Top Trade Ideas - June 2nd

SPX enjoys best month since Nov '23, data deluge ahead.

US equity markets closed higher on the week, with the S&P 500 gaining 1.9%, though trade volatility capped the upside. Nvidia’s stellar earnings beat lifted sentiment midweek, offsetting the temporary uncertainty caused by a court ruling that found most of Trump’s tariffs illegal, a decision now on hold pending appeal. Tariff headlines dominated late-week trading, including Trump’s fresh accusations that China violated the recent easing agreement, raising the risk of renewed tensions.

Sectors fared well overall, with real estate and utilities leading gains, while energy lagged as risk appetite wavered due to trade concerns. The consumer sector also showed resilience as April personal income and May consumer confidence data beat expectations, suggesting the economy’s core strength endures. However, warnings from Best Buy and HP about trade war fallout and lower guidance underscored the economic fragility tied to tariff policy.

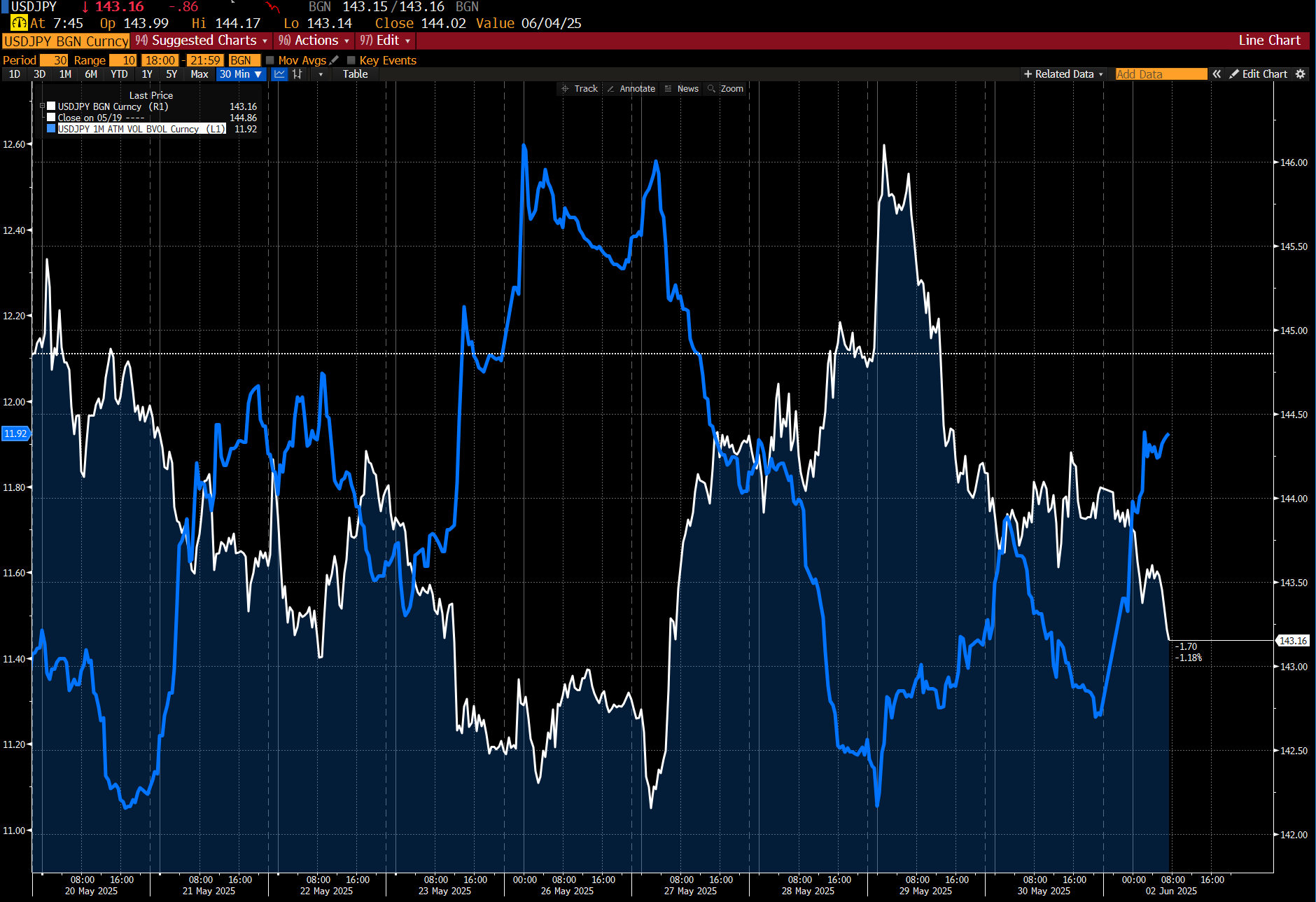

Meanwhile, the 10-year Treasury yield fell 9bps as weak global demand for long-duration bonds—catalysed by a poor JGB auction—pushed yields lower worldwide. Fed officials pushed back against rate cuts, citing still-anchored inflation expectations. The dollar ended the week modestly stronger, buoyed by yen moves and month-end flows, while USD/JPY volatility remained the main driver of FX price action.

The Week Ahead

The focus this week is squarely on US jobs data for May, due Friday, which will be critical for gauging how tariff headwinds are filtering into the labour market and shaping expectations for Federal Reserve policy. Earlier in the week, ISM manufacturing and services surveys, durable goods orders, and trade figures will provide further insight into the US growth picture. With money markets now fully pricing in two rate cuts by year-end, even modest signs of labour market weakness could push the Fed closer to easing.

The European Central Bank is expected to deliver a 25-basis-point rate cut on Thursday as eurozone inflation moderates and growth remains fragile. Flash inflation data from Germany, France, Spain and Italy earlier in the week will help calibrate the ECB’s forward guidance, which is likely to remain cautious amid ongoing trade risks. German manufacturing orders and industrial production data will round out the picture for Europe’s largest economy as it faces mounting tariff threats from Washington.

In Canada, the Bank of Canada is widely expected to leave rates unchanged on Wednesday, balancing high domestic inflation against a slowing economy. Canadian trade data and labour-market figures later in the week will add detail to the BoC’s policy outlook.

