Power In Play

Betting on the break in the grid.

The political pivot has already begun. Energy policy in the US is shifting from subsidising the transition to monetising the bottlenecks.

The tax credits that once underwrote a decade of solar and wind expansion are being phased out. Tariffs are rising. Permitting reform is being redirected, not to accelerate clean buildouts, but to clear the path for nuclear and gas. With energy-intensive AI demand outpacing infrastructure, the policy emphasis is shifting from decarbonisation to dispatchability.

This is no longer about climate, but about capacity.

Across global markets, the net-zero narrative is fraying. Europe is quietly extending coal lifelines. China is building new fossil generation at breakneck speed. In the US, regulators are being asked to approve rate hikes for technologies that voters increasingly can’t afford and politicians no longer wish to subsidise.

Markets are adjusting fast. Independent power producers (IPPs) with nuclear and fossil portfolios, once the legacy sides of the grid, are now the policy favourites. Regulated utilities with large renewables books are being left to defend eroding margins, with PUCs increasingly hesitant to authorise rate increases. The divergence between these two business models (between spot price leverage and cost-plus politics) is widening.

The trade is live. And we think it still has legs.

Why the IRA’s Sunset Matters

The IRA surpassed being just an energy bill and instead became a capital allocation regime. By creating multi-decade production and investment tax credits (PTC/ITC) for solar, wind, hydrogen, and storage, it turned renewables into a risk-adjusted investment product. Predictable cash flows, backstopped by Washington. A dream for utilities and developers.

But under Trump’s new proposal, that’s changing.

Solar and wind credits would begin phasing out in 2026 (worth just 60% of their original value) and vanish by 2028.

Monetisation mechanisms (like credit transferability) will remain, but fewer projects will qualify under stricter rules.

Tariffs on solar panels and components (especially from China and Southeast Asia) would increase cost inflation for developers.

Nuclear credits, by contrast, are extended through 2036.

What this means in practice: a two-speed energy market. Nuclear and gas get cheaper to build (relatively). Wind and solar get riskier, costlier, and less protected.

The pressure isn’t just on equity values. Most regulated utilities are heavily indebted, having issued billions in green bonds and project finance tied to IRA-era assumptions. If subsidies roll off while regulatory caps remain, utilities face a margin squeeze that could prompt credit downgrades. Investors need to consider not just equity underperformance, but also a deterioration in credit spreads and the risk of forced equity issuance.

The Global Realignment: Net-Zero Fatigue

If the IRA was America’s green subsidy cannon, the global trend is a slow-motion surrender of decarbonisation timelines.

Europe is struggling with energy security post-Ukraine, leading to coal restarts and gas rebalancing.

Asia is building out fossil generation at a record pace to match industrial needs.

Emerging markets are increasingly sceptical of importing expensive Western ESG frameworks.

AI and chips are demanding power at an unprecedented scale, and that power needs to be firm, not intermittent.

China is a prime example. It boasts the world’s largest solar manufacturing capacity, and yet it approved nearly 100 GW of new coal plants in 2024 alone. The mismatch between green policy rhetoric and brownfield reality is now too large to ignore. Globally, the divergence between climate finance flows and physical energy demand is accelerating. The US shift is not isolated, but instead the domestic leg of a worldwide pivot.

This changing reality is converging with Trump’s new policy framework to reward a specific subset of energy assets—ones that are dispatchable, margin-resilient, and unencumbered by political rate caps.

The Market Is Already Moving… But Not Done Yet

Take a look at the first chart:

Since early 2025, Constellation (CEG), Vistra (VST), and NRG Energy (NRG) have surged as the market began repricing their future earnings power in a higher power-price, lower-subsidy regime. CEG leads the pack, up over 300% in the past year. Vistra and NRG aren’t far behind.

All three are well-positioned:

CEG is the largest nuclear operator in the US and is expanding its natural gas exposure via its acquisition of Calpine.

VST owns a diversified fleet of coal, gas, and nuclear, with strong ERCOT exposure and real leverage to higher wholesale prices.

NRG is more retail-oriented but still benefits from volatility and margin expansion in spot-driven markets.

