Threading The Needle At The BoE

Takeaways, views and trade ideas following the Bank of England (BoE) meeting.

Yesterday saw the latest Bank of England meeting from the HQ at Threadneedle Street, and although no one in the market was expecting a rate cut, we were looking for another indication that signals rate cuts are becoming more and more imminent.

To that end, we wanted to review the meeting, run over our thoughts and present a few trade ideas for those that are happy to take on UK exposure.

Before we get into the article, you can become a premium subscriber with us for just £10 a month. This provides you full access to our weekly articles without a paywall, including our flagship Monday trade ideas and access to what we are buying and selling in our Global Asset Portfolio.

Key points from the BoE

If you want to read the full minutes, you can do so here. In terms of a summary, see below:

Current Economic Conditions: The committee noted that global GDP growth was stable, with advanced economies like the US and Euro area showing moderate growth rates of 0.3% in Q1 2024. Emerging markets, particularly China and India, also exhibited healthy growth.

“Bank staff now expected UK GDP growth of 0.5% in 2024 Q2 as a whole, stronger than the 0.2% rate that had been incorporated in the May Report. In light of this, the Committee discussed its view of the underlying trend in growth. The latest upside news to measured GDP over the first half of this year should be set against the surprisingly weak output data that had been observed during the second half of 2023.”

Inflation Trends: Headline CPI inflation in the UK continued to fall, driven by base effects and lower goods prices. This was reflected in the 2% CPI YoY reading earlier this week.

However, core inflation and wage growth remained elevated, indicating persistent inflationary pressures. The MPC emphasized the need for restrictive monetary policy to ensure inflation returns to the 2% target sustainably.

“Twelve-month CPI inflation had fallen to 2.0% in May from 3.2% in March. The decline in headline CPI inflation had been accounted for largely by base effects across both goods and services. The May outturn had been close to the expectation made at the time of the May Report, although downside news from core goods price inflation had somewhat offset upside news from services price inflation.”

Labour Market: The labour market showed signs of loosening, with indicators such as the vacancies-to-unemployment ratio suggesting reduced tightness. Nonetheless, wage pressures remained significant, contributing to domestic inflation.

International Developments: The committee discussed the global economic landscape, noting that inflation remained above targets in major economies. The US and Euro area continued to experience elevated services inflation, with US headline CPI inflation at 3.3% and Euro area HICP inflation at 2.6% in May.

Monetary Policy Stance: The MPC reiterated that monetary policy needs to remain restrictive to mitigate the risk of inflation becoming entrenched above the target. They are prepared to adjust the policy as necessary based on future economic data.

“Monetary policy will need to remain restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term in line with the MPC’s remit. The Committee has judged since last autumn that monetary policy needs to be restrictive for an extended period of time until the risk of inflation becoming embedded above the 2% target dissipates.”

Our thoughts

Over the past couple of months, we’ve been saying that at least two cuts are coming from the UK this year. As of close on Wednesday, the market had 41.5bps worth of cuts priced in. August specifically had 8bps of cuts, with Sept at 10bps.

Following the meeting, rate cut pricing has picked up, as shown below:

Bets on rate cuts in August have edged up to 15bps, close to a coin toss, while the cumulative figure by September have gone to 23bps.

We think this pricing has room to increase further based on a few factors.

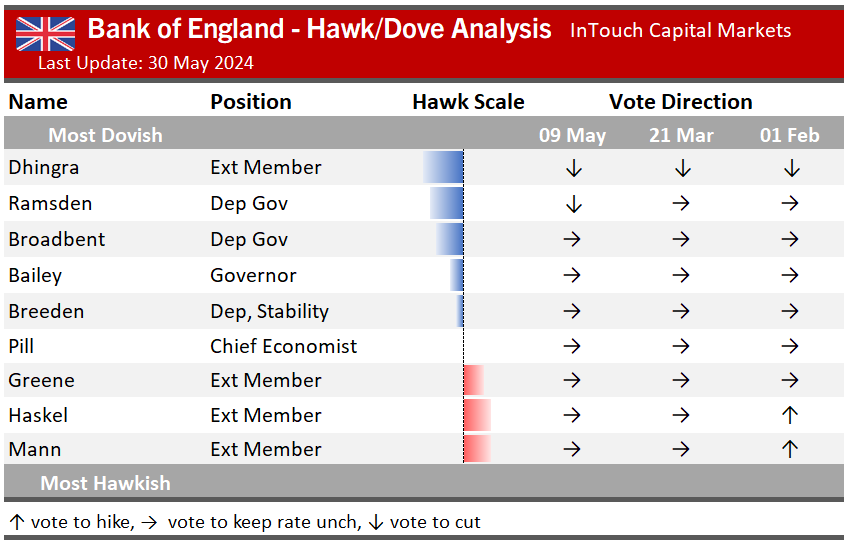

Doves vs Hawks

Firstly, the 7-2 vote was accompanied by the ‘finely balanced’ comment. To us, this shows that there were others who were a lot more on the fence this time around that could be persuaded to lean to a cut in August/Sept.

Swati Dhingra and Dave Ramsden both kept their call for a cut, which didn’t surprise us. When you consider the dove/hawk scale right now, it’s not hard to see that the votes are there. Below we highlight this with a handy summary from the team at InTouch Capital Markets:

We think that Broadbent, Bailey and Breeden could swing to voting for a cut, which would allow a 5-4 split. In reality, if Bailey was to vote for a cut, we feel this would be supported by more of a 6-3 move, likely supported by Pill.

Labour market

Even though wage pressures are still there, we also feel the labour market is starting to flash warning signs that the BoE won’t want to ignore. They commented that “the restrictive stance of monetary policy is weighing on activity in the real economy, is leading to a looser labour market.”

The unemployment rate is ticking higher, and is now at 12 month highs at 4.4%.

Based on these, and other influences, we feel that we’ll definitely have two cuts this year, with a leaning towards three. The bank want to see low inflation sustained, and so even with no meeting in July giving more ample time for the August meeting, we feel the first cut comes in September.