Rewiring the Robotics Trade

AI is migrating from the digital world of bits and bytes into the physical world of atoms and photons.

AI has spent the past three years proving that it can write, summarise, and imitate. One of the next phases will be far more commercial: can it lift, sort, grasp, walk, inspect, and do it repeatedly enough to earn a line item in an operations budget? Of course, we’re talking about physical AI.

Nvidia’s (NVDA US) own definition is useful here. “Physical AI” is not just a humanoid that represents the science fiction future we imagined as children, but AI that can understand and interact with the physical world, spanning industrial manipulators, mobile robots, humanoids, and even robot-run infrastructure such as warehouses and factories. In that sense, physical AI is the attempt to turn intelligence into labour.

The installed base is already large before the humanoid dream fully arrives. The International Federation of Robotics says 542,000 industrial robots were installed globally in 2024, taking the worldwide operational stock to 4.664 million units. Physical AI is already underway. It began in factories, fulfilment centres, and logistics networks that already buy automation.

Amazon (AMZN US) is the clearest reminder that the “physical” part of AI need not look like a person to matter. In mid-2025, the company said it had deployed its one millionth robot across more than 300 facilities, making it the world’s largest operator of mobile robotics, while its new DeepFleet foundation model is designed to improve fleet travel time by 10%. Far from science fiction. Long before a humanoid folds your laundry, a more prosaic machine will probably move your parcel.

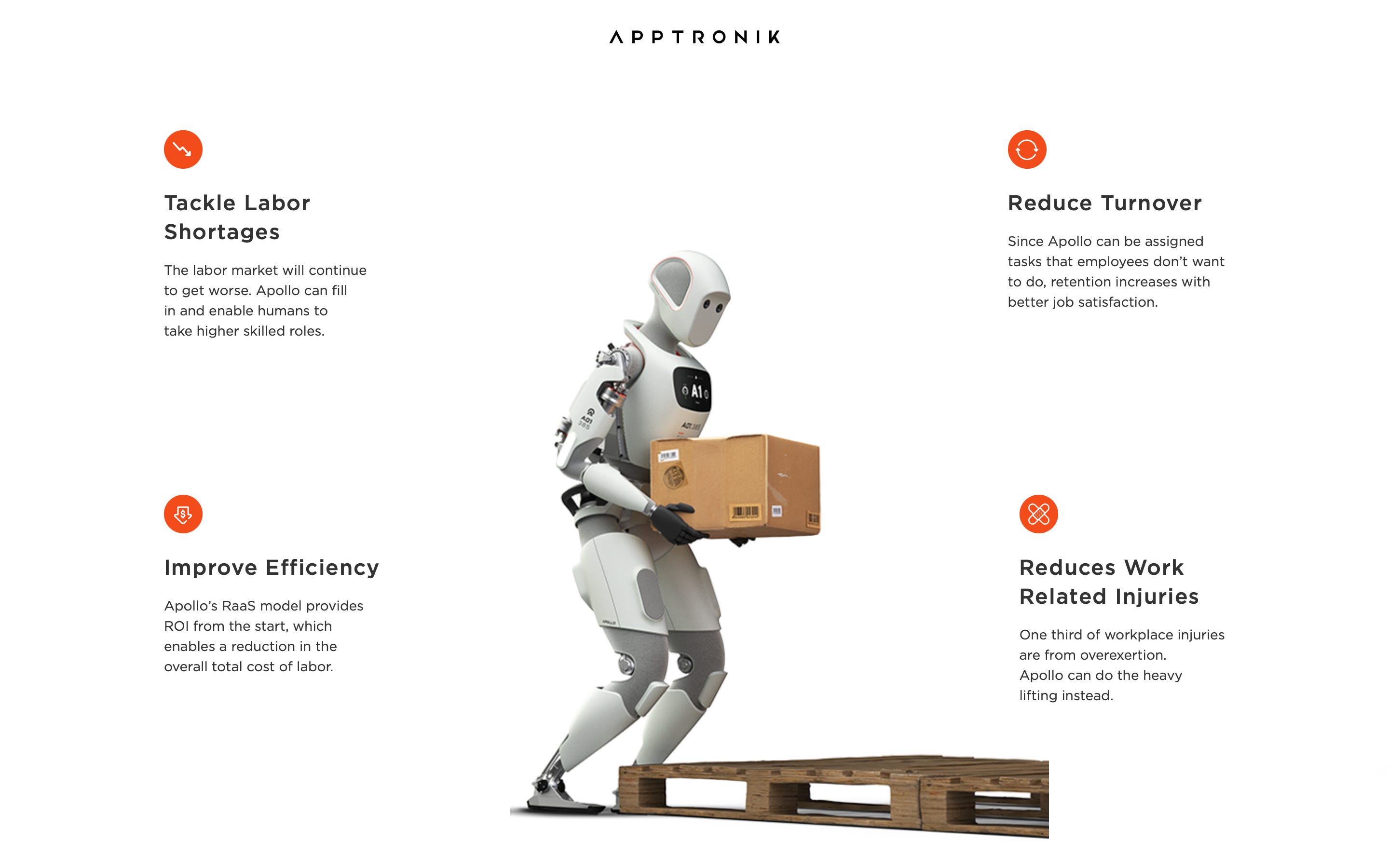

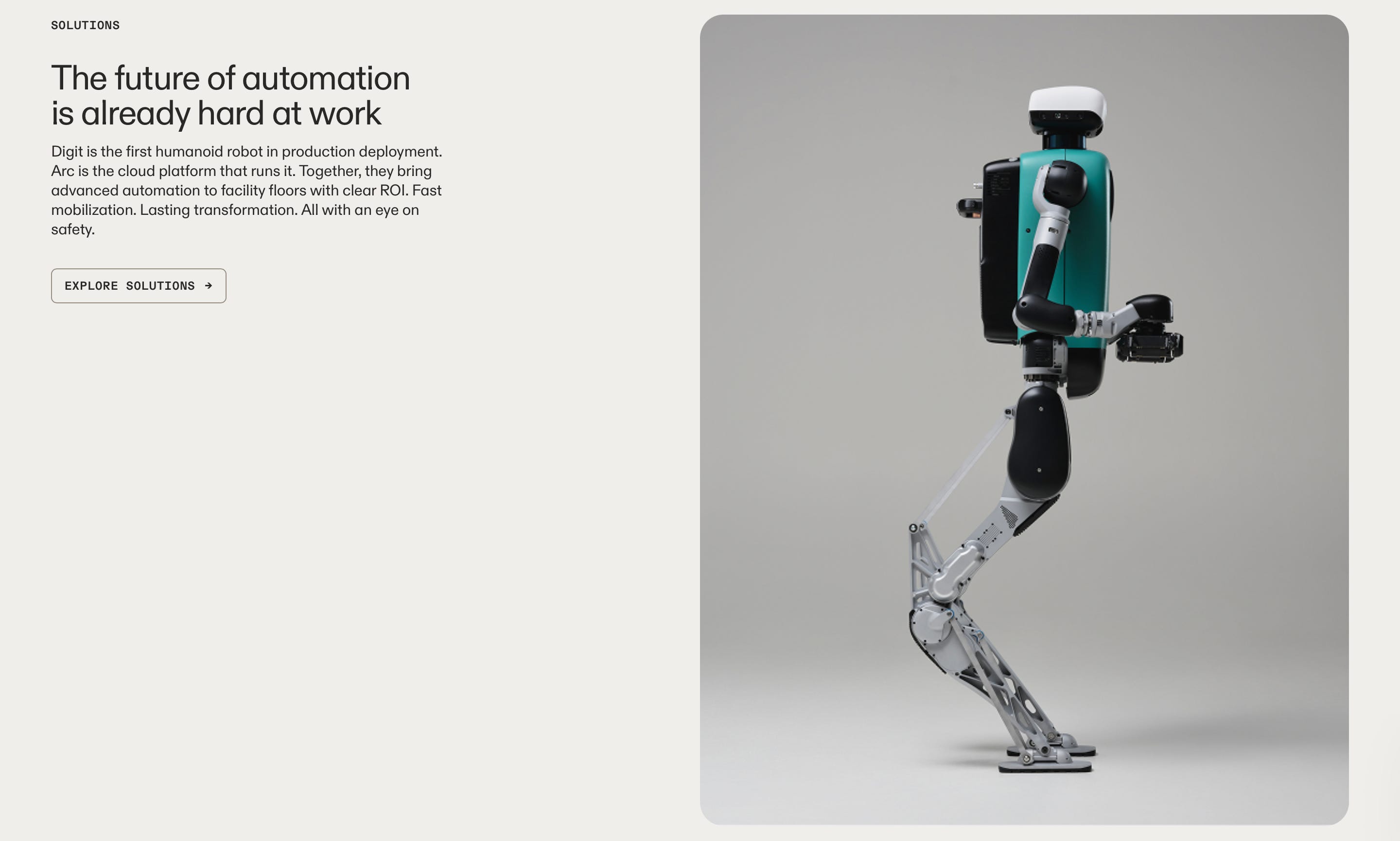

Humanoids, though, are where the imagination and the optionality sit, because the world is built to human dimensions. Apptronik says Apollo1 (a General Purpose Humanoid Robot) is designed to work in areas built for people, and Amazon made the same point about Agility’s Digit2: its size and shape are suited to buildings designed for humans. Figure’s 11‑month deployment at BMW’s Spartanburg plant gives the best recent evidence that this is moving, slowly, from concept to shift work: its Figure 023 robots ran 10-hour shifts, loaded more than 90,000 parts and contributed to the production of more than 30,000 X3 vehicles. GXO, meanwhile, says it has trialled three humanoid prototypes and was the first logistics provider to deploy such technology in a live operating facility.

This is the real split in the theme. The public sees the sci-fi skin, while corporates see another way to fill a repetitive task in a human-native space.

The Market Shift

This theme has plainly become louder over the past year. Investor interest in embodied AI accelerated meaningfully after Jensen Huang’s CES presentation on physical AI and robotics in 20254, adding that it was fielding questions daily from investors on how to express the theme in public markets. By January 2026, Arm Holdings (ARM US) had reorganised to create a dedicated Physical AI unit. In market terms, that is how a phrase becomes a sector. Humanoids are the next phase of the AI hype cycle, but turning viral machines into useful workers remains difficult and expensive.

