It has been instructive to see which of this year’s early convictions have survived contact with reality. Precious metals are attempting to redeem their bull-market credentials, with gold and silver making a valiant effort to recover. The USD/JPY trade has recovered a majority of its post–rate-check slide, an uncomfortable reminder for those who chased the move lower. Meanwhile, at the tip of the risk spear, Bitcoin continues to trade heavy.

Most consensus trades are bruised, but still fighting.

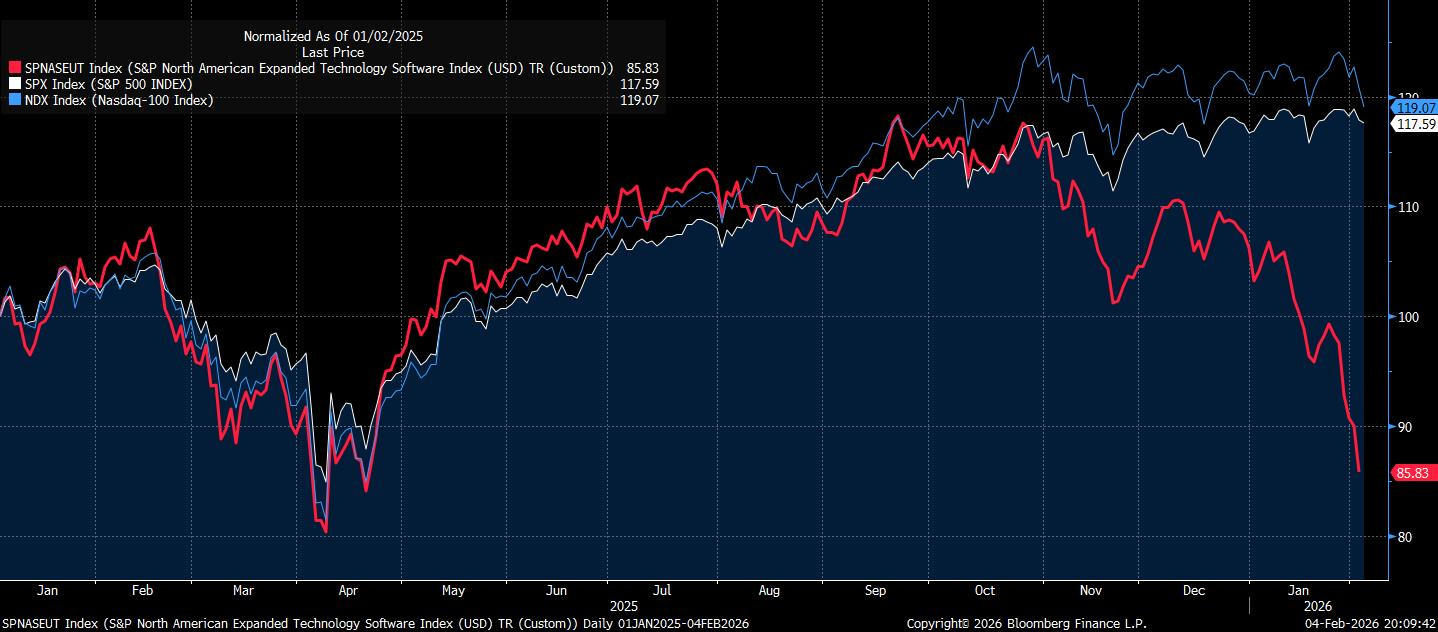

The AI trade, however, has turned the page to a harsher chapter. Over the long arc, artificial intelligence should be pro-equity, and we believe it will be: productivity up, margins up, multiples justified. In the meantime, it is indiscriminately killing SaaS stocks.

The catalyst of the recent software slaughter is Anthropic’s new tooling, Claude Code and Cowork (as well as other “vibe-coding” startups), which repositioned AI capabilities from a clever assistant to a junior employee. While various business models are threatened, software-as-a-service is particularly vulnerable. AI-native firms can often offer quicker and cheaper solutions, meaning companies that once operated in a defensible sector are now at risk of competition from new players. Users with no coding experience can now build software, dramatically lowering the programming skill barrier and undermining rigid, one-size-fits-all products.

Markets are in a shoot-first, ask-questions-later environment. Guilty until proven innocent.

