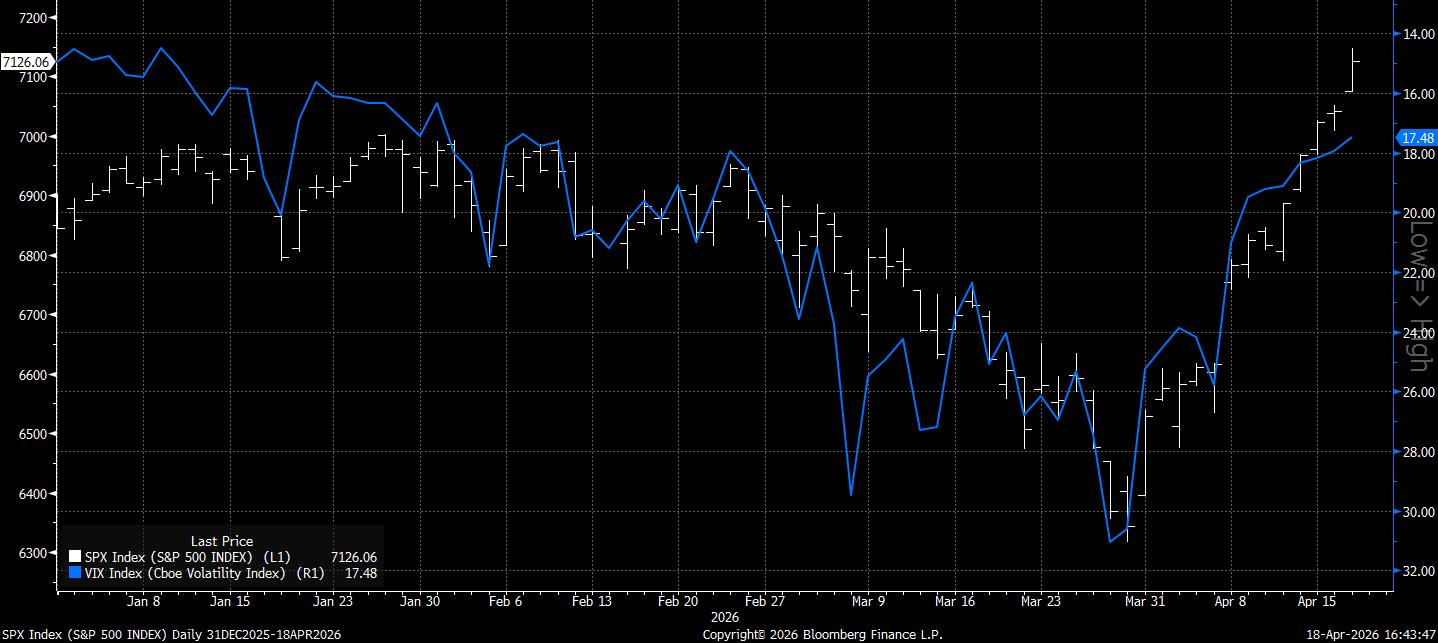

Spot up, vol down, and tail risks lessening. The S&P 500 closed out its strongest week since May with a string of record highs, as markets leaned hard into a de-escalation narrative that, for now, has moved from tentative to tradable. The combination of a holding ceasefire between the US and Iran and the reopening of the Strait of Hormuz removed the most acute tail risks that had defined price action over the past month, allowing positioning to reset quickly and risk appetite to return with force.

A 13% drop in WTI crude acted as the immediate release valve, easing inflation expectations and unlocking a broad rotation into fuel-sensitive sectors. Autos, airlines and discretionary gained, while the unwind in energy positions marked a clean reversal of one of the most crowded trades of the conflict period. Beneath that, however, the move had the hallmarks of a classic positioning squeeze. Heavily shorted baskets surged double digits, and both dealer desks and systematic flows pointed to continued mechanical buying.

