Top Trade Ideas - June 30th

Buy America is back in vogue.

US equities posted strong gains as geopolitical risks eased and trade progress resumed. A ceasefire between Israel and Iran helped stabilise global sentiment, while the White House announced further advances in tariff negotiations with China and the EU. The S&P 500 and Nasdaq 100 both closed at record highs, driven by broad strength in tech, communication services, and consumer discretionary. The Dow gained 3.8%, its best weekly performance in months.

Lower volatility and favourable gamma positioning also contributed to the rally, with Nomura suggesting dealer long gamma could provide further support on dips. Despite the strong risk-on tone, sentiment faded slightly late in the week as Trump abruptly suspended trade talks with Canada.

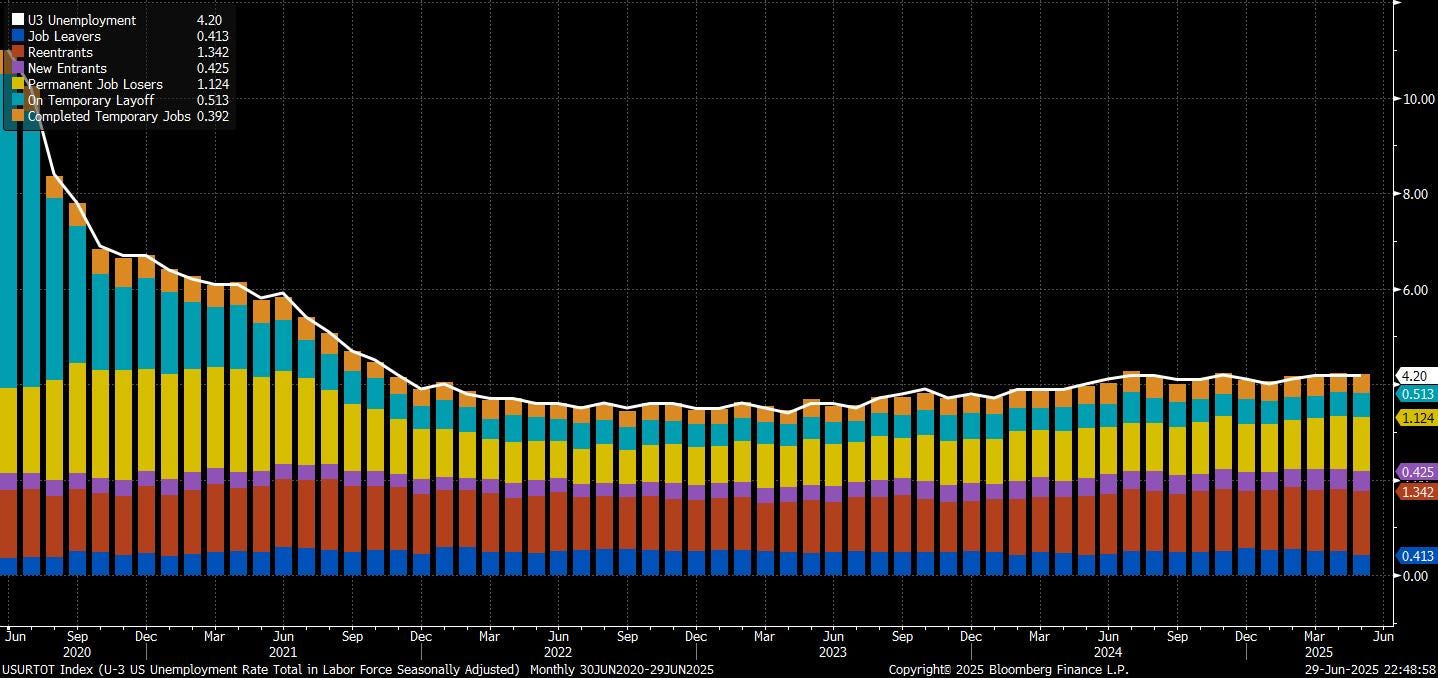

Economic data and Fed speak had little immediate market impact. Powell reiterated a cautious stance, but dovish signals from Daly and Kashkari helped boost expectations for rate cuts, with OIS markets now pricing in 64bps of easing by year-end. Treasury yields declined across the curve, with the 10-year falling 13bps as new long positions added to momentum.

