Nobody Likes Negative Rates

But that might be the direction for the Swiss National Bank.

With several central bank meetings on the cards this week, there was a higher chance that an unexpected move would occur, leading to outsized moves in FX and rates markets.

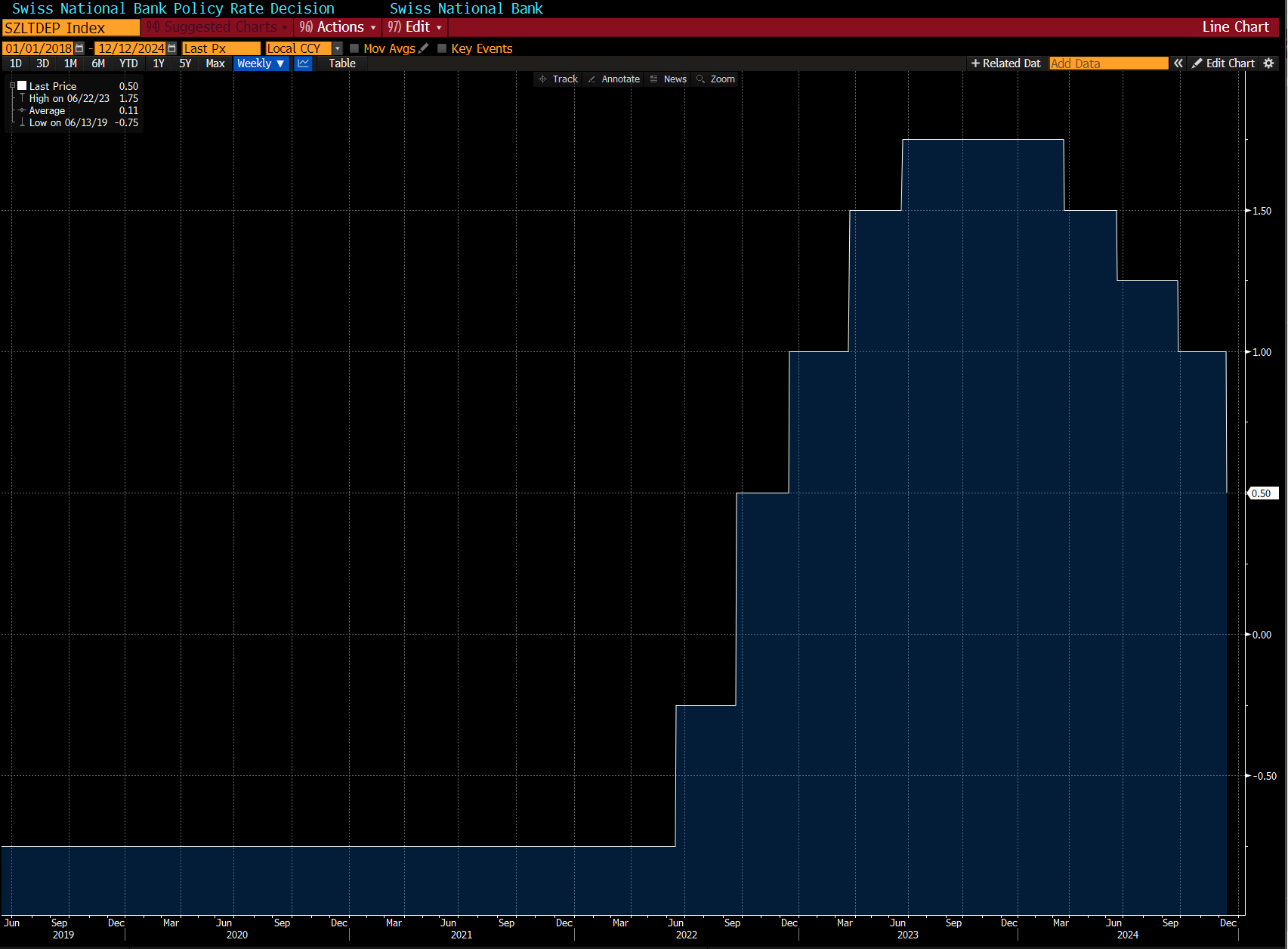

With the BoC, RBA and ECB all following through with their expected cuts, the SNB was left on its own, cutting rates by 50bps when markets expected a quarter-point reduction.

The large movement on Thursday positions the SNB merely half a point—or two quarter-point reductions—away from a zero interest rate. Should the upward pressure on the Swiss franc continue and policymakers decide to pursue further cuts, they will soon face a critical choice:

Reconsider the negative interest rate policy previously implemented, with the associated risks to the financial system or

Expand their balance sheet through market interventions.

Switzerland implemented a subzero interest rate policy for nearly eight years to deter currency speculators. The nation maintained the lowest interest rate in the world at -0.75% and was the last economy in Europe to transition out of subzero conditions, moving higher in September 2022.

“One very important lesson is that negative interest rates worked,” Schlegel, President of the SNB, said. Their plan to introduce negative interest rates in 2015 was to lower the attractiveness of the Swiss franc, and it did work.

Schlegel refrained from commenting on the forthcoming actions of the SNB, but he indicated that policymakers could be flexible to convene outside their standard quarterly meeting schedule if necessary. “To wait on cuts doesn’t make any sense,” he added.

Market pressures over the past year have intensified, driven by investors’ perceptions of Switzerland as a haven during periods of political uncertainty, of which there have been many. Even aggressive rate cuts and lower yielding rates haven’t slowed the Swiss franc’s climb. Last month, the currency reached its highest value against the euro in nearly a decade. In September, it approached its strongest level against the dollar within that timeframe. However, recent dollar strength has since weakened the franc in this pair.

The gains in the franc have become a burden for the export-oriented Swiss economy that risks driving inflation below the central bank’s 0-2% target range.

The central bank’s inflation projections were revised down substantially, as price gains kept surprising to the downside in the last few months. The SNB forecast inflation will average 0.7% in 4Q24, down from 1% in its September projections. They now expect inflation to average 0.3% in 2025, compared with the 0.6% expected at the September meeting. Finally, there is an expectation that inflation will reach 0.2% in the second quarter of 2025.

It doesn’t look likely that the current depreciation of the Swiss franc will last. The scope for further cuts is now even more limited, and there isn’t a case for a stronger euro in the medium term. We saw from the ECB meeting that, although the December decision was only a quarter point, some committee members still feel a half-point cut is necessary next year to support the bloc. More on this later.

So, does the SNB consider option one: sub-zero rates?

Negative Rates

Nobody likes negative rates, but Schlegel said in Thursday’s meeting that “they do work.” Given that it took a pandemic to generate inflation and lift the likes of Switzerland, the Eurozone, and Japan out of negative rates, one might argue with the assessment that they do actually work as intended. Anyway, maybe the days of negative rates are not over. Suddenly, they are becoming a little bit more realistic. (Maybe an out-of-consensus view for the macro scene in 2025?)