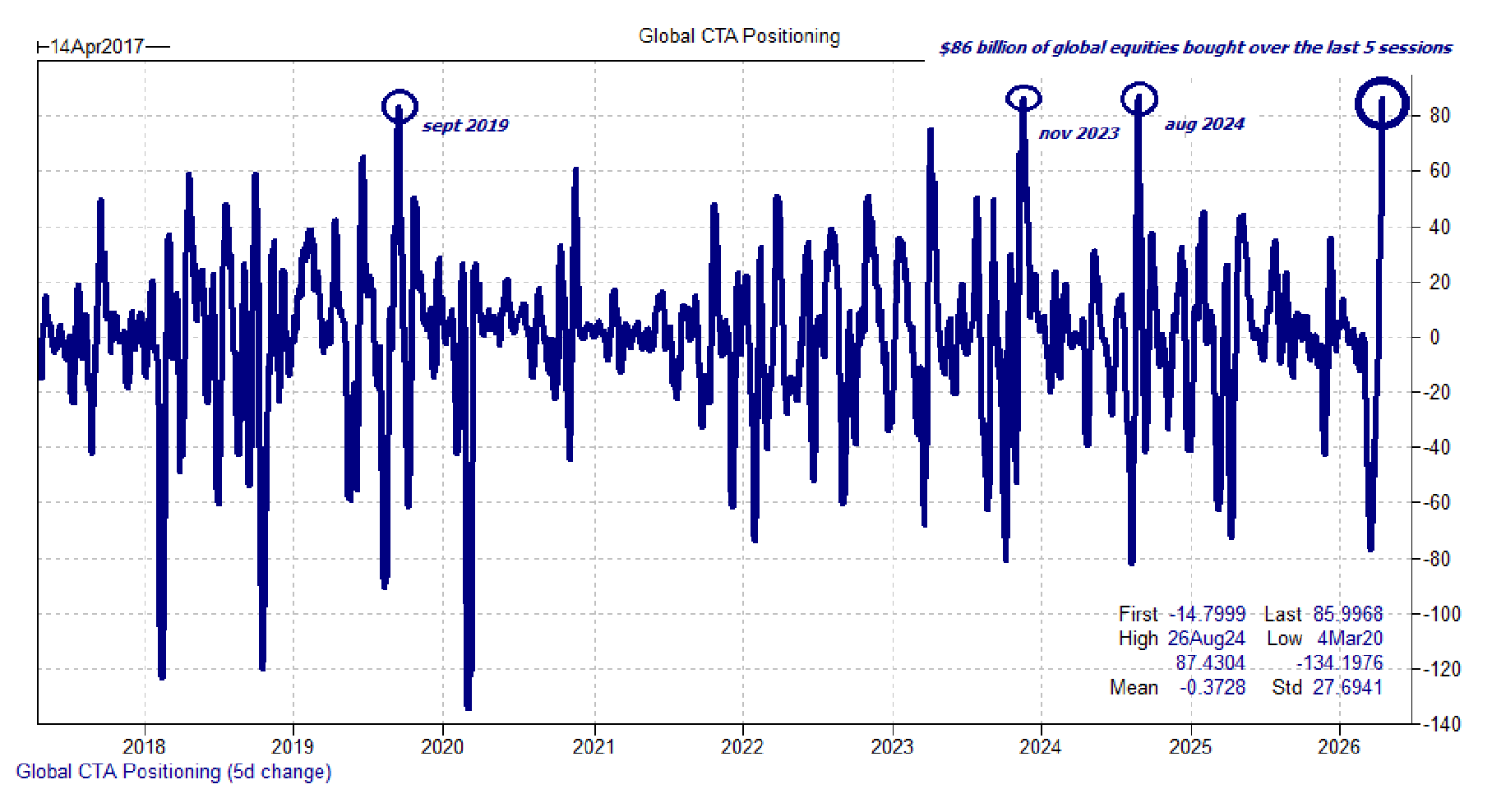

Goldman Sachs estimates a further $70 billion in CTA demand for global equities over the coming sessions, on top of already significant inflows ($86 billion last week), suggesting the rally has been as much about forced participation as about improving fundamentals.

“Previous episodes of accelerated demand have seen short-term consolidation, followed by medium-term strength for the S&P 500,” Goldman Sachs’ Brian Garrett wrote, noting the US index is typically up by an average of 2.2% a month after such a buying spree, and up 8.2% three months later.

Earnings season has not yet provided a clean fundamental confirmation of the move, but it validates an economy that is neither overheating nor rolling over, giving a sturdier foundation for markets beyond the near-term bounce. Bank results were broadly underwhelming, with strong equity trading offset by softer FICC performance, pointing to a more mixed underlying environment than headline index levels might suggest. The market has been willing to look through this for now, aided by upward revisions to full-year earnings expectations, particularly in sectors tied to energy and semiconductors.