The reason the fascination is not only promotional is that the underlying software stack has improved meaningfully. Nvidia’s Isaac GR00T N1, launched in March 2025, is presented as the first open humanoid robot foundation model and is paired with synthetic-data generation blueprints and a robotics physics engine. Figure’s Helix, unveiled in February 2025, is a vision-language-action model that combines perception, language and whole upper-body control, and Google DeepMind’s Gemini Robotics and Gemini Robotics‑ER extend Gemini 2.0 into robotic action, embodied reasoning and spatial understanding. In non-technical terms, the market hears that large-scale AI may now translate language and perception into motor control with fewer hand-coded rules and more generalisation.

Embodied AI may be a secular trend even while many of its listed beneficiaries still look, and are priced, like industrial or automation companies. The first money made in a theme is often made by the infrastructure.

The Economics of Embodied Labour

The long-run economic case for physical AI is not difficult to sketch. Start with labour. Labour shortages raise recruitment and operating costs, disrupt production, and can weaken growth and innovation. The UN’s latest population work points to a world that is ageing steadily, with the global population aged 65 and above projected to reach 2.2 billion by the late 2070s, surpassing the number of children under 18. Sure, we’re not looking at 2070 for this thesis to play out, but it goes to illustrate the direction of travel. GXO makes the same point from the warehouse floor, arguing that growth in the working-age population is slowing. This is the first durable pillar of the theme: in many rich economies, the question is whether there is enough labour in the right place, on the right shift, at the right cost.

