The market still managed to rise, but the character of the rally is far different.

US equities were on course for a clean holiday-week advance before technology stocks once again complicated the picture. A softer payrolls report, less hawkish language from Kevin Warsh, and further signs of resilience outside the AI complex all supported risk appetite, but the late-week semiconductor selloff kept a lid on the broader move. The S&P 500 finished higher, the Dow outperformed and the Nasdaq lagged, which tells the story clearly enough.

After using his first FOMC meeting to signal a much tougher inflation stance, Warsh sounded less aggressive, noting that inflation expectations and price risks had eased slightly in recent weeks… enough to push back against the idea of an imminent hike, which gave equities room to breathe.

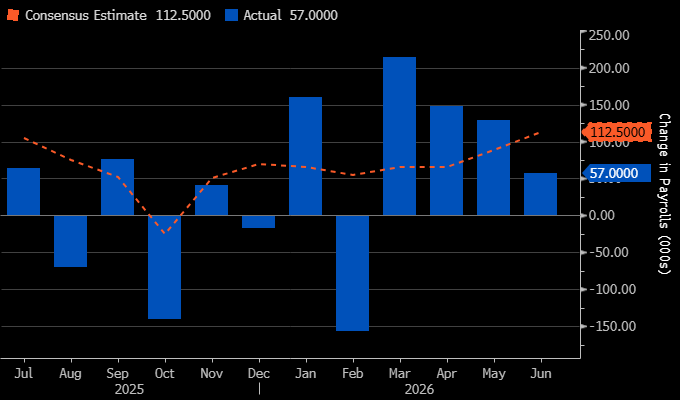

Payrolls then added to the same message. June nonfarm payrolls came in well below expectations, with a negative two-month revision and a drop in participation. The expected summer hiring boost failed to appear, particularly in leisure and hospitality, which made the report feel softer beneath the surface as well as at the headline level. Equity futures initially rallied as markets pushed hike pricing from October to December. After several weeks of the Fed becoming an active constraint on risk assets, this was the first clean data point that gave investors permission to question the urgency of tightening.

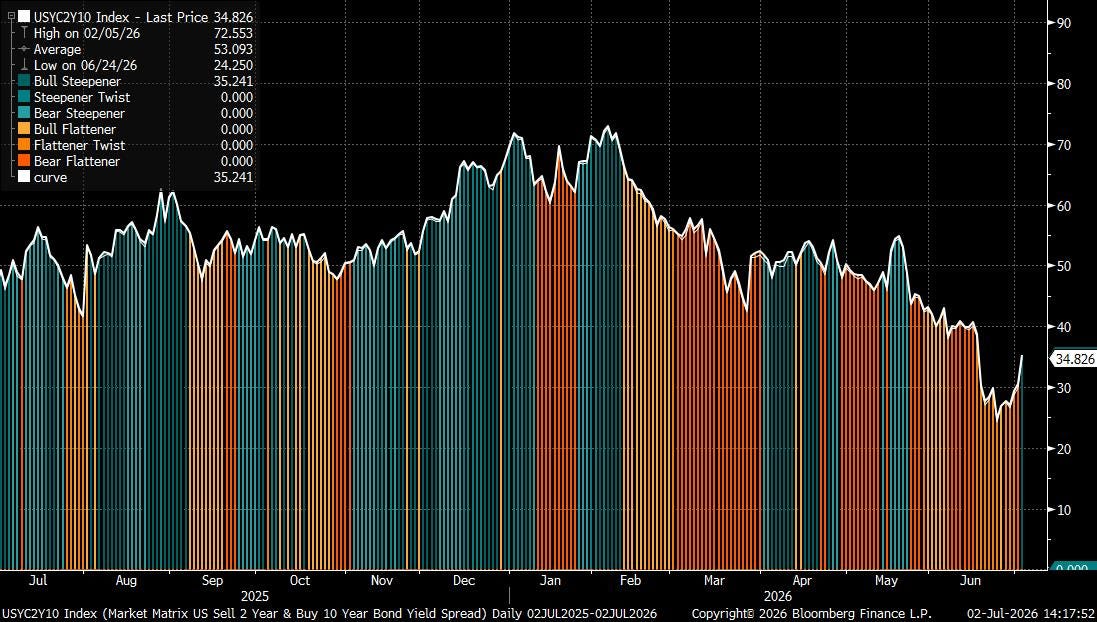

Across rates, the curve steepened as the market reacted to Warsh’s softer tone and the weak payrolls print. The move in the dollar was equally straightforward, with the greenback slipping as traders faded the more aggressive Fed path. USD/JPY briefly moved back below 161, offering some relief to Japanese officials, though the pair remains close enough to intervention-sensitive levels to keep the Ministry of Finance in focus, particularly in thinner holiday liquidity.

The market has not lost its appetite for risk, but is becoming more selective. A softer Fed path, lower oil, and resilient non-tech sectors are enough to keep the index supported. But the AI trade is now more volatile, more crowded, and more exposed to changes in market structure than it was earlier in the year.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“US Labour Market and Rates Impact”

“Small Themes, Defence Shines”

“Software Strength, the Pain Trade”

US Labour Market and Rates Impact

The dominant macro event of the week was Thursday’s June payrolls print. The number came in at just 57,000, barely half the consensus expectation and a sharp loss of momentum from the spring run-rate (three consecutive beats). On the surface, the unemployment rate falling to 4.2% should have been hawkish. In normal times, a lower unemployment rate is not exactly an invitation for the Fed to relax.

But this wasn’t the market’s read. The unemployment rate fell because the labour force shrank. Participation dropped sharply, removing workers from the denominator and inflating the headline unemployment rate.

Treasuries rallied, the dollar sold off, and the market quickly stripped out the near-term Fed hike risk that had been building since the stronger May print. The 2-year yield fell around 5–6bps toward 4.11–4.13%, while the 10-year was little changed around 4.46–4.48%, leaving the curve with a cleaner path to re-steepen.