The US 30-year yield crossing 5% has become the bond market’s version of a smoke alarm. Every concern around inflation, oil, fiscal sustainability, Fed credibility, and duration demand gets compressed into one round number, and every move through it invites the same question: is this the start of something bigger, or simply the level where buyers return?

We think the answer is more nuanced than much of the commentary suggests. The move higher in US long-end yields is not best understood as a purely domestic Treasury story. It is part of a broader global repricing of long-duration risk, with the US dragged into a move that has been far more aggressive elsewhere.

In the US, 5% 30-year yields still attracts buyers. In the UK, 30-year gilt yields at the highest level since 1998 are forcing investors to reprice political risk and diminishing fiscal credibility.

Rather than treating higher US yields as the cleanest expression of bearish duration, we think the better setup is relative, and outline a new spread trade below on the premise that US long bonds may remain volatile, but UK gilts look more vulnerable.

The Global Tail Wagging the US Dog

Let’s start our case by looking at the front-end policy logic, where recent meetings from the Bank of England (BoE) and the European Central Bank (ECB), presented a much easier stance to understand to see than for the Fed. The BoE kept the bank rate at 3.75% at the end of April, but its scenarios explicitly contemplated a “forceful tightening” if the energy shock produced material second-round inflation, and markets still price roughly two hikes this year.

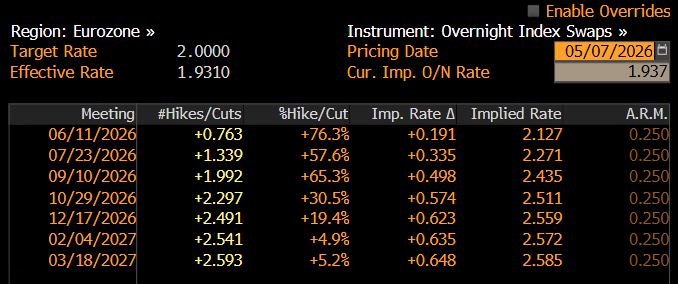

The ECB also stood pat, but openly debated a hike at its April meeting and has since signalled that the chance of a move has risen, with markets now expecting the first increase by July and more coming by the end of the year. If the UK and the euro area are repricing for actual tightening, Treasuries were never going to ignore the same global energy shock altogether.