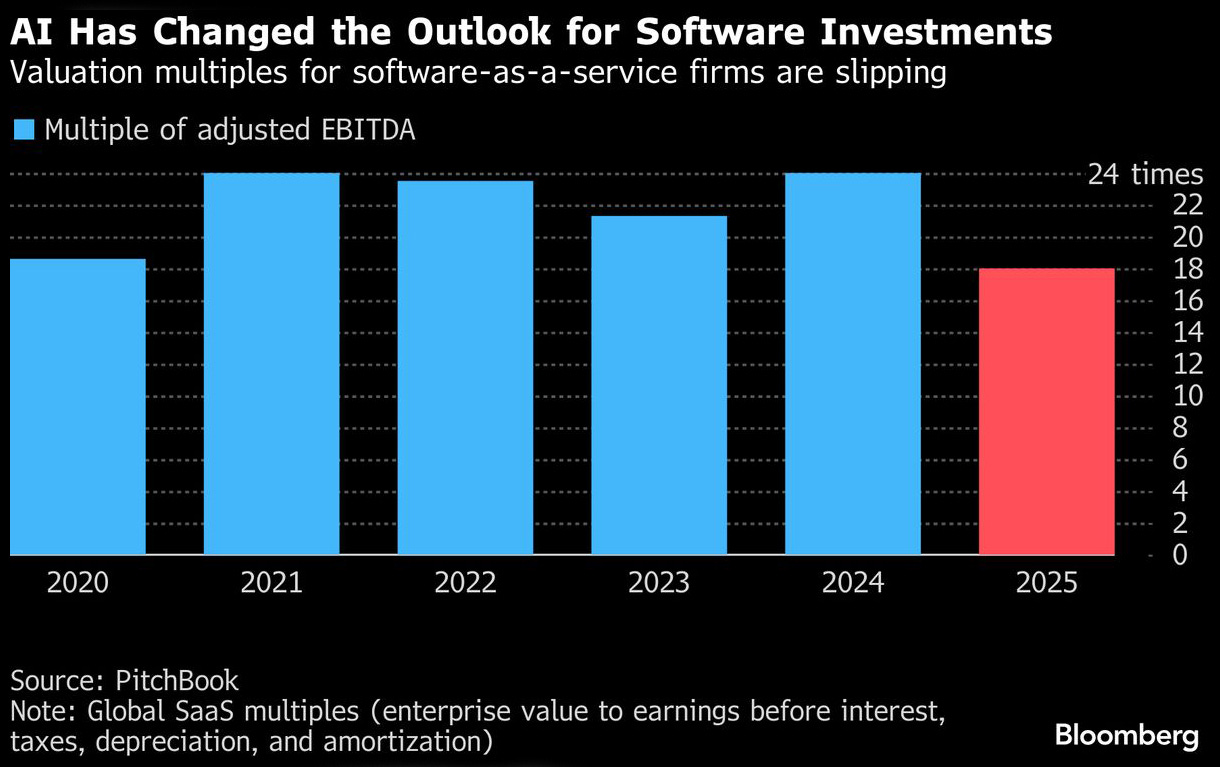

The other casualty is private equity’s decade-long software binge, something credit desks have started calling “Loan-aggedon.” Wall Street’s largest alternative-investment firms are under pressure, driven by fears that artificial intelligence-driven disruptions would cause steep losses on their books. Blue Owl (OWL US), built on financing software businesses and a name we hold short exposure to in the portfolio, now trades where it last did in September 2023.

The latest leg lower reflects mounting concerns about the fallout that AI will cause among software companies, many of whom received funding from alternative asset managers at lofty valuations. UBS Group AG analysts this week estimated that private credit could see default rates surge to as high as 13% if the disruption is aggressive.