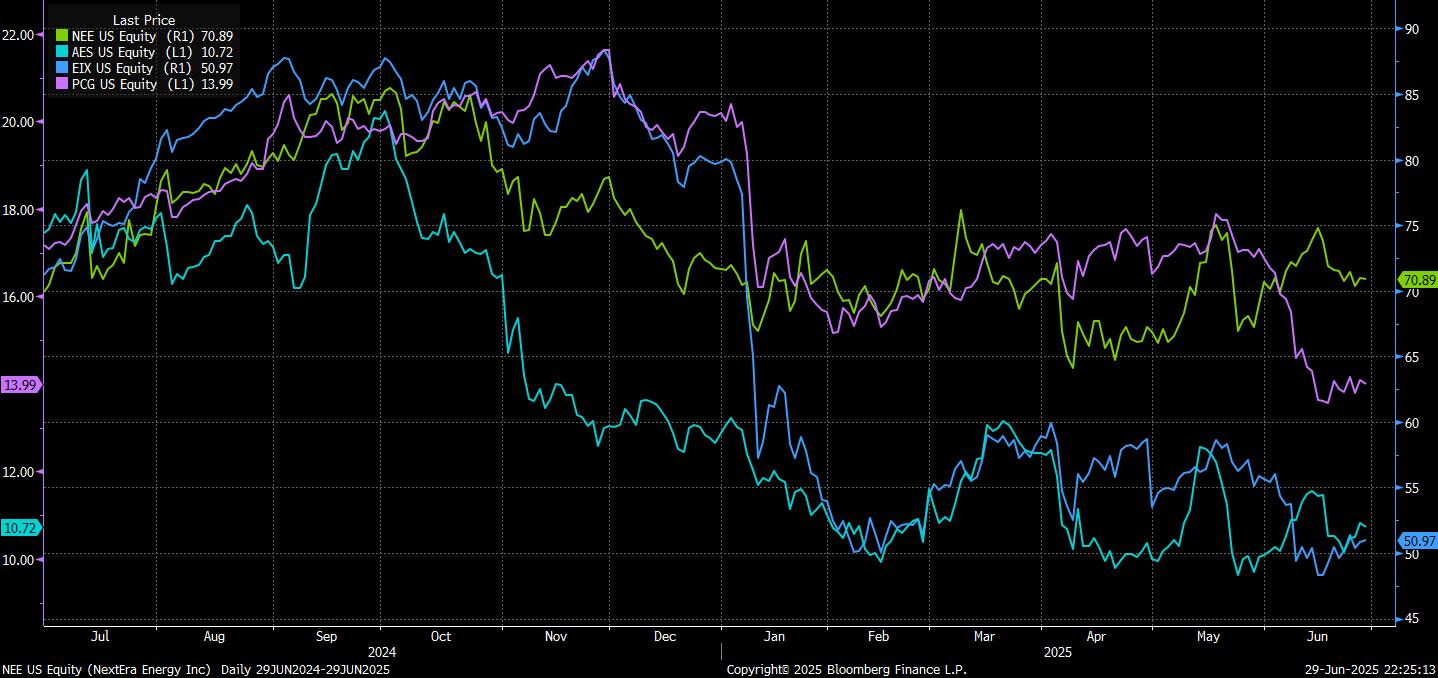

By contrast, look at the next chart:

Names like NextEra (NEE), AES Corp (AES), Edison (EIX), and PG&E (PCG) have struggled. These are the companies most exposed to regulatory lag, wildfire liability, rate cap risk, and renewables margin compression.

The divergence is real.

But here’s the call: we’re still in the early innings.

Most analysts are still running base-case assumptions under old subsidy timelines. Sell-side models continue to assume PTC/ITC regimes remain untouched through 2032. That’s no longer safe. If OBBB passes in its current form, a second wave of earnings revisions and re-ratings is coming.

For the past decade, ESG mandates have mechanically funnelled capital into renewable developers and utilities with green portfolios. But 2024 saw net outflows from ESG-dedicated funds for the first time. As passive ESG flows slow, the cost of capital is normalising, and in some cases reversing. Fossil/nuclear-heavy IPPs, once screened out by ESG filters, are now benefiting from relative valuation compression in renewables. This isn’t just an earnings trade—it’s a capital reallocation.

The Mechanics: Why IPPs Win in This Regime

Three reasons: