The Labour Market's Two-Way Test

A weekly look at what matters and how to trade it. (June 1st)

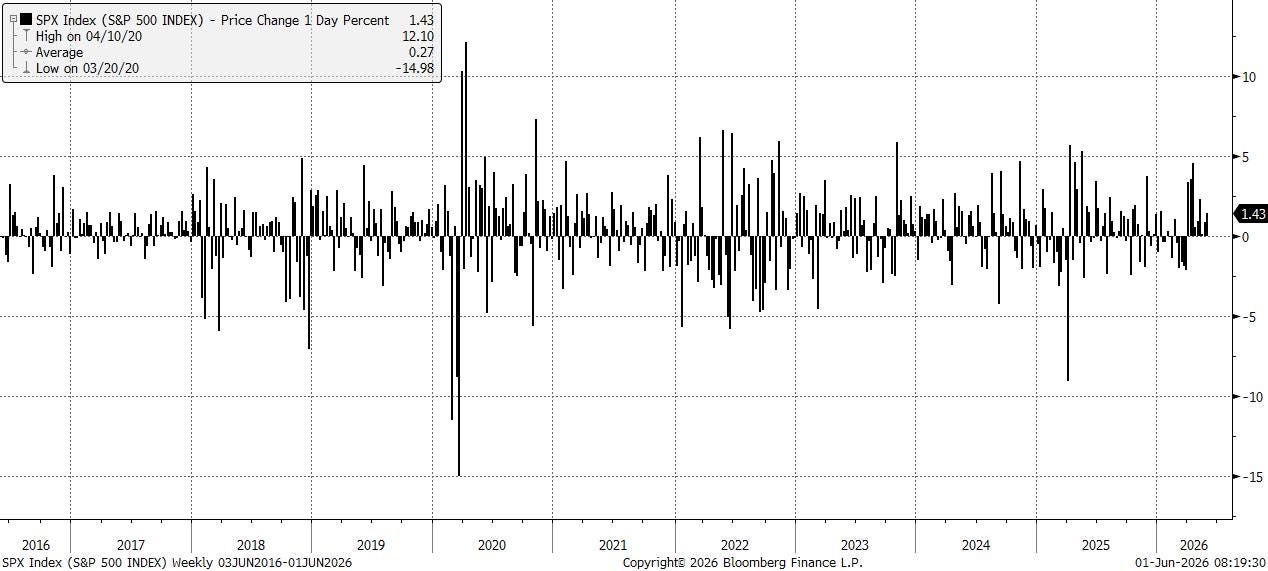

US equities advanced for a ninth consecutive week, matching one of the longest winning streaks of the past four decades, as even modest pullbacks continued to find buyers. Optimism around an eventual US-Iran deal, easing oil prices, another burst of AI enthusiasm, and the first tentative sign of disinflation in the Fed’s preferred PCE measure all acted as tailwinds. The combination was enough to push the S&P 500 higher every day of the week, even as the pace of gains slowed from the more violent rebound off the March lows.

The market’s leadership remained heavily concentrated in AI beneficiaries. Micron crossed the $1 trillion market-cap threshold, while AMD and Broadcom advanced again. Dell was the standout, surging after lifting its annual sales outlook on the back of AI server demand as RetroTech continues its omeback.

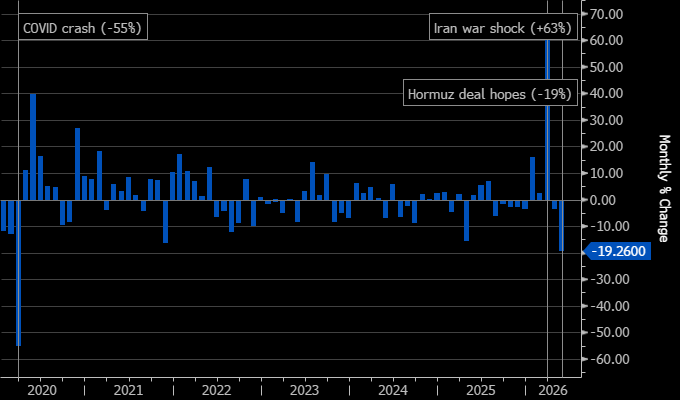

Oil provided the other major support. Crude fell around 7% as hopes for a 60-day US-Iran truce extension gathered momentum, easing some of the inflation anxiety that had dominated the previous month. The energy sector lagged as a result. Lower oil gives equities breathing room, especially when the Fed is still more worried about inflation than growth. The problem is that the peace process remains incomplete. Mixed signals from both sides mean markets are pricing progress, not resolution.

The macro backdrop improved, but not enough to change the Fed story yet. Core PCE came in slightly softer than expected, giving equities a clean disinflation impulse for the first time in a while. Fed speakers remained firmly cautious, with several officials still openly discussing the possibility of hikes if inflation fails to cool.

Rates reflected that tension. Treasury yields moved lower on Iran optimism and softer inflation, but the curve itself was stable and demand at supply remained healthy. At the same time, options flow still showed traders paying for upside yield risk, with 10-year structures targeting levels above 5%. In FX, the dollar ended broadly flat as month-end support offset the risk-on selloff following positive Iran headlines. Spot markets still look ready to fade dollar strength on peace news, but options continue to price a more durable USD premium, especially in USD/JPY.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“Earnings Season Takeaways”

“Japan’s $73bn Speed Bump”

“NFP Preview”

Earnings Season Takeaways

With the bulk of corporates now having reported for Q1, there’s enough data to get clean takeaways from a helicopter view rather than just at a company-specific level.