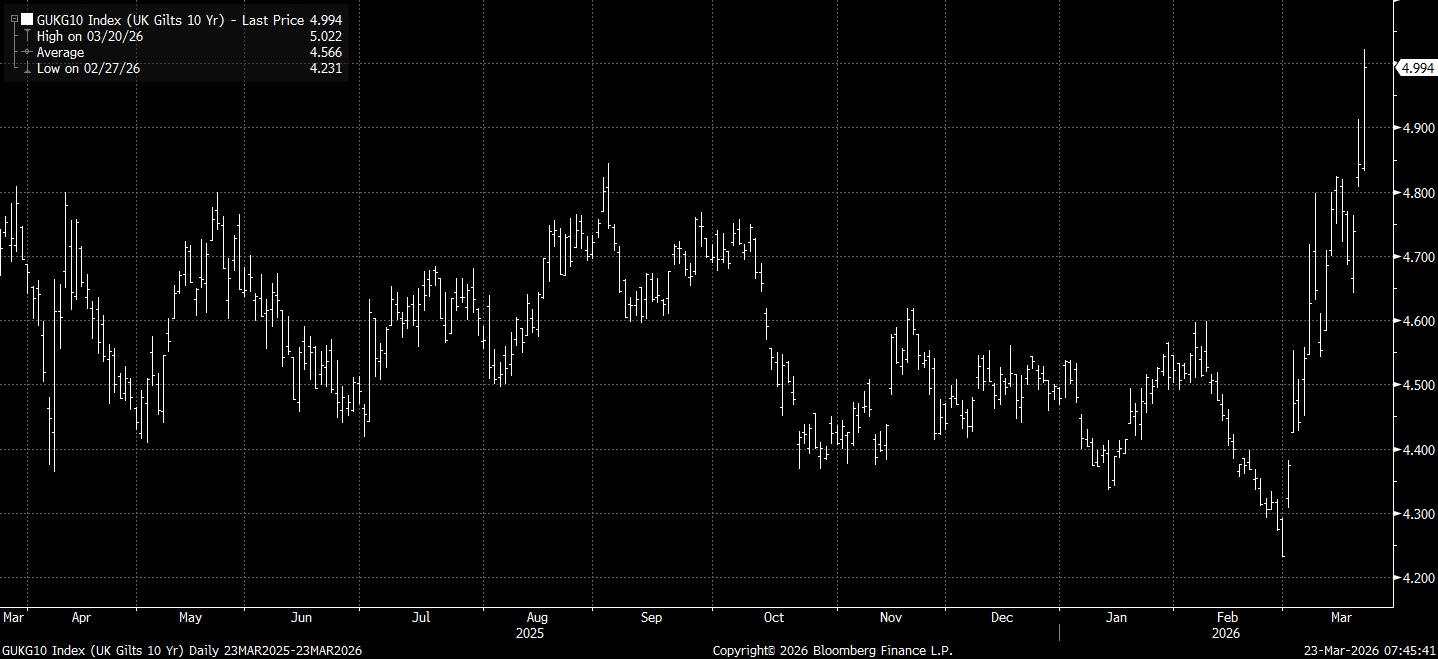

Gilts Get Renewed Headaches

UK Gilts experienced a sharp and disorderly repricing over the past week, with the 10-year surging through the 5% threshold for the first time since the global financial crisis, marking a decisive break from the disinflationary backdrop that had dominated pricing earlier in the year.

The adjustment has been particularly acute at the front end, where two-year yields have repriced aggressively higher as markets rapidly abandon expectations for rate cuts and instead begin to discount a renewed tightening cycle from the Bank of England. It has been nothing short of a very eye-opening move whereby the gilt market has transitioned in a matter of days from a “late-cycle easing” framework to one centred on renewed inflation risk. UK 1-year inflation swaps have moved sharply higher, rising by approximately 50bps to trade above 4%, while 5-year breakevens have also drifted upward.

The core of the move has been the sharp escalation in global energy prices following the Middle East conflict, which has reintroduced a classic cost-push inflation shock into an economy already exhibiting fragile growth dynamics. As we’ve noted since the conflict began, along with the EU, the UK does have a structural sensitivity to imported energy, which therefore feeds directly into inflation expectations. Yet the move in Gilts has been compounded by the BoE’s own communication, which, while holding rates steady, explicitly acknowledged upside risks to inflation and signalled that further tightening may be required if second-round effects materialise.

Having to wheel out Governor Bailey for media appearances on Thursday afternoon after the meeting goes some way to show how keen they were to try and calm the markets down (which didn’t do much good).