The Shadow Anchorman

Powell's new role at the Fed is more important than he's indicating.

Back in March, Jerome Powell made clear that he intended to remain at the central bank until the Justice Department’s investigation into him and the Fed had run its course. Last night’s confirmation at the FOMC meeting, then, was not exactly a surprise. But it did add texture to what his post-chairmanship role is likely to look like.

The public line was deliberately dull. Powell said he planned to keep a low profile as Governor, a sort of phrase central bankers use when they would like everyone to stop listening quite so carefully. We are less interested in the formal wording than in the reality behind it.

Powell may no longer be the frontman, but that does not mean he exits the stage. In a Fed facing political pressure, legal scrutiny, fiscal dominance, and a policy regime increasingly reminiscent of earlier episodes of Treasury-Fed tension, a former chair sitting on the Board is a shadow power centre.

So, while the president may prefer Jerome “Too Late” Powell, we think the more useful title for his next act is Jerome Powell, The Shadow Anchorman.

Learnings From the Past

The last time a Fed chair stayed on the board was in 1948, when Marriner Eccles served as a policymaker until 1951.

In formal terms, nothing required his departure. In practical terms, his continued presence became highly consequential given the macro regime the US was navigating, which we feel signals what Powell could be steering towards in 2026.

During World War II, the Fed had committed to capping Treasury yields to ensure cheap and stable government financing. By the late 1940s, however, rising inflation and a shifting economic backdrop made this arrangement increasingly untenable. Eccles had already begun to pivot toward a more orthodox central banking stance by the time his term was up.

His decision to stay on as a Governor was therefore strategic. Eccles became one of the leading internal voices pushing for a reassertion of Federal Reserve independence from the Treasury. This culminated in the Treasury–Federal Reserve Accord of 1951, which restored the Fed’s ability to conduct monetary policy without direct fiscal oversight.

There was also a reputational and legacy dimension. Eccles had been instrumental in shaping the modern Federal Reserve framework during the 1930s and 1940s, including its expanded role in macroeconomic stabilisation. Remaining at the Fed through this transition allowed him to complete that project.

In that sense, his tenure beyond the Chairmanship mirrors, in part, what we think Powell is guiding for, namely that influential policymakers stay on in a reduced formal capacity to guide the system through uncertain periods.

Uncertainty in 2026

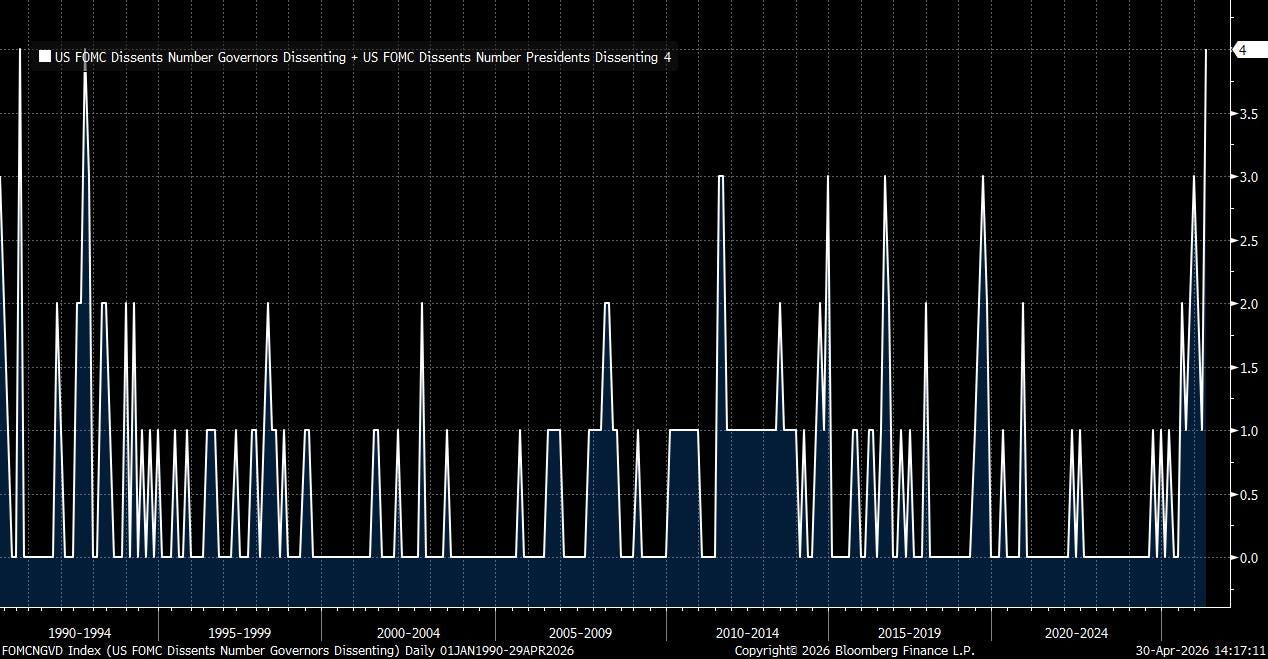

What is the uncertainty that Powell could be staying on to help guide? Last night showed further signs of dissension in the ranks, with an 8-4 voting split, marking the highest level of dissent since 1992.