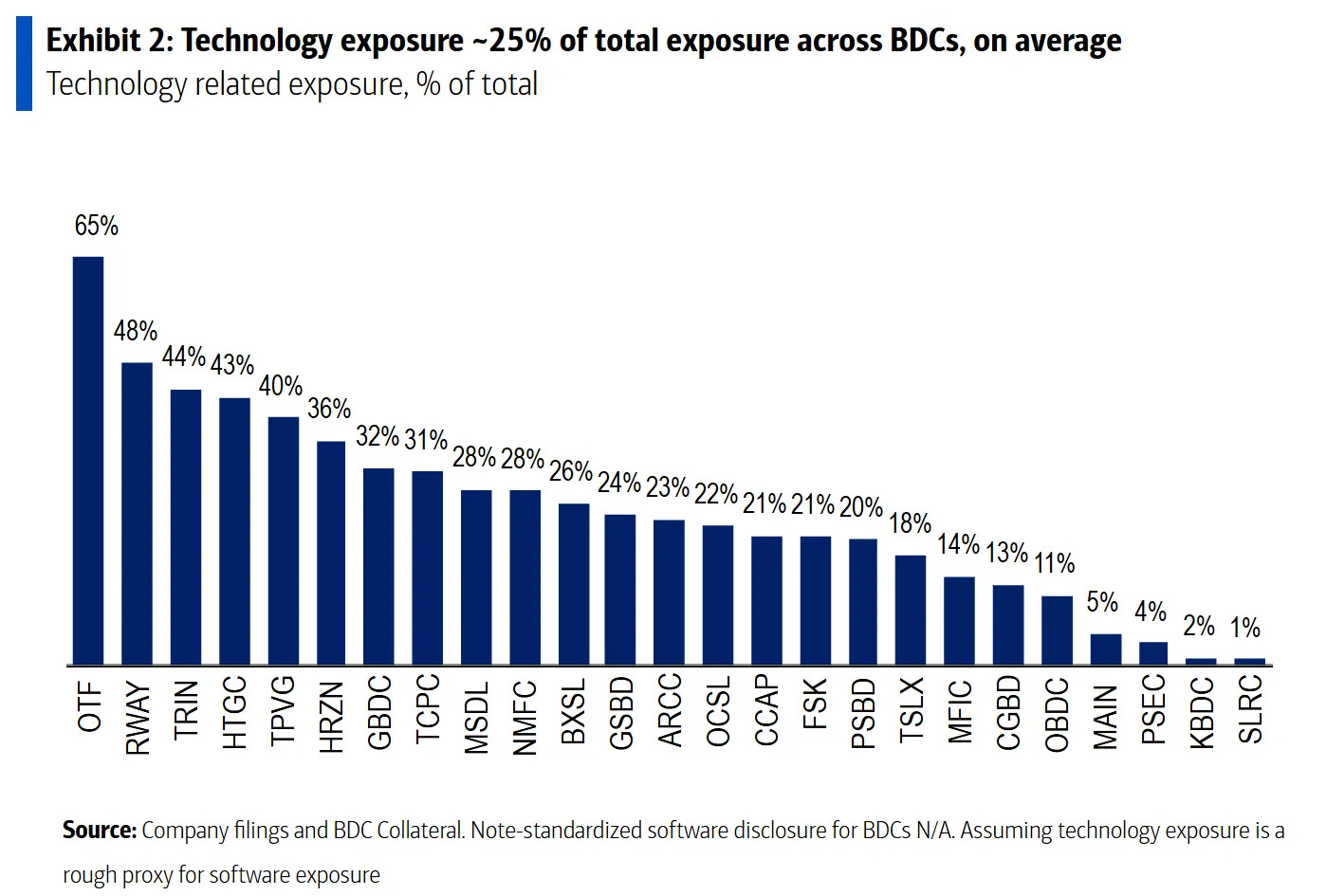

Anxiety about software has been simmering for months, but in recent weeks has boiled over into the leveraged-loan market, and this week the splash reached alternatives and business development companies (BDCs). Shares of BDCs, which pool private credit loans, have also hit multi-year lows as investors assess the level of software exposure in their portfolios. The lack of reporting means that while shares may trade daily, their portfolio health is only updated quarterly.

The SaaS Slaughter and the Capital Structure

We were not positioned for the velocity of the SaaS unwind and missed the boat with this one, but the momentum leg of this trade may have run its course. Markets occasionally hand out perfect pitches. More often, they do not, and the job is to recognise when the easy money has been made and where the asymmetry now sits.

There are reasonable arguments that the equity slaughter pauses from here, or at least the worst of it is done. Businesses such as Intuit are defended by proprietary data and by the swamp of the US tax code, a moat that even an eager AI struggles to drain. Bank of America made a point on SAP, which is busy turning the threat into a product by embedding its own agents inside client workflows. The market has not yet separated the indispensable from the ornamental.

Our preference is therefore to express the theme lower in the capital structure. The loan market offers cleaner asymmetry. More than $17.7bn of US technology loans have slipped into distressed territory over the past month, taking the total SaaS-heavy distressed pile to roughly $47bn, the largest since 2022. Equity can stabilise on hope and narrative; credit eventually meets the covenant.

This is why we have leaned on shorts in the alternative managers space, with Blue Owl the clearest expression in the portfolio to date. The risk-reward here is more convex than in listed software. Equity can stabilise on a story about reinvention. Private credit cannot mark to a narrative forever.

The structure of the business model compounds that problem. Alternative managers collect fees on assets, not outcomes, and many of these assets were financed at lofty valuations with thin equity cushions beneath them. The risk/reward is therefore skewed. Upside is capped at maintaining current marks and fee streams, and the downside is disproportionate because loan recoveries rank ahead of the manager’s equity. When underwriting assumptions fail, the write-downs bypass the fee layer and land directly on shareholders.

Unlike SaaS equities, where prices can overshoot and rebound on a single product announcement, the credit cycle moves in arrears. Defaults arrive with a lag, restructurings grind on for quarters, and quarterly reporting means investors discover the damage in instalments. Slow recognition on the way down and capped participation on the way up is why we prefer expressing the theme through shorts in the financiers rather than the software itself.

Per Barclays, BDCs have around 20% of their portfolios tied to the sector. However, if a software company sells into healthcare, many funds classify it as healthcare exposure. The result is that true software risk is materially higher than headline allocations suggest.

