The Escalation Trade Is Wrong

A weekly look at what matters and how to trade it. (March 16th)

Stocks extended their decline for a second consecutive week as the war in Iran continued to dominate price action across global markets. Brent crude hovered near $100 per barrel as concerns over supply disruptions intensified, keeping volatility elevated and reinforcing a risk-off tone across asset classes. The S&P 500 briefly stabilised at the start of the week after President Donald Trump suggested the conflict was “very complete,” but the reprieve proved short-lived.

From Tuesday onward, a barrage of geopolitical headlines reignited inflation fears, pushing Treasury yields higher across the curve and extending the rally in the US dollar. By Friday, the index was sitting only marginally above its 200-day moving average, a level many investors had hoped might provide a near-term floor.

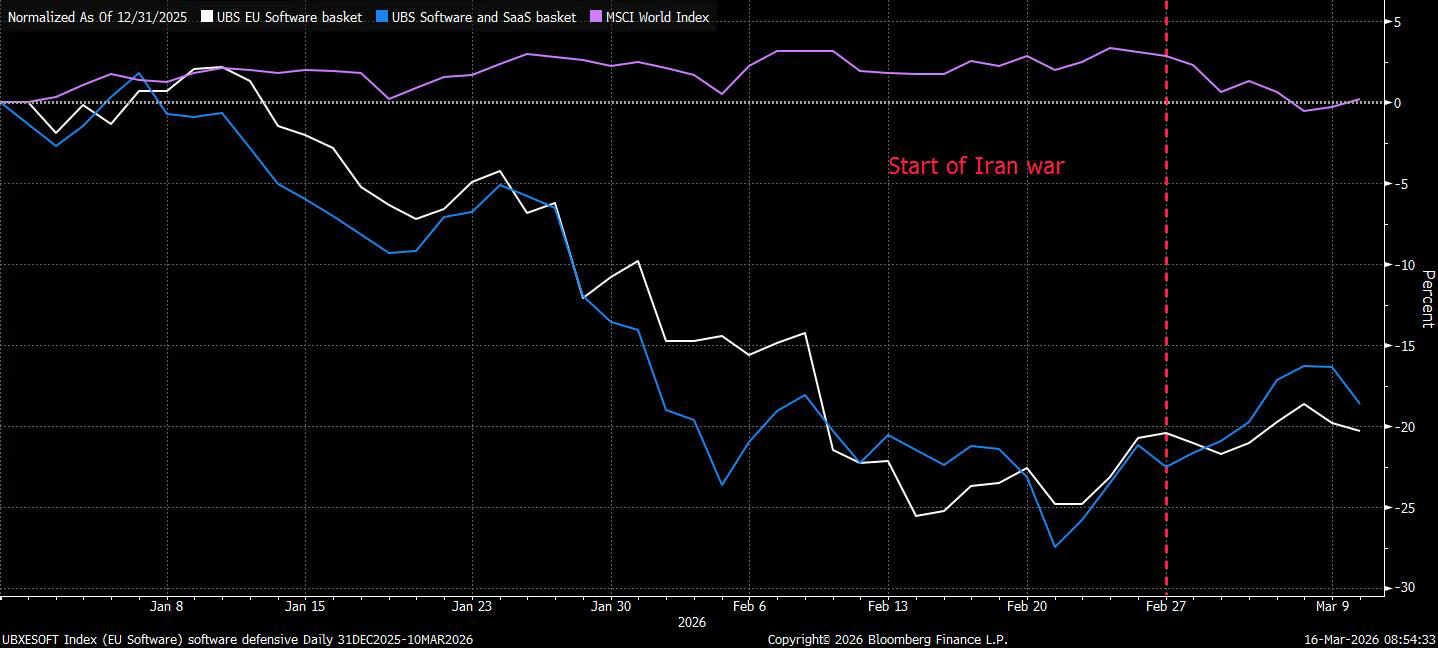

Sector leadership reflected the macro shock. Energy was the only group to post meaningful gains as crude prices surged, while defensive areas such as consumer staples and utilities held up relatively well as investors reduced cyclical exposure. Materials, industrials and consumer discretionary stocks bore the brunt of the selling as markets reassessed the economic implications of sustained high oil prices. Even the Magnificent Seven were not spared: the group slipped into correction territory as higher yields and geopolitical uncertainty pressured valuations. Interestingly, some investors appeared to treat parts of the software sector as a defensive allocation, reflecting the market’s search for businesses less directly exposed to commodity shocks or global trade disruption.

Financial stocks faced an additional headwind as stress in private credit markets intensified. A series of developments highlighted growing liquidity strains across the $1.8 trillion industry, with JPMorgan restricting some lending to private credit funds after marking down software-linked loans and Morgan Stanley and Cliffwater capping withdrawals from multi-billion-dollar credit vehicles following heavy redemption requests. The measures underscore concerns that the long-feared “cockroach” phase of the private credit cycle may be emerging, amplifying downside pressure on bank and asset manager equities.

Macro data did little to offset those concerns. Inflation readings remained elevated even before the latest oil shock, while fourth-quarter GDP was revised sharply lower, reinforcing the increasingly uncomfortable mix of slowing growth and persistent price pressures. Core CPI and PCE held near expectations but remained well above the Federal Reserve’s target, leaving policymakers with limited room to respond if energy prices feed further into inflation. Markets responded by aggressively repricing the rate path, with expectations for easing this year pulled back sharply as the conflict raised the risk of a more prolonged inflation impulse.

Cross-asset moves reflected that shift in macro expectations. The US dollar continued to strengthen as investors sought safety and as higher oil prices supported US terms of trade, pushing one-month risk reversals to their most bullish level in several years. Treasury yields moved higher as well, led by the front end where two-year yields rose more than 15 basis points amid a sharp repricing of rate-cut expectations. OIS markets now price only modest easing through the end of the year, down significantly from the outlook before the Iran conflict escalated.

Taken together, the market is increasingly being shaped by geopolitical dynamics rather than traditional economic drivers. As long as oil prices remain elevated and the conflict shows little sign of resolution, risk assets are likely to remain highly sensitive to headline risk, with the path of energy prices continuing to dictate the broader macro narrative.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“The Incentives to De-Escalate”

“Rate Decisions in a World of Oil Shocks”

“The Next Trade War”

The Incentives to De-Escalate

Reports over the weekend suggest that a potential diplomatic off-ramp may be emerging in the Iran conflict, even as the fighting continues. According to reporting cited by NBC News, US officials say Iran has signalled a willingness to negotiate a ceasefire or broader deal, though the current terms under discussion have been rejected by Washington as insufficient. President Trump said Tehran “wants to make a deal,” but indicated he was not prepared to accept the proposal yet, arguing that any agreement would need to be “very solid” and meet stronger US conditions.