The second pillar is that the human form can be economically convenient. Humans designed the world for the human body, so a humanoid can, in principle, operate without a full factory redesign. Mercedes-Benz said much the same when it announced its Apollo pilot, noting that humanoids could automate physically demanding, repetitive tasks in spaces designed for people, not robots. For a meaningful class of environments (brownfield logistics, general manufacturing, internal transport, tote handling, machine tending), the retrofit burden can be lower than many sceptics assume.

The third pillar is the cost curve, and here the market should watch what is already happening. Morgan Stanley estimates that the cost of a humanoid in a high-income country may fall to around $150,000 by 2028 (from $200,000 in 2024) and $50,000 by 2050, with lower-income supply chains potentially far below that. Meanwhile, Unitree’s G1 is currently listed at $13,500 on the company’s own shop page. Those are not like-for-like products in capability, of course, but the hardware price tag is coming down, especially at the lower and narrower end of the capability curve. When paired with software improvements, an absurd prototype becomes a tolerable capital request.

The fourth pillar is the financing model. In the latest IFR service-robot dataset, professional service robot sales reached almost 200,000 units, with transportation and logistics accounting for 102,925 units, or 52% of the market. This is already the most commercial part of the physical AI stack: mobile robots moving goods through warehouses, factories and hospitals. The category grew 14% year-on-year, while robots-as-a-service adoption in transportation and logistics rose 42%, with the broader RaaS fleet up 31%. The payment model turns robotics from a capex decision into an operating-cost decision, allowing the technology to get out of the demo room and into the P&L. Apptronik explicitly pitches Apollo through a RaaS lens, arguing that it can deliver ROI from the start and reduce total labour cost.

The fifth pillar is the learning flywheel. Nvidia says synthetic data, simulation and post-training are central to robot improvement, while Amazon’s DeepFleet shows that once large robotic fleets exist, software can extract additional efficiency from the installed base. This is what makes the sector potentially self-reinforcing. More deployments produce more data > more data produces better policies > better policies improve ROI > better ROI produces more deployments. The bridge years are unlikely to be cleanly autonomous. They will probably be messy, with narrow-task deployments, supervised autonomy, and staged roll-outs. But economically, that’s good enough. Markets rarely wait for perfection if acceptable productivity arrives first.

The Bottlenecks

“Bottlenecks” might be the most featured word in research this year. However, Dexterity remains the most underappreciated hurdle. Useful robot models must be general, interactive, and dexterous. Many everyday tasks still require fine motor skills that remain difficult for robots. One of the top hardware failure points in the field was the forearm, a subsystem constrained by tight packaging, dexterity demands and thermal limits. The machine can look splendid in a demo and still lose a shift to heat, cabling, or wrist complexity.

Battery life, payload, grip quality, and stability are equally unforgiving. Apptronik’s own specifications still centre on a four-hour battery pack and a 55-pound payload, while GXO says its field feedback has focused on battery life, ability to carry heavier loads, floor stability, dexterity, and integration with other automation. In other words, the three unlovely ingredients of industrial reality (uptime, safety, and interoperability) are still doing the vetoing.

Timing, then, is the issue. Morgan Stanley’s forecasts assume adoption remains relatively slow until the mid-2030s, with acceleration later in the decade, and it expects roughly 90% of humanoid use in 2050 to be industrial or commercial rather than domestic. Investors should think in layers: arms and AMRs are already commercial, humanoids in structured industrial settings are the emerging wedge, and the household generalist remains the expensive mirage that sells narrative before it sells units.

So, who are the beneficiaries in the short-term?

A Public-Markets Basket for Physical AI

To build a public-markets basket around physical AI today, we would avoid the temptation to bet everything on one future humanoid champion. Most of the marquee OEMs are still private, and the listed route is cleaner through the stack: compute, simulation, factory automation, motion control, machine vision, and precision components. Morgan Stanley’s “Humanoid 100” value-chain framing is the right instinct (more details of this further on). Deployed automation already exists, while the sexier part of the story is only just entering controlled commercial use. The best basket is therefore a barbell between AI infrastructure and industrial incumbency.