The S&P 500 extended its winning streak to six consecutive weeks, continuing to grind to fresh record highs as resilient earnings, stable macro data, and cautious optimism around the Middle East supported risk appetite. While the geopolitical backdrop remained unresolved, the market increasingly traded as though the probability of a broader escalation had declined, allowing investors to refocus on the themes that have driven the rally for much of the past year.

Technology once again carried. The semiconductor complex remained the clearest expression of the market’s conviction around the durability of the AI capex cycle, with Advanced Micro Devices (AMD US) delivering the standout report of the week. The company’s stronger-than-expected sales outlook reinforced the view that hyperscaler and enterprise spending on AI infrastructure remains robust, even after months of investor concern around saturation and monetisation. Importantly, the strength was not confined to GPUs. AMD highlighted renewed demand for CPUs tied to AI workloads, a reminder that the buildout story is broader than a single chip category. The positive read-through extended across the ecosystem. Akamai Technologies (AKAM US) rallied after securing a major agreement with Anthropic, underscoring the degree to which AI demand is beginning to pull through into adjacent infrastructure providers.

Beneath the surface, however, the rally retained a distinctly geopolitical undertone. The fragile ceasefire between the US and Iran held together for another week, helping suppress the tail-risk premium that had dominated markets earlier in the quarter. Yet the absence of meaningful progress on reopening the Strait of Hormuz continues to leave a structural risk embedded within energy markets. Traders have become more comfortable fading escalation headlines, but not fully comfortable removing the risk premium altogether.

On the macro side, the latest payrolls report effectively reinforced the market’s baseline assumption: the Federal Reserve remains firmly on hold. The data was neither weak enough to force easing discussions nor hot enough to revive serious tightening fears. Wage growth continued to moderate, revisions softened the headline strength, and the broader labour-market picture still points toward gradual cooling rather than collapse. The Fed is trapped in wait-and-see mode, with officials increasingly acknowledging inflation risks while simultaneously resisting the idea that hikes are imminent.

Rates and FX markets reflected that equilibrium. Treasury curves finished little changed as oil price fluctuations continued to dominate day-to-day moves more than domestic data releases. In currencies, the dollar ended broadly flat, though USD/JPY remained the key source of volatility amid growing suspicion of renewed Japanese intervention activity. More broadly, FX markets appear stuck in a holding pattern, unwilling to fully re-engage structural dollar bearishness until the geopolitical backdrop becomes cleaner.

The bigger picture remains one of a market climbing despite, rather than because of, the macro environment. Earnings are holding up, AI spending remains relentless, and positioning dynamics continue to provide support on pullbacks. But underneath the surface, the rally is increasingly reliant on a narrow set of conditions remaining intact simultaneously: contained geopolitical risk, stable growth, moderating inflation, and continued faith in the AI investment cycle. For now, markets are willing to extend that benefit of the doubt.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“Party Like It’s 1999”

“Energy Keeps CPI Warm (US Inflation Preview)”

“Global Rates Rundown”

Party Like It’s 1999

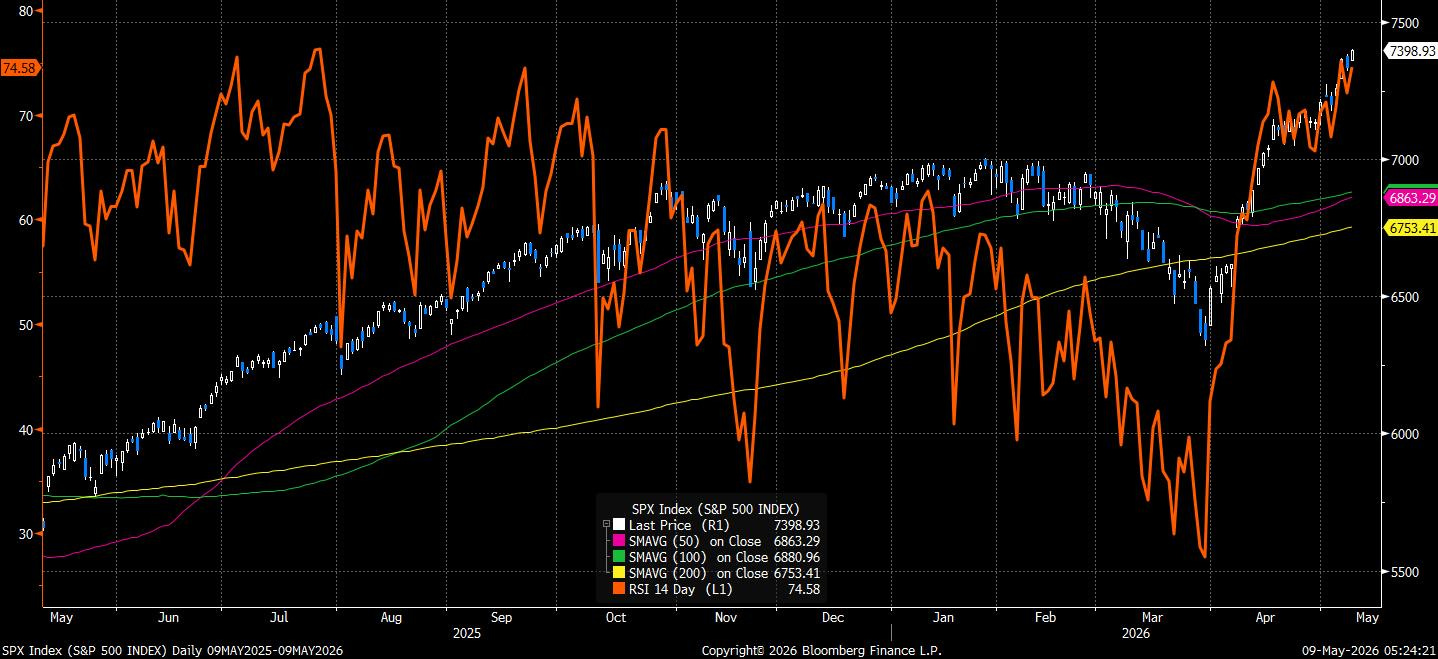

Equities have reached the part of the move where momentum is both the argument and the risk. Following one of the strongest short-term rallies in modern market history, the S&P 500 has broken into fresh all-time highs, with its 14-day RSI now sitting around 72. In isolation, that normally argues for caution. Markets that move this far, this fast, tend to digest the move. Two-week forward returns after similar momentum bursts have historically been weaker, as some degree of mean reversion usually follows the initial chase.

But overbought is not the same thing as bearish. It is often the condition of a market with genuine force behind it. The ability to get this extended, particularly after a “blue sky” breakout into all-time highs, is also evidence that the underlying trend has become durable.