Tied To The Fed?

European equities could be the biggest loser of higher U.S. rates.

2025 is set to be another interesting chapter in the U.S. interest rate cycle. At the FOMC meeting in December, Jerome Powell introduced markets to a “new phase,” with market expectations now at just one or two cuts across the year. Opinions are mixed, with a handful of voices, including ourselves, expecting the Fed to out-dove current pricing. The topic of where the neutral rate is will also be a big conversation this year.

However, today’s article looks at how higher U.S. rates will have a significant impact, not locally but in Europe.

Higher Impacts

The initial reactions to the Dec. 18th Fed meeting were taken negatively by equity markets, as the S&P 500 fell 300bps and the tech-heavy Nasdaq fell 100bps further. Over in Europe, there was no escape. The SXXP also fell 300bps.

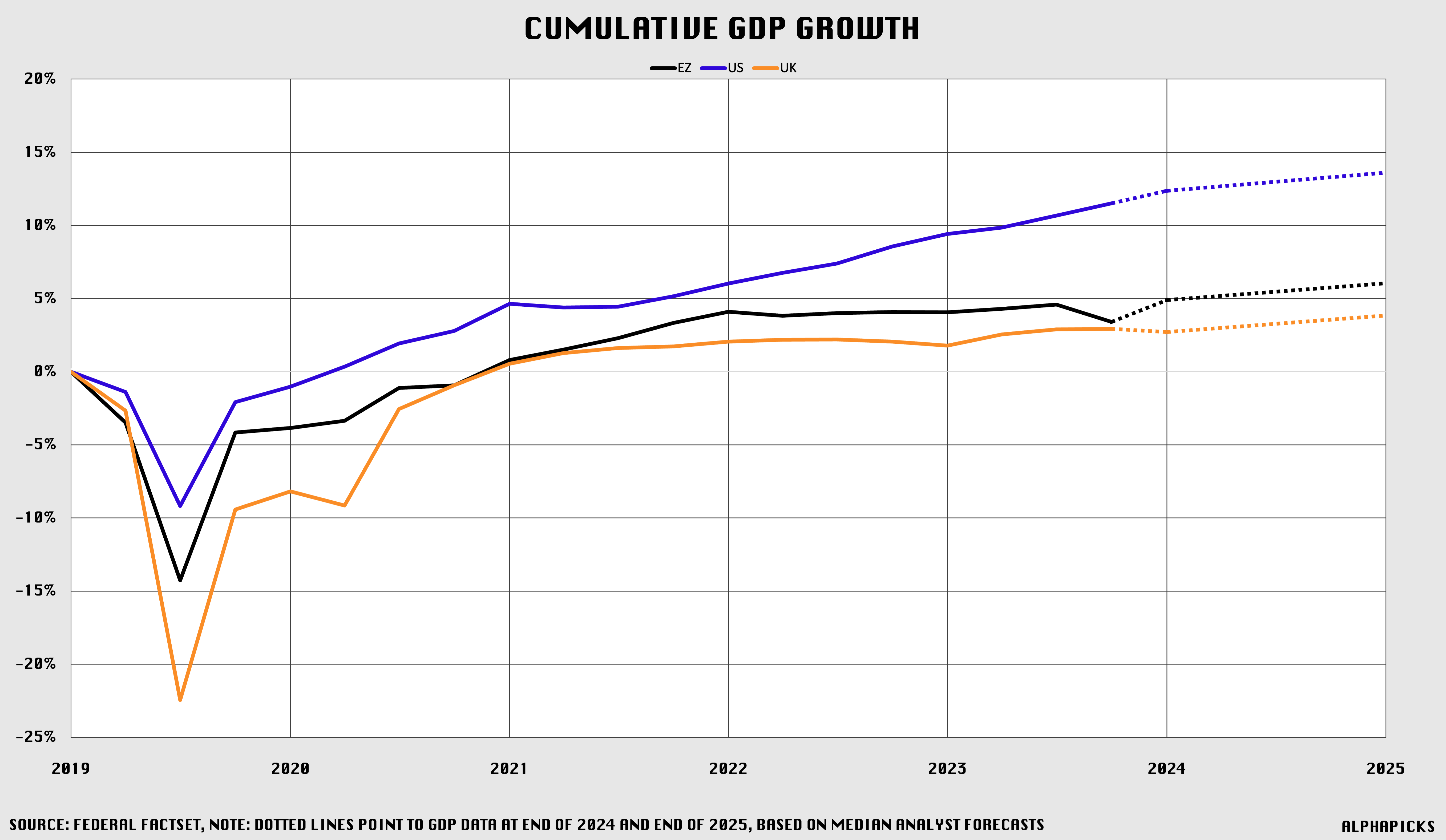

Taking a slightly wider look back, since the ECB first cut rates in June, the European equity benchmark is 270bps lower, while the U.S. indices are both over 1,000bps higher. While there have been several factors serving as a strong headwind for Europe—diminishing 2024 returns in the process—the divergence of path expectations might weigh in again this year.

In contrast to the U.S., the gross domestic products of both the Eurozone and the United Kingdom have not returned to the growth trajectory observed prior to the pandemic. Europe is characterised by a lower concentration of tech companies, and fiscal stimulus measures implemented were comparatively less extensive. Also, China’s manufacturing expansion poses a threat to the export-led economic models of the core economies within the eurozone.

