Markets tend to assume that geopolitical crises escalate until something breaks. History suggests the opposite is often true. The moment when investors begin to imagine the worst is often when the incentives to avoid it become overwhelming.

The confrontation around Iran has quickly become one of those moments. Oil has surged, tanker traffic has slowed almost to a stop, and risk assets have been forced to price a scenario that earlier this month sat firmly in the tail of the probability distribution.

Yet crises are rarely governed purely by ideology or military logic, and are more often constrained by economics, domestic politics, and the basic question of who, if anyone, actually benefits from prolonging the conflict.

Viewed through that lens, the current standoff begins to look less like the start of a long war and more like a high-stakes game of incentives (something we should be used to in Trump-office markets). And once those incentives are mapped out, several conclusions follow, including one that markets may not yet fully appreciate.

Hormuz has to reopen.

Problems in the Strait

At a fundamental level, a prolonged conflict is not in the economic or political interest of most actors involved, including Iran itself.

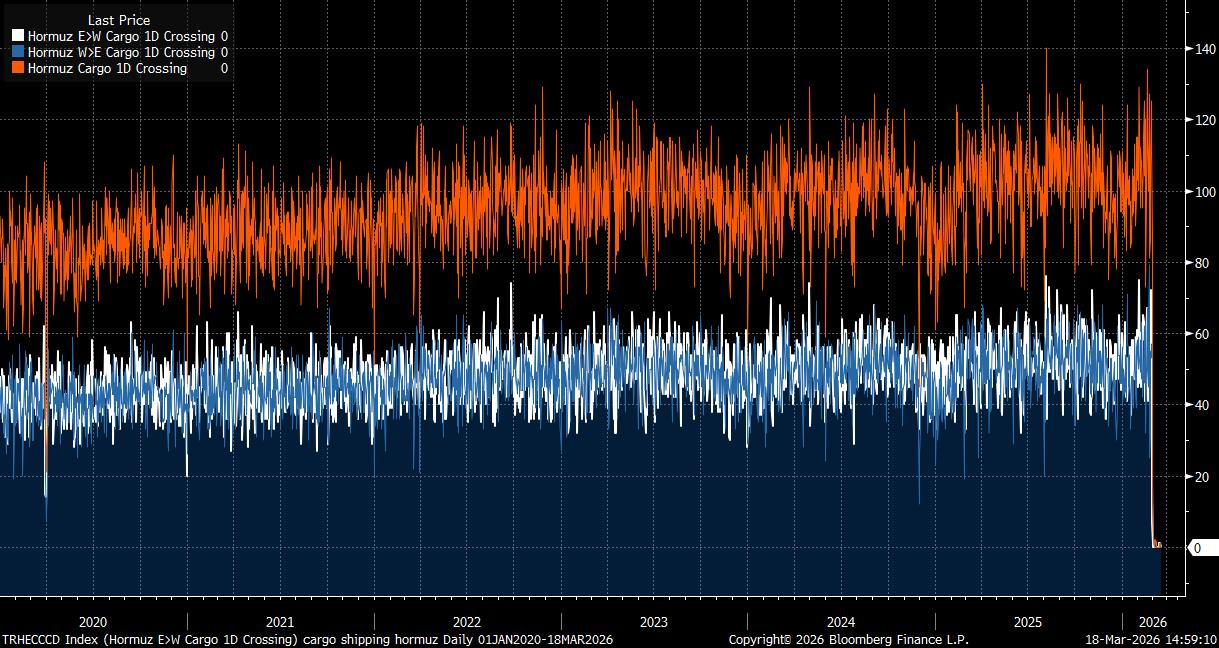

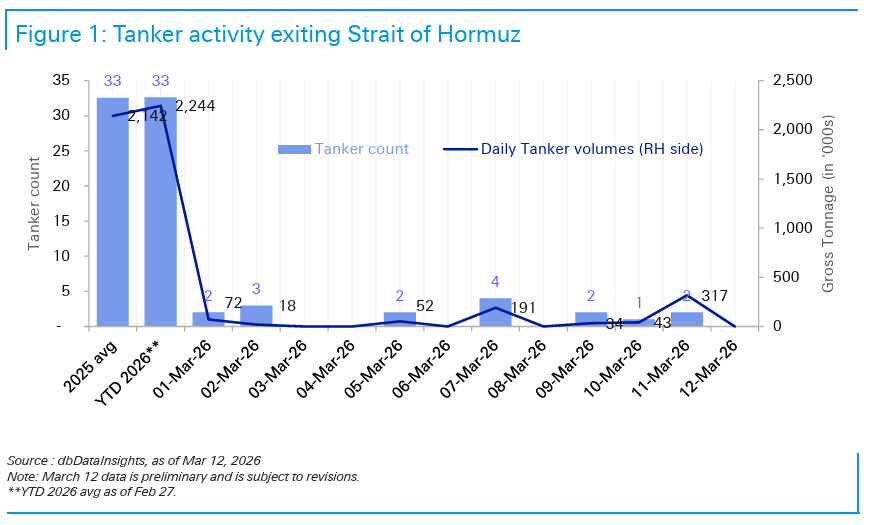

The Strait of Hormuz, through which roughly 20% of global oil and LNG flows transit, is a critical artery not only for Gulf exporters but also for Iranian crude shipments. Sustained disruption would therefore undermine Iran’s own ability to export oil (much of which is sold to China) and deprive the regime of one of its most important sources of foreign currency. Even amid the current crisis, tankers carrying Iranian crude have continued to transit the strait toward Asia, highlighting Tehran’s reliance on the route for revenue.

A similar logic applies to the broader region. Gulf producers, Asian importers, and Western governments all have strong incentives to prevent a durable closure of Hormuz, given the scale of global supply at risk. Tanker activity has slowed to a snail’s pace, with severe implications for global growth and energy prices if it continues for much longer.

Trump Has an Eye on Midterms

From a domestic political perspective, there are also strong incentives for the White House to avoid a prolonged conflict. President Trump has historically framed his foreign policy around decisive outcomes and rapid demonstrations of strength rather than open-ended military engagements.

A drawn-out confrontation with Iran risks undermining that narrative, particularly if it results in sustained instability in energy markets, higher fuel prices for US consumers, or the perception that Washington has been pulled into another costly Middle Eastern conflict. With the US midterm elections approaching, the administration will likely be acutely aware that geopolitical crises can quickly become domestic political liabilities.