Asia will see monetary policy decisions from the Reserve Bank of India and the Bank of Korea, both of which are under pressure to ease further as global growth headwinds mount. Japan’s data calendar is busy, with Tokyo inflation, industrial production, retail sales and labor market figures all due Friday, alongside key JGB auctions midweek that will test investor appetite for ultralong bonds after recent volatility.

Meanwhile, Australia’s first-quarter GDP data on Wednesday is expected to confirm that growth remains tepid, reinforcing the Reserve Bank of Australia’s dovish turn. RBA minutes and Governor Bullock’s recent China visit underscore concerns that the country’s export-heavy economy is increasingly vulnerable to a fresh slowdown in China.

Elsewhere, central banks in Switzerland, Poland and South Africa will also set rates, while inflation figures from Sweden, Switzerland and across Southeast Asia will offer further evidence of how tariff-driven uncertainties are rippling through global prices. With trade tensions flaring anew and long-end bond yields signalling unease about deficits and inflation, policymakers face a delicate balancing act: containing price pressures while avoiding a deeper hit to already fragile growth.

FX

We may have been a little early to the party for EUR/GBP, but the move higher does appear to finally be getting some traction.

The pair managed to turn the trend channel top, which previously acted as resistance for a move, into support for EUR bulls. The ECB meeting on Thurs and top tier data out on Friday will act as the drivers behind the price action for the coming week.

From our perspective, another ECB cut is on the cards, but the market expects this. Any signal that this might be the end of the easing cycle this time around, or comments on inflation being under control, could help to kick the EUR higher.

Watch for breaks of 0.8470/75 and 0.8500 on the topside, with 0.8350 on the lowside.

TRADE IDEA - EUR/GBP PRIMED FOR HIGHER

Entry: 0.8436

Take Profit: 0.8645

Stop Loss: 0.8340

We flagged XAU/USD in our latest Money Markets post, citing the precious metal's key month ahead.

When you consider the below chart, the lower highs and lower lows mean that something has to give, with the wedge becoming ever tighter.

We can make pretty convincing arguments for both sides of the coin as to why gold might pop higher beyond $3500 or why a break lower could happen. Yet one thing is clear, a move out of this treading-water period will see people either buy the rip or look to jump on a move lower, with plenty of longs to unload.

That means that implied volatility is likely to spike over a one-month tenor, so we look to make a direction-agnostic play in the options space.

TRADE IDEA - GOLD READY TO SHIFT (EITHER WAY)

Buy a one-month XAU/USD 25D strangle costing 1.65% with strikes at $3440 and $3210