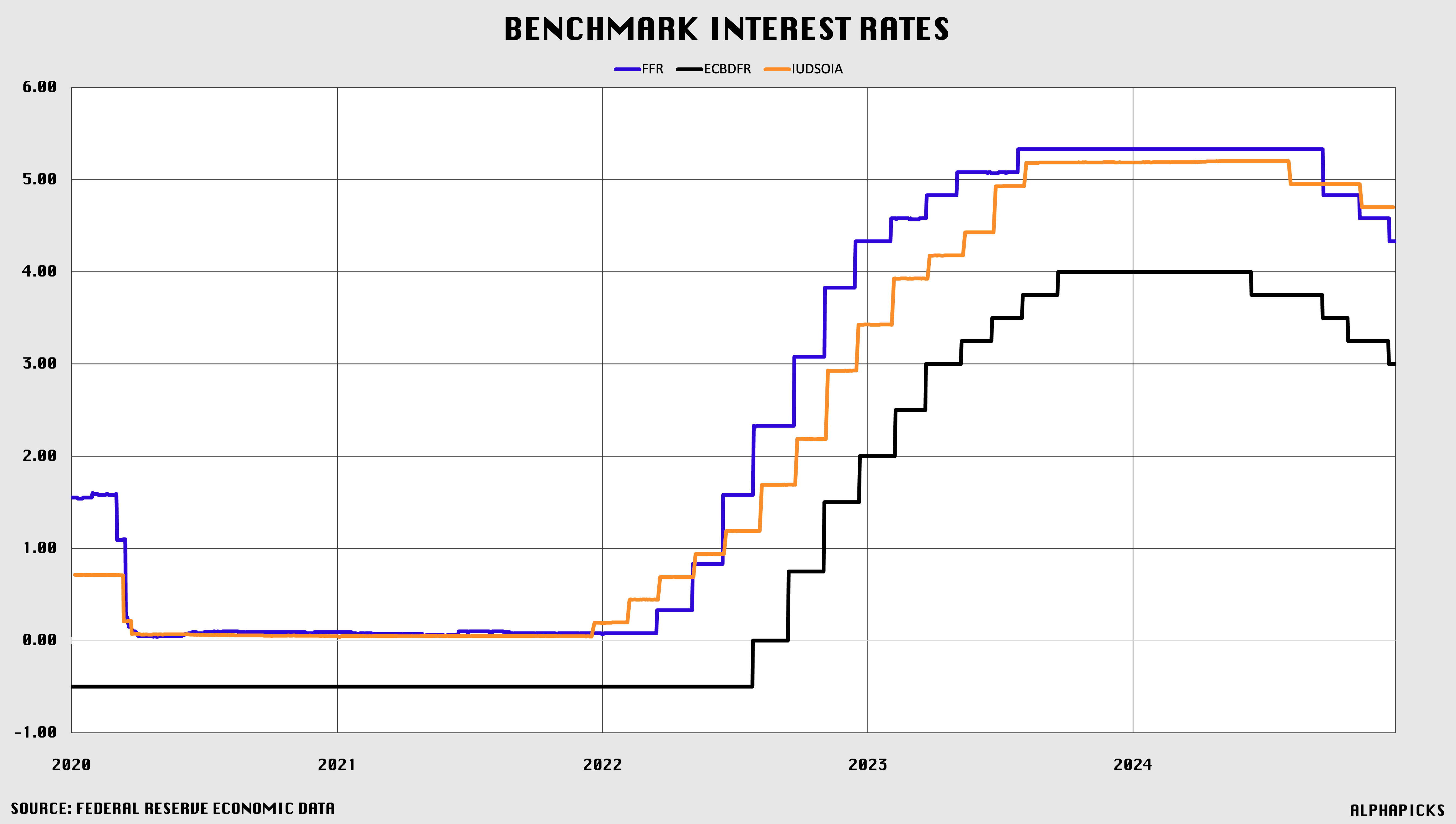

While the ECB was the first to cut rates this year and the BoE has now fallen slightly behind, they have both spent the past three years moving in lockstep with the Fed.

Sure, the eurozone has lower borrowing costs in absolute terms, with benchmark rates currently positioned at 3%, compared to a target range of 4.25% to 4.5% in the United States. But this is because the Federal Reserve officials identify the “neutral rate” in the U.S. to be approximately 2.9% (by one measure, but that’s up for debate among economists). Conversely, ECB President Christine Lagarde estimates the neutral rate for the eurozone to fall between 1.75% and 2.5%, reflective of its slower long-term growth trajectory.

Investors are anticipating that the ECB will engage in a series of interest rate cuts next year in order to reach the lower end of that range, even as the Federal Reserve and the BoE largely maintain their current policies.

In the calculations that central banks must now undertake regarding the recent resurgence in inflation versus the potential risk of an economic slowdown, the ECB should place greater emphasis on the latter consideration—and the same is true for the BoE.

Median projections indicate that the disparity in economic growth across the Atlantic is expected to continue widening in 2025. With the re-establishment of the European Union’s fiscal regulations in April, the potential resurgence of austerity measures could become a contentious issue, particularly amid ongoing political crises in Germany and France. The economic outlook for the United Kingdom remains uncertain, influenced by budgetary consolidation, possible trade tariffs, and the absence of a coherent growth-oriented strategy.

Holding The Fed’s Hand

This situation places increased importance on the actions of the BoE and ECB. Both institutions have historically resisted the notion that their decisions are primarily influenced by the Federal Reserve. However, the experiences of recent years should prompt investors to exercise caution.