Energy prices are particularly sensitive in this context. A persistent spike in crude would feed directly into gasoline prices, a metric closely watched by voters and historically correlated with shifts in political sentiment. For any administration heading into a midterm cycle, a sharp increase in pump prices can act as a powerful amplifier of broader concerns about inflation and the cost of living.

The optics are therefore important: a conflict that drives oil materially higher risks turning a geopolitical event abroad into an economic grievance at home.

In that sense, the political calendar matters. Midterm elections often serve as referendums on the incumbent administration’s economic management and overall competence. Allowing a geopolitical crisis to evolve into a persistent economic shock, particularly through higher energy prices or financial market volatility, would risk complicating the administration’s domestic narrative at a sensitive moment.

Peak Fear Priced

There are increasing indications that markets may already have priced in peak geopolitical fear around the Iran conflict, which could limit the scope for further large downside moves in risk assets.

Recent price action across asset classes suggests that the most aggressive phase of the risk-off adjustment may already be over (see Brent, G10 STIR, etc.).

Positioning indicators flagged levels of stress comparable to major crisis periods, with volatile markets briefly showing dynamics similar to those seen during the early stages of the pandemic. At the same time, cross-asset repricing was swift and broad, with equities, rates, and commodity markets all rapidly incorporating a higher geopolitical risk premium. This type of sharp, front-loaded adjustment is often characteristic of the point where markets begin to price worst-case scenarios rather than base cases.

From a market-structure perspective, the key point is that large directional moves become harder to sustain once investors have already repositioned defensively. In the latest selloff, the biggest drawdowns occurred in markets that had been the strongest performers earlier in the year, suggesting that investors rapidly reduced risk in crowded positions.

Historically, such episodes of intense repositioning often mark the moment when fear peaks rather than when the decline begins, as the marginal seller becomes exhausted.

Importantly, the focus for markets tends to shift from the absolute level of geopolitical risk to the change in expectations. Even if tensions remain elevated, what matters for pricing is whether conditions are getting worse or simply becoming “less bad.” Once the trajectory of events stabilises, markets often begin to recover even while the underlying geopolitical situation remains unresolved.

The likely outcome is that volatility gradually subsides and the geopolitical risk premium embedded in assets begins to compress as investors reassess probabilities rather than possibilities.

Positioning for De-Escalation

Oil Lower

Buy a 2x1 put spread on COM6 (spot ref 102.50)