Macro data offered a constructive, if incomplete, backdrop. Softer-than-expected PPI and stronger regional activity surveys helped reinforce the idea that underlying demand remains intact as inflation pressures begin to moderate.

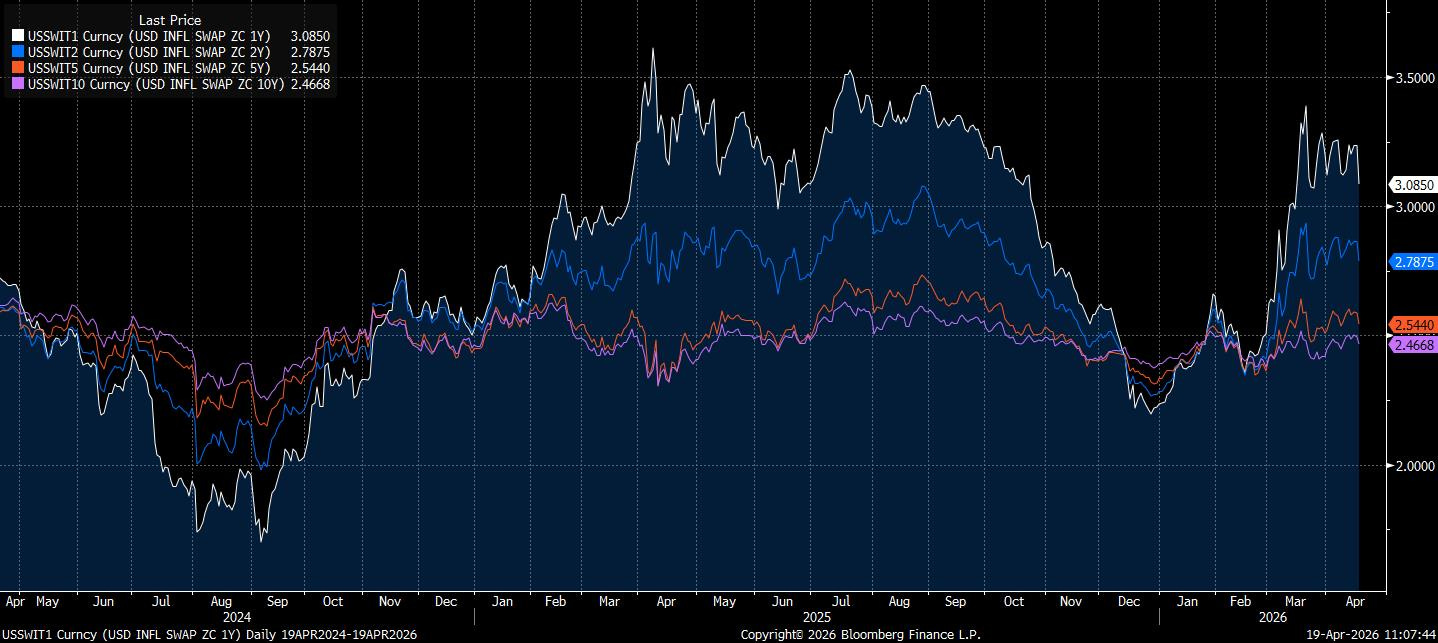

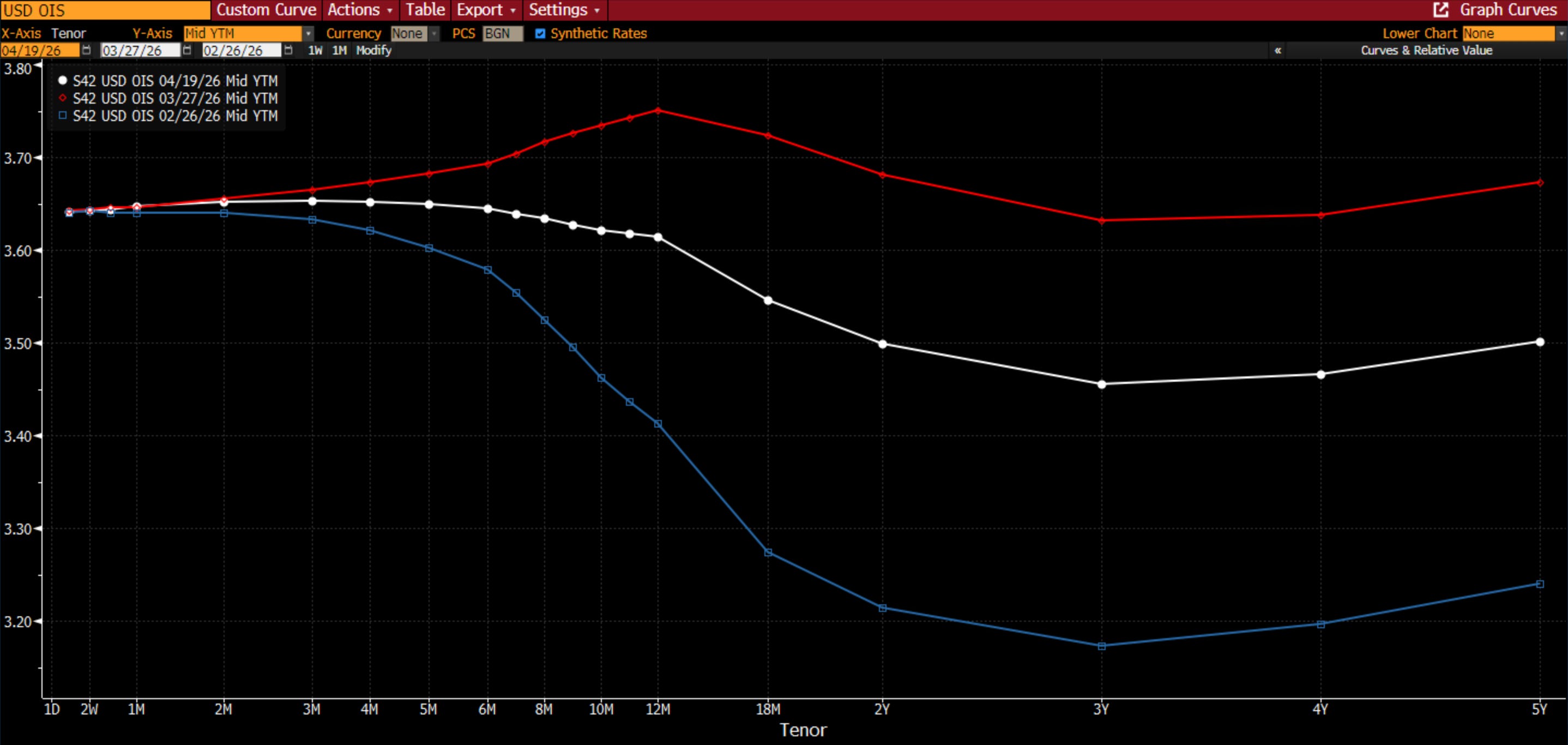

Alongside this, Fed communication continues to emphasise patience, with policymakers broadly aligned around the view that current policy is appropriately restrictive given lingering uncertainty on inflation. The modest re-pricing of rate cuts in OIS reflects that balance, shifting back toward easing (white) but without the conviction seen earlier in the year (blue).