Some words from the Street…

UBS: While the timing of future disruption remains uncertain, under an “aggressive AI disruption” scenario, we expect defaults to rise unevenly across markets to 2%-4% in high yield, 6%-8% in leveraged loans, and 12%-13% in private credit.

Citigroup: We initiate an underweight recommendation on software loans, in line with our general cautious positioning in the asset class. In our view, yields in the 6%-8% range for much of the sector mean it has limited appeal beyond real money and CLO investors.

Morgan Stanley: We like shorting loan total return swaps vs. high yield total return swaps on the back of higher software exposure and worse convexity.

Barclays: Software equities are down around 15% YTD, and software BSLs have declined 3-4 points in the past few weeks. At a minimum, this decline could increase the LTVs of the loans that BDCs make to the sector. More serious risks include possible obsolescence of some software borrowers, which could introduce more material asset quality issues in BDC portfolios.

Alongside our short position in OWL US, we’re adding short exposure to ARES US and KKR US.

As we get underway in the second month of the year, the lesson learned is that 2026 will sort the AI winners from the AI victims, and the scarce skill will be avoiding the latter rather than discovering the former. For now, we would rather own the data centres, the GPUs, the robotics, and short the financiers than chase a SaaS rebound or further leg lower.

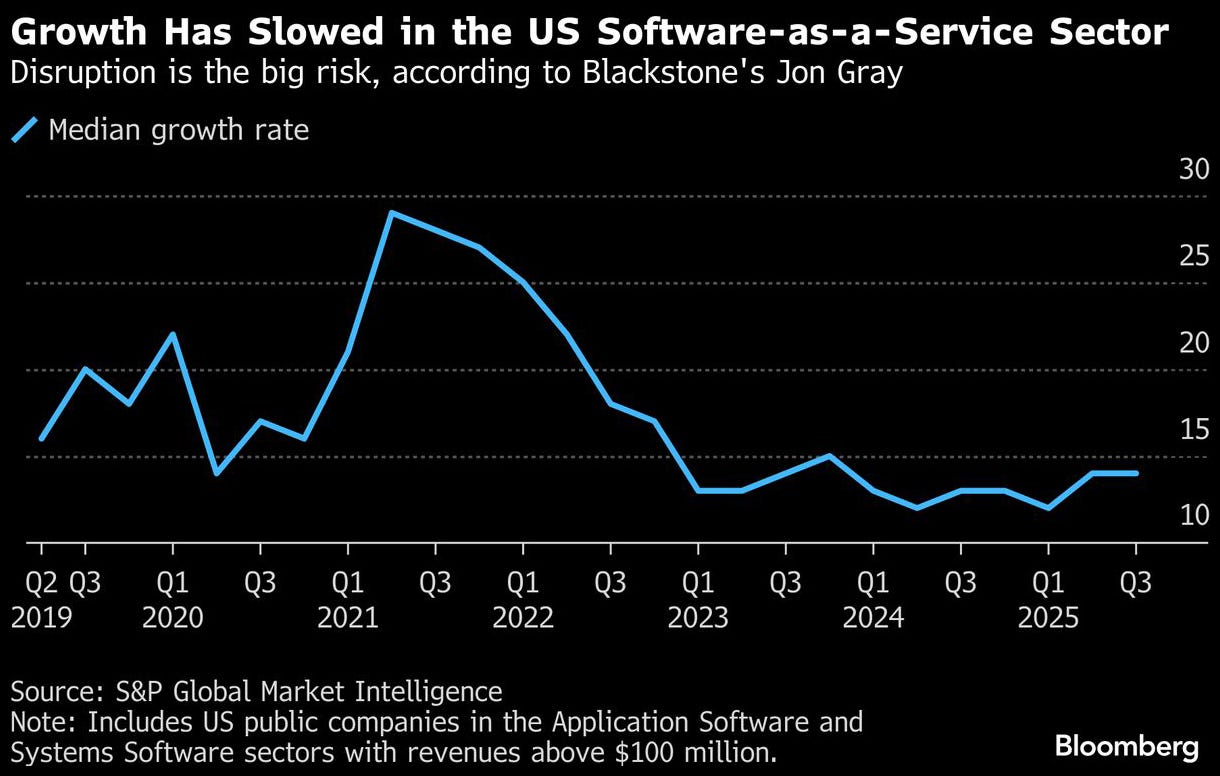

“Everyone’s focused on these bubble risks, I think the biggest risk is actually the disruption risk. What happens when industries change overnight, like what we saw to the Yellow Pages back in the nineties when the Internet came along?” — Jon Gray, Blackstone

AP

reread this :) how many cockroaches are there hiding? it is hard to believe atm that there will be a comeback for SAAS + interesting to witness what the inflation expectations + potential fed tightening will do to those loans which will need to be refinanced 🏓

Really good piece here!