Miran voted for a rate cut (no surprise there), while three others opposed the statement’s “easing bias” that hints at future reductions.

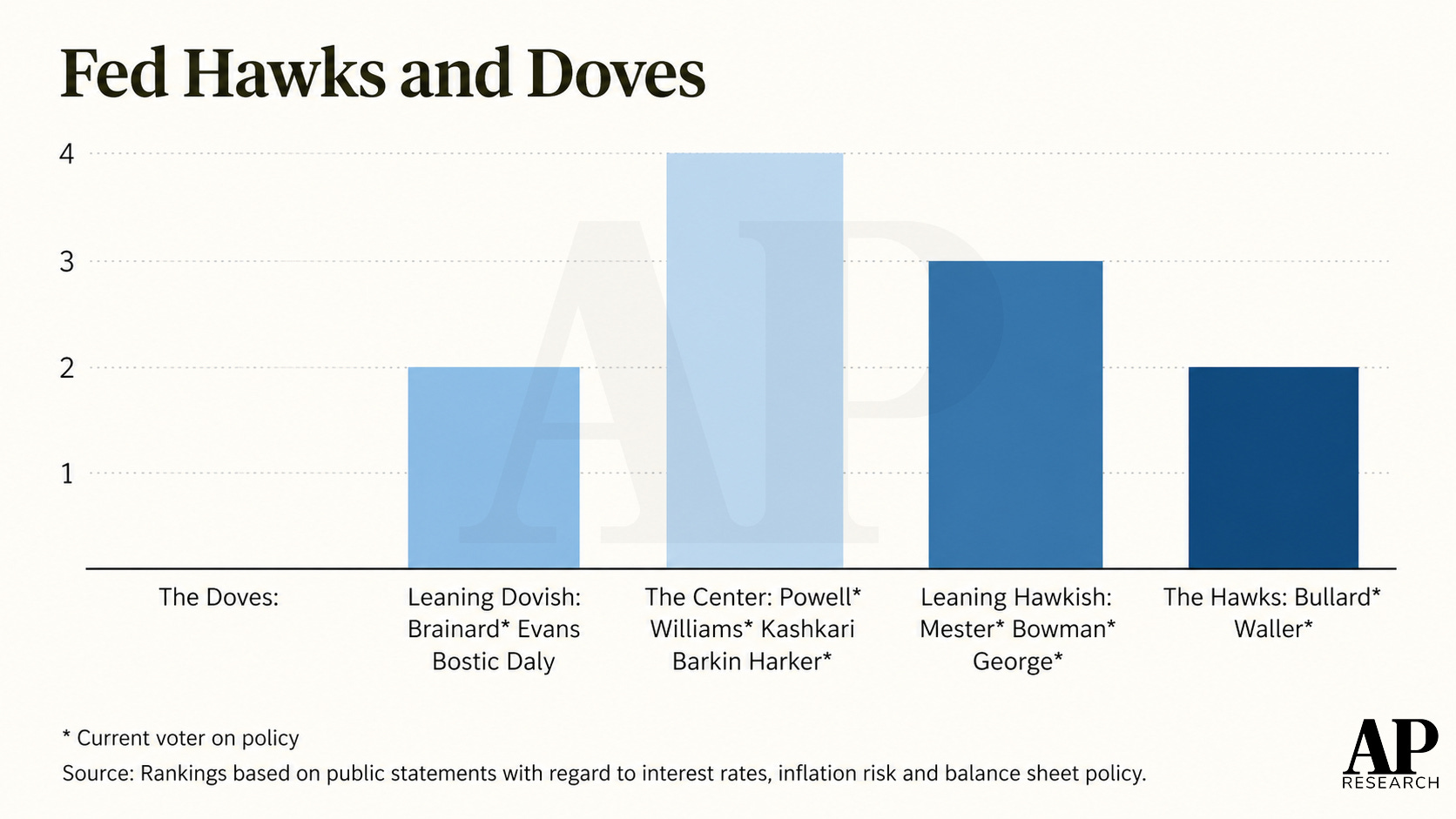

If he left now, Powell would be handing the reins over to Warsh, who we’d argue is leaning dovish, setting the scene for higher friction in policy setting right at the time where inflation remains elevated and a “low hire, low fire” employment setting.

Although he’s a one-man army, Powell firmly sits in the centre of the hawk-dove scale.

We believe this centrist positioning becomes more valuable, not less, once he steps down as Chair. Without the formal authority of the Chairmanship, influence shifts toward persuasion, credibility, and coalition-building within the FOMC.

A policymaker anchored in the middle of the distribution is structurally better placed to bridge internal divides, particularly in the likely future regime where disagreement is likely to widen. Powell, in this capacity, can act as a reference point for both sides of the spectrum, shaping outcomes at the margin by nudging the committee toward compromise rather than amplifying factional splits.