Top Trade Ideas - February 3rd

The global trade war commences.

Sifting past the extensive coverage of DeepSeek from last week, there were a few other headlines that appeared from the earnings of some of the biggest names. Both Meta and Microsoft talked up their AI strategies and ambitions following their earnings, with Mark Zuckerberg stating that large capex spending and infrastructure in AI will be a strategic advantage over time.

Tesla CEO Elon Musk revealed more detailed plans about robotaxi operations alongside new model forecasts, as the stock rallied around 3% in pre-market trading despite missing earning forecasts. Apple climbed more than 3% after the market closed following earnings, with an upbeat revenue forecast and strong services growth offsetting disappointing news out of China.

The latest U.S. Federal Reserve meeting saw interest rates remain on hold as it seeks to make more progress on lowering inflation. With strong economic growth and a resilient labour market, the stock market didn’t take the chatter in a significantly negative way. We’re now in a wait-and-see stage for rates.

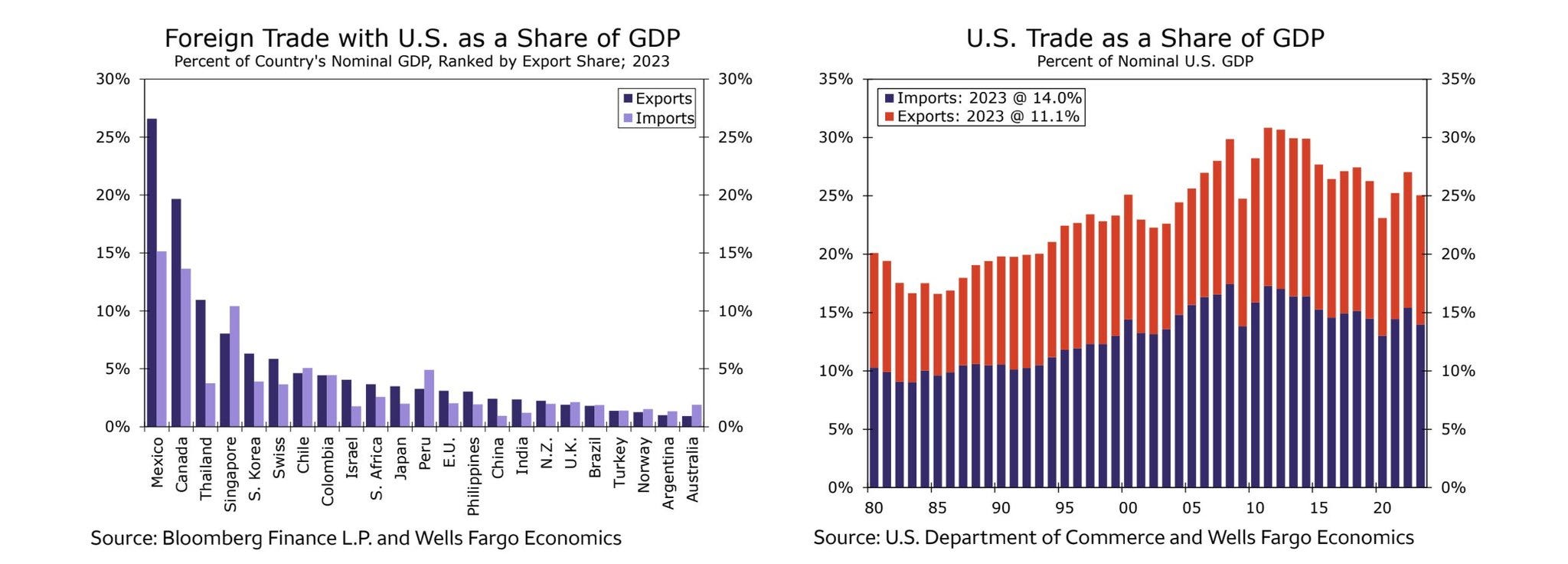

However, the big news over the weekend may play into that. Trump has imposed 25% tariffs on Canada and Mexico and 10% tariffs on China, and European levies are on the way. We are at the start of a global trade war that will bring lots of volatility across the board. Plenty of this week’s thoughts are based on this development.

If you are not yet a premium subscriber to AlphaPicks, you can manage your account here.

The Week Ahead

In Europe, the preliminary January inflation data for the eurozone will be released amid widespread expectations that the Bank of England will lower interest rates.

In Asia, attention will likely focus on a summary of opinions from the latest meeting of the Japanese central bank, along with regional purchasing managers’ surveys and inflation statistics.

In the U.S., manufacturing activity for January is set to be released on Monday, with the ISM index to follow on Wednesday. Additionally, a significant indicator of the current state of the U.S. economy will be the University of Michigan’s preliminary consumer survey for February, scheduled for Friday.

Insights into the job market will come from December’s Jolts job openings report on Tuesday and the ADP private payroll numbers for January on Wednesday. However, the main attention will be on Friday’s nonfarm payroll figures.

FX

Last week, we pivoted our USD view into a bearish one and expressed this via long trades on EUR/USD and GBP/USD.

The technical break that we saw on both pairs did press on, but the tariff-induced end-of-week USD rally saw both close lower. The Trump chatter to the EU specifically on Sunday saw the market knee-jerk early on Monday.

On EUR/USD, we learned precious little news from both the ECB and Fed, so our fundamental view on excess EUR pessimism still holds true, while the Fed pause gives little fresh reason to be getting long.

Everything considered, we stick to our guns, with EUR/USD back towards 2025 lows. A tight stop below this offers an attractive risk/reward.

TRADE IDEA - STICKING TO VIEW ON EUR/USD

Entry: 1.0225

Take Profit: 1.0530

Stop Loss: 1.0165