The Fed Put Has Left the Building

A weekly look at what matters and how to trade it. (June 22nd)

A shortened US trading week began with a gap higher after officials in Washington and Tehran confirmed a deal to reopen the Strait of Hormuz, taking another layer of geopolitical risk premium out of crude and giving equities a clean macro tailwind at the open. Oil prices fell, inflation fears eased, and the AI trade quickly reclaimed leadership. SpaceX added to the momentum, surging again in its first full week of trading. If oil risk is falling and AI flows are still alive, investors are not going to spend much time sitting in cash.

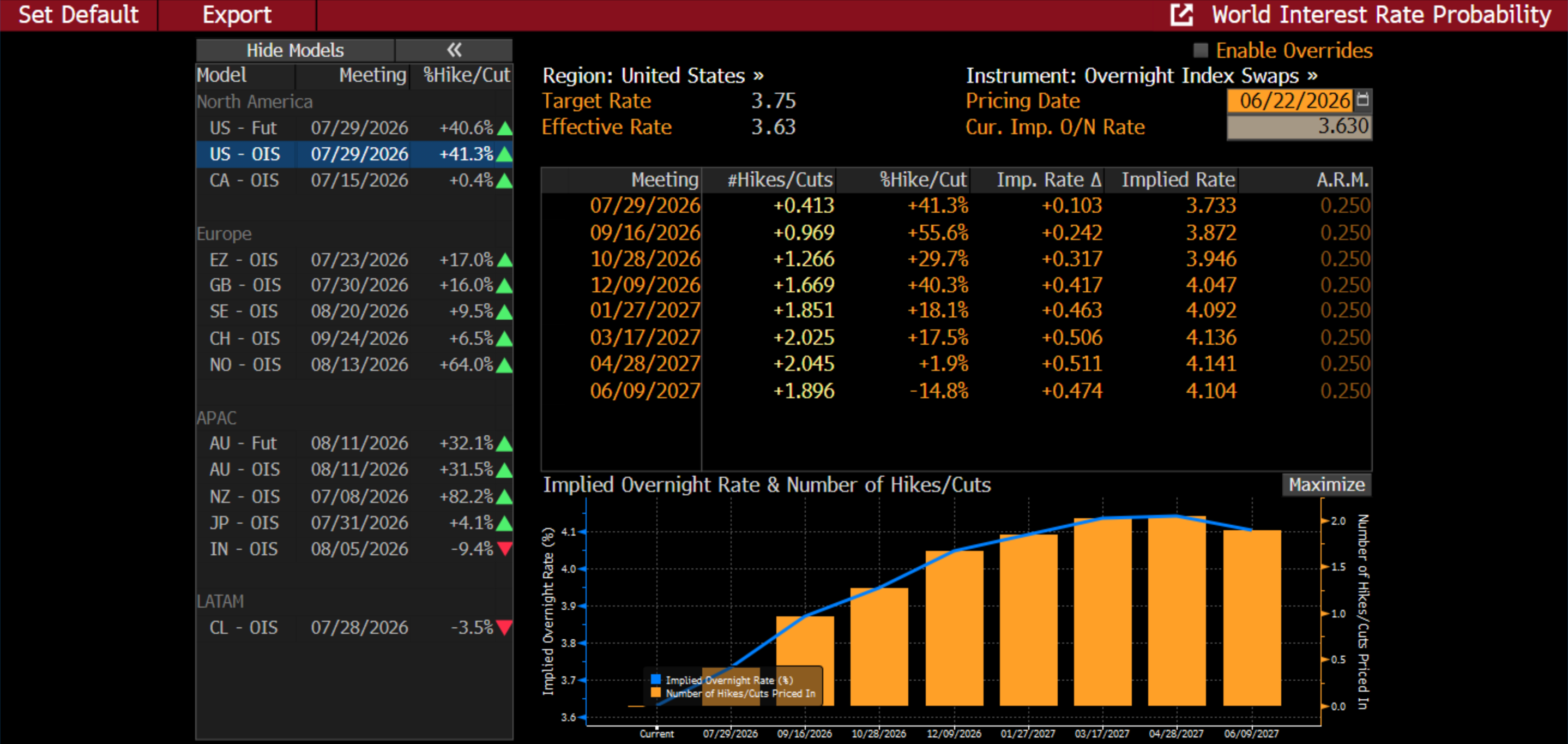

That changed on Wednesday, at least temporarily, when Kevin Warsh delivered his first FOMC meeting as Chair. Rates were left unchanged, as expected, but the statement and press conference made clear that this is not a Fed trying to preserve optionality around cuts. The new message was inflation first, patience second. The shortened statement was blunt: “The Committee will deliver price stability.” Updated projections showed headline and core PCE revised materially higher, with nine officials now seeing at least one hike this year and six pencilling in 50bps or more.

