Powell's Last Rodeo

Jackson Hole preview.

This year’s Jackson Hole Symposium (Aug 21–23) lands at a rare crossroads: it’s Fed Chair Jay Powell’s likely final appearance and the main policy stage before the September FOMC meeting. The theme is “Labor Markets in Transition: Demographics, Productivity, and Macroeconomic Policy”, and comes amid a turbulent period for Powell, where he’s needed to thread a tight needle between easing expectations and economic caution.

Sticky inflation (Core PCE at 2.8%) and persistently hot wage gains (4.8% YoY) provide the foundations for Powell to push back on recent dovish rate repricing. Yet at the same time, negative revisions for payroll growth and weaker job numbers have provided evidence of a fragile labour market, one that needs easing monetary policy.

The stance Powell chooses to take will reveal his hand ahead of the key September FOMC meeting and, in some ways, determine how his legacy from his time at the Fed will be remembered.

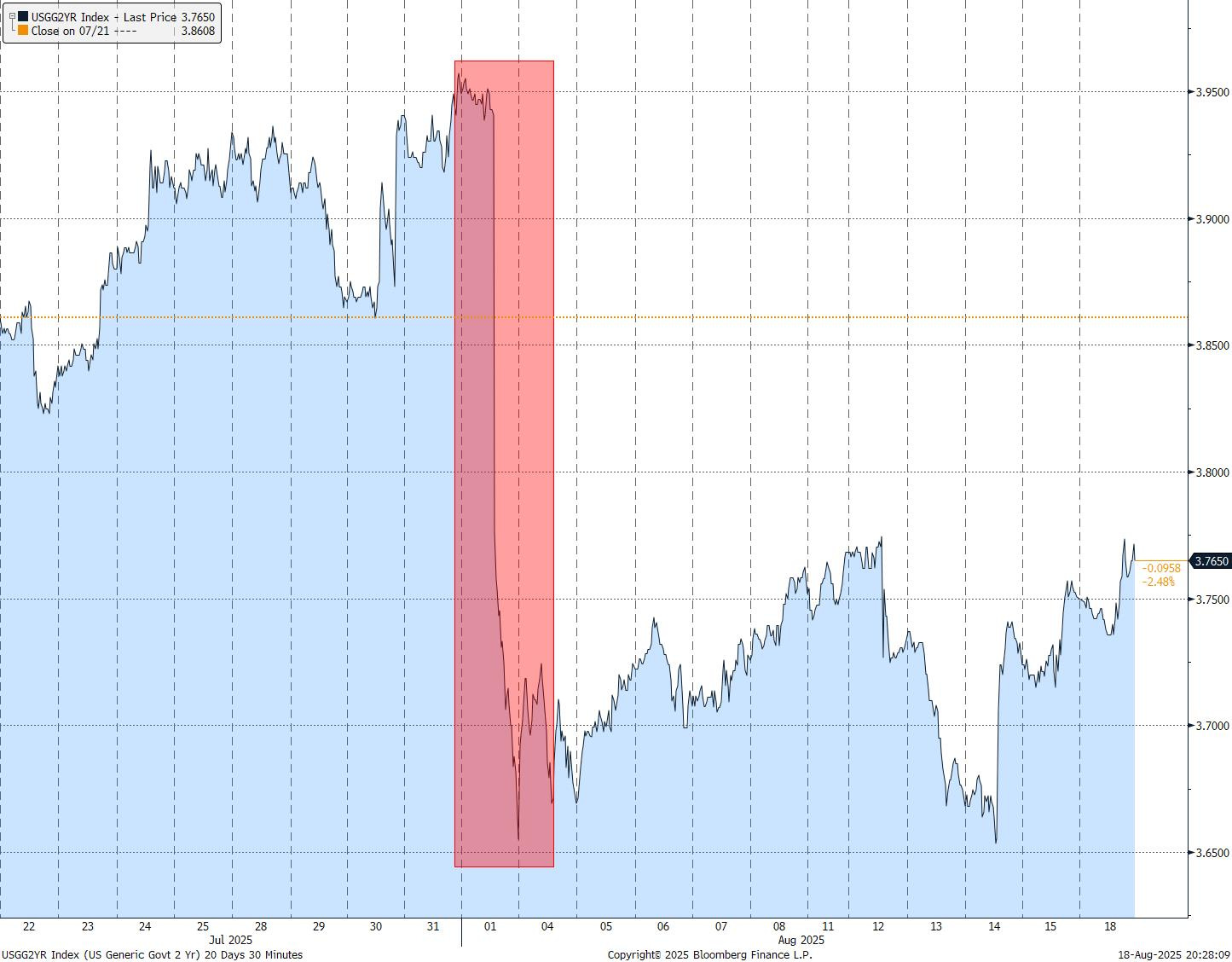

Bond Markets Frontrunning

Bond markets rarely wait for Powell to speak before making their move, and this week has been no exception. Traders have leaned aggressively into rate cut bets ahead of Friday, with fed funds futures now discounting a faster and deeper easing cycle than the Fed itself has guided.

The bulk of the pivot came from the weak payroll figures and revisions at the start of the month, where the sensitive 2-year yield shifted aggressively lower.

The curve has shifted in anticipation of a dovish tilt, as if Powell will validate the recent loosening in financial conditions. It’s a familiar reflex: positioning ahead of the chair’s words, hoping to catch the turn before it’s officially blessed.