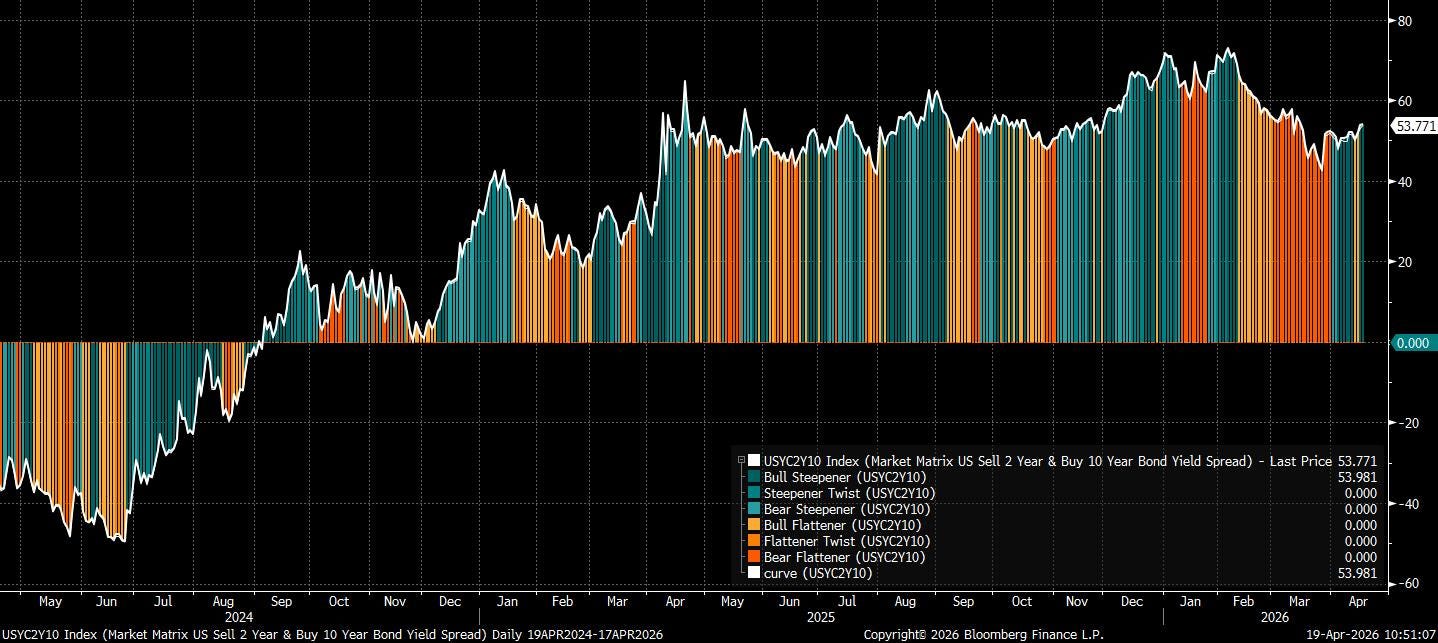

Across assets, the response has been more nuanced than the equity rally might suggest. The dollar weakened sharply as geopolitical risk premia unwound, with positioning and hedging flows now pointing back toward a broader structural downtrend. The decline in oil has allowed for a partial re-steepening of the curve as front-end easing expectations returned. Options positioning, particularly in the 10-year sector, indicates growing confidence in lower yields into the next data cycle.

Taken together, the past week marks a clear inflexion in sentiment, but not necessarily a resolution of the underlying macro tensions. The market has moved quickly to price in a best-case near-term outcome (stable geopolitics, easing inflationary pressures, and resilient growth), but that equilibrium remains fragile. If the ceasefire holds and oil remains contained, there is scope for positioning and flows to carry equities higher in the near term. However, the speed and nature of the rally suggest it is still being driven more by the removal of tail risks than by the emergence of a new, durable macro regime.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“Thematic Leaders and Beta Chasing”

“EZ Rates: Between the Baseline and Adverse”

“Play the Dollar Range”

Thematic Leaders and Beta Chasing

US Equities

What stands out in the current tape is the clarity of behaviour. Leadership has re-emerged quickly, and it is unmistakably high beta. The market has pivoted from discounting a meaningful deterioration in growth to re-embracing the same pro-cyclical, momentum-driven themes that defined the pre-conflict regime.

The cross-section of returns reinforces that point. Month-to-date performance is dominated by Q1 leadership, with capital rotating back into the most reflexive expressions of the AI buildout. Memory has reasserted itself at the centre of that trade. Names such as Teradyne (TER US), Micron Technology (MU US), and Sandisk (SNDK US) — all of which delivered outsized gains into the pre-conflict peak — are once again among the primary beneficiaries of the rebound. The reappearance of these names in the top decile of performance is a re-leveraging of existing narratives.

Alongside this, the speculative layer of the market is behaving as one would expect in a positioning-driven rally. High short-interest baskets, meme equities, and de-SPAC cohorts have all materially outperformed, with month-to-date gains exceeding 20%. This reflects a mechanical unwind of bearish positioning rather than any fundamental reassessment of underlying cash flows. Short covering remains a core driver of the move, and it tends to be self-reinforcing in the early stages of a squeeze. Even Alt AMs and BDCs had a good week.

The chase for speculative beta is also prevalent in the market right now. Short interest, meme stocks, and de-spac baskets… all more than 20% higher month-to-date. The former is a fundamental example of the short covering underscoring this move higher.

Where the signal becomes more nuanced is in the options market. In a typical relief rally, implied volatility compresses in line with rising spot. Yet that relationship has loosened. While the S&P 500 has advanced, implied volatility (proxied by the VIX) has not declined proportionally. Instead, it remains relatively firm, reflecting a market that is not simply adding exposure but actively paying for convexity on the upside.