The dollar weakened throughout the week amid rebalancing flows and speculation surrounding a potential change in Fed leadership, as spot and options converged once again on bearish momentum (chart below). Crude oil sold off sharply, down $10 on the week, as the Middle East ceasefire took hold, driving underperformance in the energy sector.

(To get full access to all research and notes posted, consider becoming a premium reader here.)

The Economic Week Ahead

Markets enter Q3 focused on US jobs data, with June’s payrolls report (due Thursday) expected to clarify whether the Federal Reserve could cut rates as soon as July. While core inflation has moderated, Fed officials remain cautious, citing the risk of tariff-driven price pressures. But a weak print could be the catalyst that shifts market pricing (currently centred on September) toward an earlier move, especially amid growing political pressure and speculation over Fed Chair Powell’s future.

Ahead of payrolls, the US calendar includes ISM surveys, ADP private payrolls, jobless claims, and trade data—all of which will be assessed in the context of tariff drag and political uncertainty. Treasury auctions across the curve will also test demand amid a weaker dollar and heightened fiscal concerns.

In Europe, flash eurozone CPI and labour market data will provide fresh evidence on disinflation and employment trends. Both headline and core inflation are expected to tick lower. Meanwhile, the ECB’s Sintra forum will bring together key central bankers, including Powell, Lagarde, and Ueda, for a timely discussion on how to adapt policy to structural shifts in growth and inflation. Eurozone PMIs and industrial data will fill in the macro picture, with any signs of weakness likely reinforcing the ECB’s easing bias into H2.

In the UK, the second estimate of Q1 GDP will be scrutinised for signs of underlying weakness after strong headline growth. Money markets now price a two-thirds chance of a BOE rate cut in August. Final PMI prints and retail borrowing data will round out the calendar, while a green gilt syndication will test long-end demand.

In Japan, the quarterly Tankan survey will gauge how tariffs and slowing global trade are affecting corporate sentiment and capex plans. Industrial production and household spending data are also due, while BOJ board member Takata’s speech may offer clues on the next rate hike. Inflation remains sticky, and policymakers appear in no rush to accelerate policy normalisation.

China’s June PMIs, both official and Caixin, will give a read on whether manufacturing weakness is stabilising or worsening. Soft global demand and lingering U.S. tariffs continue to weigh on sentiment. Markets will also watch for signals from Beijing on trade policy, especially after rare-earth export tensions appeared to ease.

In Australia, May retail sales and household spending data will help determine whether the Reserve Bank of Australia moves forward with another rate cut in July. Weak consumption alongside disinflation trends has put the RBA back in easing mode.

With markets still digesting global disinflation, resurgent geopolitical risk, and trade fragmentation, the week ahead could set the tone for the path of global monetary policy as central banks balance the impulse to cut with the discipline to wait.

Now for the ideas and commentary for cross-assets for the week ahead…

FX

Another short USD hedge:

We saw a divergence in inflation metrics for Japan and the US late last week, with Tokyo CPI coming in below expectations on Thursday, while US core PCE on Friday beat the consensus.

This helped USD/JPY to catch a bid to end the week, with the pair in an interesting position in making higher lows and lower highs over the past couple of months.

The pair is a nice way to hedge against our broader short USD position, so we look to buy spot here for a potential move higher, which would likely accelerate towards the 148.00 handle.

Entry: 144.60

Stop Loss: 143.40

Take Profit: 148.00

AUD/CHF trending lower:

Talking of inflation, Australia’s CPI print came in at 2.1%, below the 2.4% foretasted and significantly boosting the chances of another cut from the RBA coming up.

When playing for tactical Aussie weakness, we like to pair it up with being long CHF. We’ve been vocal in our views, particularly with APFX Research, about why we continue to be long Swiss and don’t see the trend finishing, even with the SNB just taking rates down to zero.

We feel the pair can test April levels just below 0.5000 within the coming month, if things play out as expected.

Entry: 0.5220

Take Profit: 0.5000

Stop Loss: 0.5295

Indices

Equity markets are powering higher, with both the S&P 500 and Nasdaq pushing to fresh all-time highs. The macro backdrop continues to favor risk assets: Middle East tensions have faded without disrupting flows, hard data in the U.S. has remained resilient, and the growing likelihood of Fed rate cuts is providing a tailwind—particularly for duration-sensitive sectors like tech and AI. In this environment, it’s unwise to fight the tape. Strong momentum, favorable macro signals, and a clear risk-on tone argue against shorting into strength. Price discovery is still unfolding, and bull markets tend to extend further than expected before topping out.