Markets reacted accordingly. Equities sold off through the statement, press conference and into the close, while rates repriced sharply. OIS now prices a 25bp hike by October, a remarkable shift from the pre-war environment.

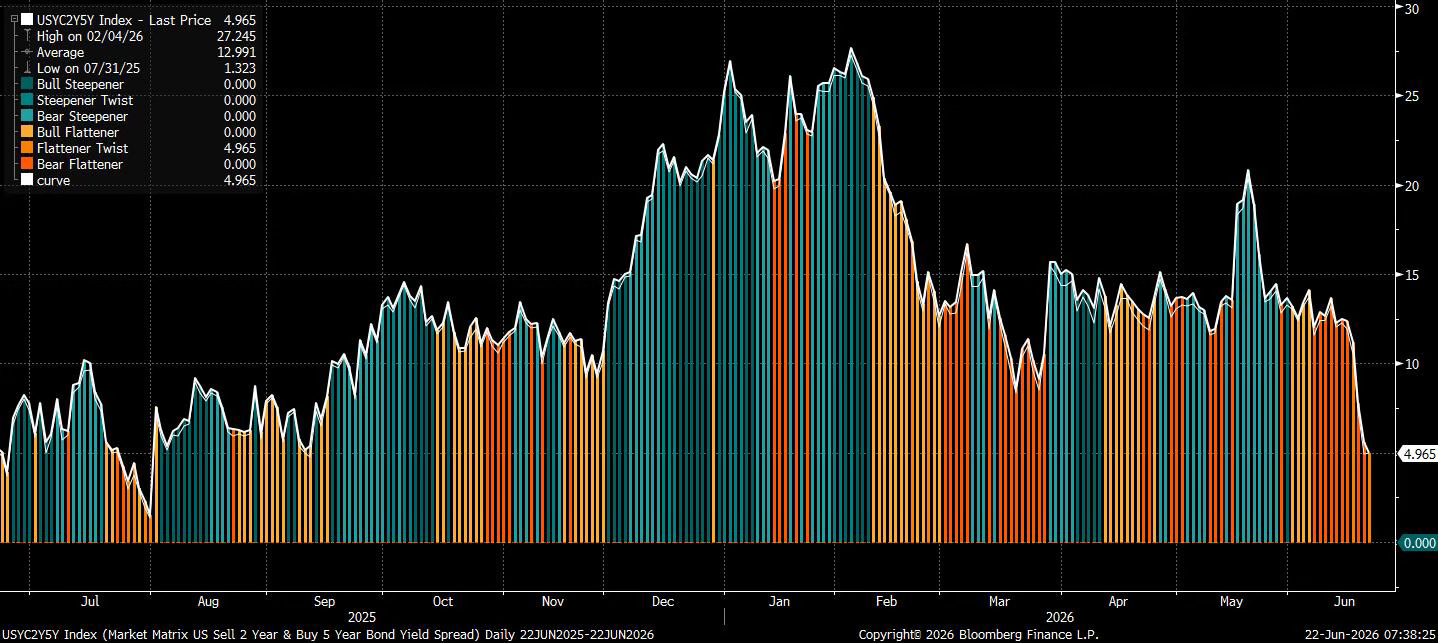

The front end bore the brunt of the move, with 2s5s close to inverting as policy expectations adjusted. The Fed reaction function has changed, and the market is still adjusting to what that means.

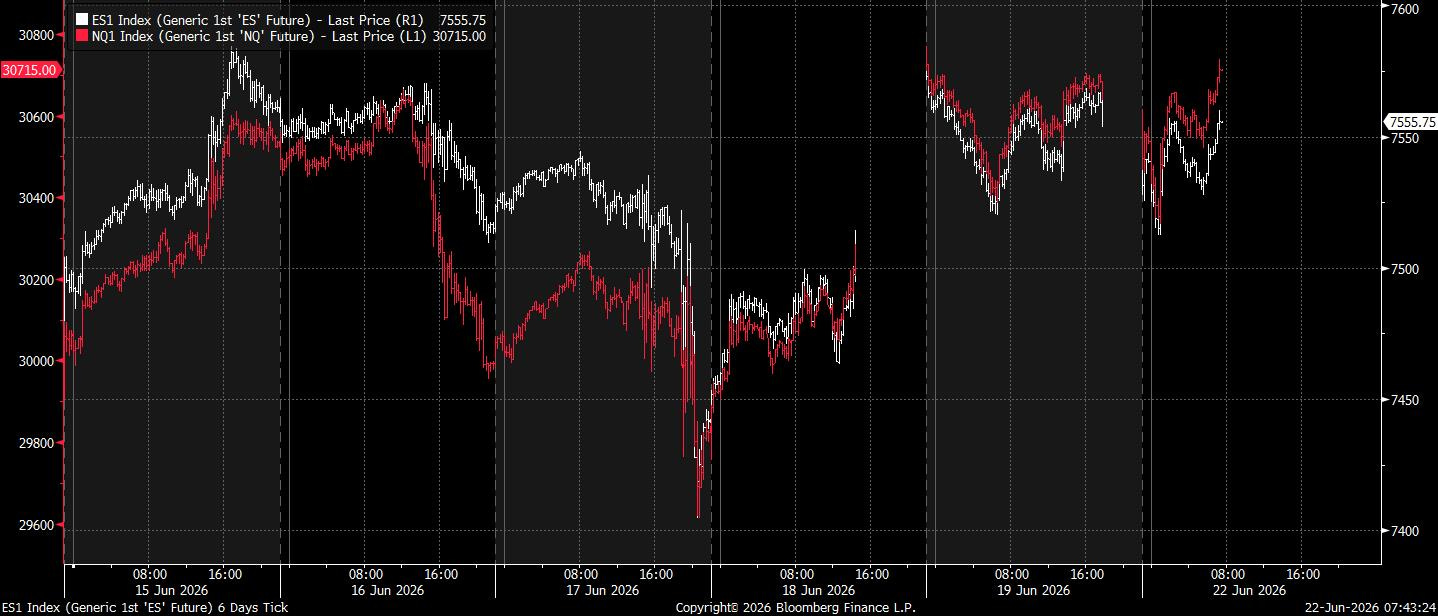

Yet equities again proved reluctant to stay down. Thursday’s rebound was led by semiconductors. Macro markets are trading a genuinely tighter policy path, while equity markets are still willing to look through it as long as AI-linked earnings and capital spending remain intact.

The dollar was the clearest macro winner. Even as oil prices fell toward the end of the week, the hawkish Fed repricing kept the greenback well bid and raised the question of whether the USD can finally break out of the structural weakness that defined the last 18 months.

USD/JPY moved back above the prior intervention zone, trading beyond 161, which keeps Japanese officials firmly in focus.

Markets have entered a more complicated phase. The geopolitical tail risk has eased, the AI trade remains alive, and dip buyers are still active. But the Fed has become an active constraint. From here, the market needs either continued AI earnings strength, a durable fall in oil, or a clean disinflation impulse to offset a policy path that is now moving in the wrong direction for risk assets. For now, equities are still climbing, but the macro floor underneath them has become noticeably less forgiving.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“AI Funders and Winners”

“The Hawkish Hold Needs a Witness”

“Sentiment Can Adjust Immediately, Oil Barrels Can’t”

AI Funders and Winners

The dominant theme over the past week has been a broadening of the AI trade away from the largest mega-cap names. Mag 7 and hyperscaler names are both nearly flat for the year.

For most of the past two years, exposure to AI was simple. Own the largest US technology platforms and own the semiconductor leaders. The trade is now starting to separate. Memory, semiconductors, custom chips, Asian supply chains, and data-centre infrastructure are among the leading beneficiaries of the AI capex cycle. The hyperscalers themselves are beginning to look more like the funding vehicle for the cycle than an upside expression of it.