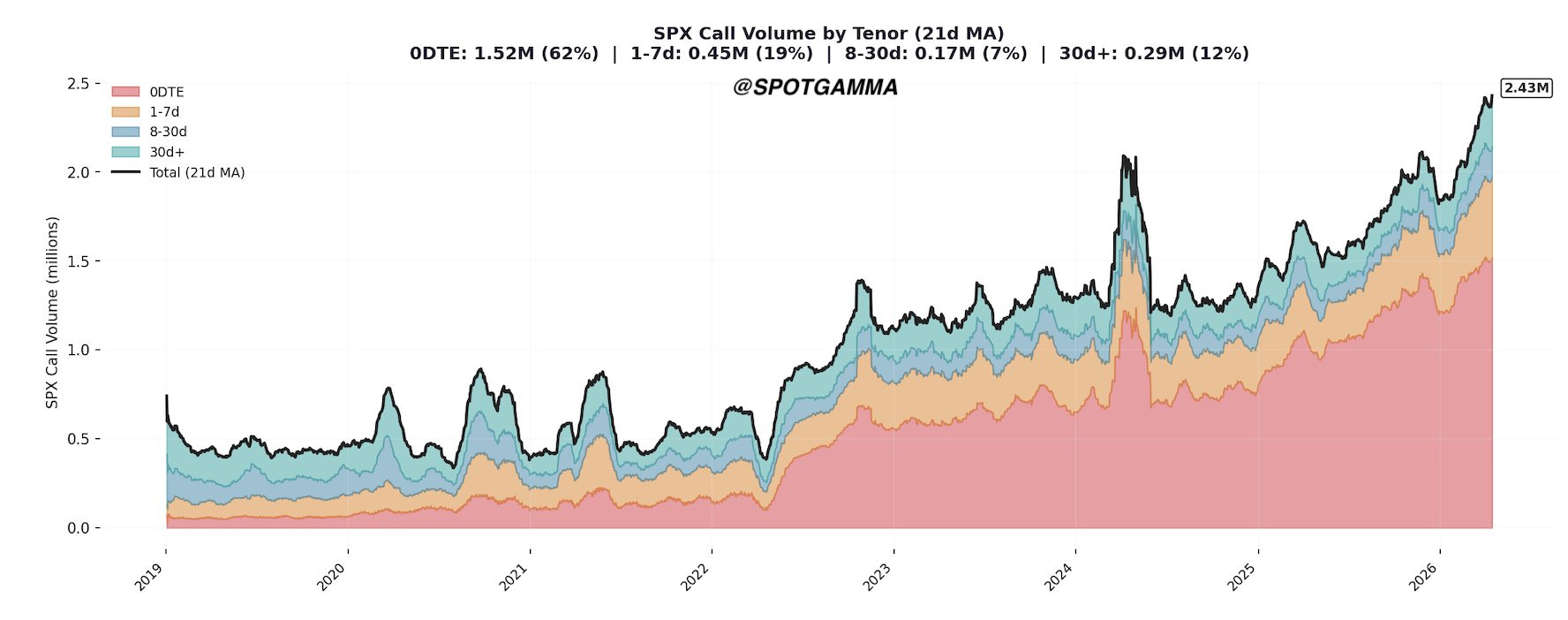

Flow data corroborates this. Institutional call-put ratios have reached their most elevated levels since late 2024, while call skew has repriced sharply higher. Non-0DTE index call volumes have accelerated, and single-name call demand has intensified. Investors are expressing bullish views through leverage.

This matters for the durability of the move. The current options positioning, particularly into expiry this Friday, leans heavily toward calls on a delta-adjusted basis. SpotGamma estimates suggest the latest expiry profile is among the most call-skewed on record, following a double-digit rally in the index over a compressed time frame. That creates a dependency on continued dealer hedging support. Should flows slow, or should investors choose to monetise rather than roll exposure, the hedging dynamic flips. Dealers would move from buyers of strength to sellers of weakness, amplifying any downside move in spot. After all, the tail risks have lessened, but it’s not out of the question for a spanner to be thrown into the works of the negotiation.

In that sense, the rally is increasingly endogenous. It is being sustained by flows that, if reversed, would act in the opposite direction with similar force. That does not invalidate the move, but it does make it more fragile than the surface price action suggests.

From an allocation perspective, the distinction between beta and fundamentals is important. The former has already moved aggressively; the latter still offers more durable entry points. Two areas we like: