Top Trade Ideas - March 31st

It’s “Liberation Week.”

President Donald Trump has set the stage for a high-stakes showdown on April 2, when his administration is expected to unveil a sweeping package of so-called reciprocal tariffs. While the president has promised a “lenient” approach, investors remain wary, with markets bracing for potential upheaval, as shown in part by the price action in the equity space on Friday:

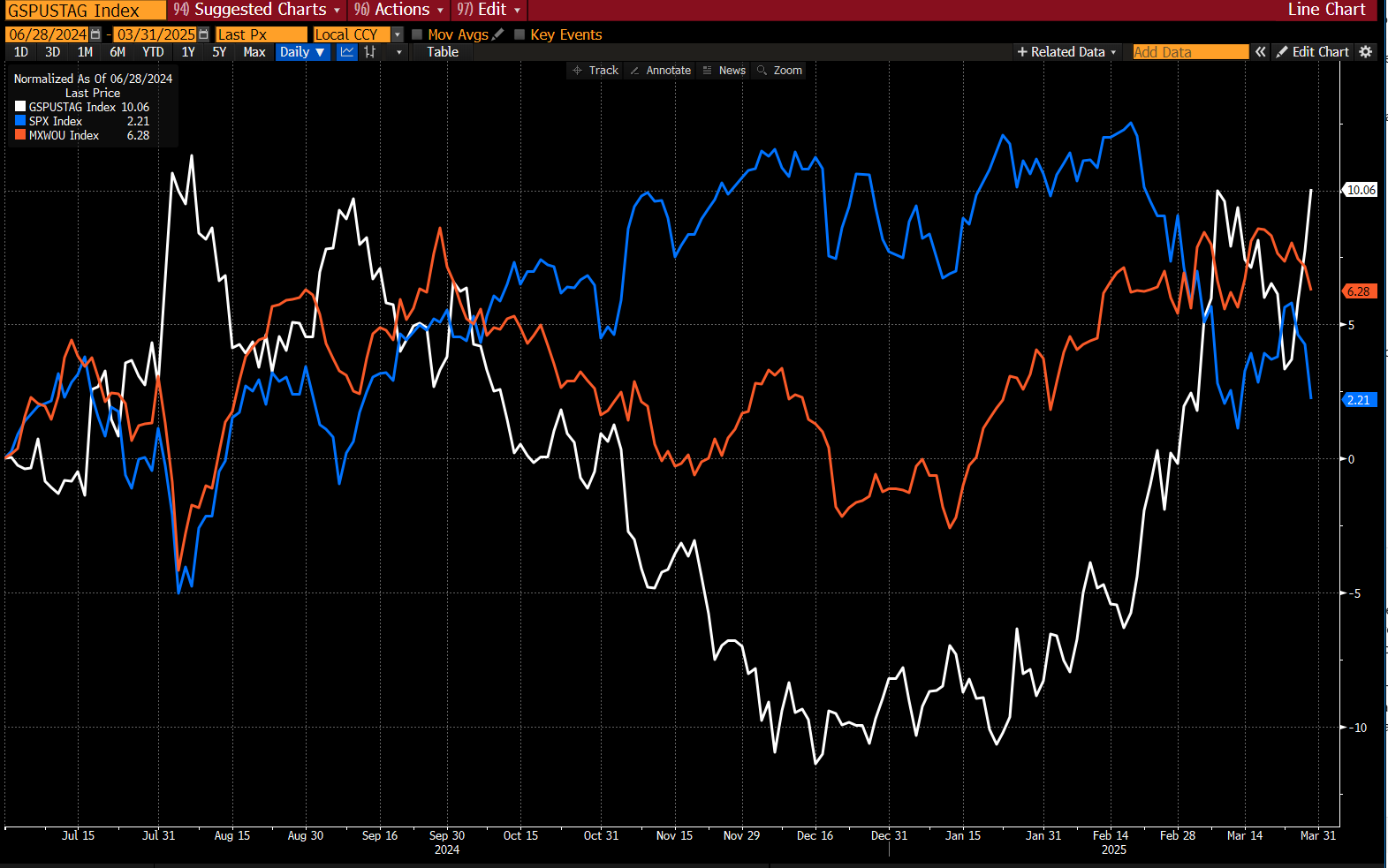

The latest round of tariffs, following last week’s auto levies, could deliver another blow to equities already reeling from trade uncertainty. Wall Street is preparing for heightened volatility as the announcement’s scope remains unclear. The stakes are high: Economists warn of possible inflationary pressures and a drag on U.S. GDP, while a Goldman Sachs index tracking stocks that benefit from stagflation has been surging (shown below in white vs SPX blue and MSCI World ex US red).

We’re at a pivotal moment. Inflation is accelerating, consumer confidence is slipping, and tariffs are a major piece of the puzzle.

Barclays strategists suggest that the market’s reaction will hinge on the details. A broad, aggressive tariff package could spell trouble for risk assets, while exemptions or a delay might trigger a relief rally. Meanwhile, the spectre of retaliation from major U.S. trading partners threatens to amplify volatility.

To take you quickly down memory lane… Long gone are the days when we used to have tweets like this one:

Before we move on to an industry breakdown and some macro trades for biases either way (benign outcome or full force), let’s run down some other events that are still on the agenda for the week ahead.

The Week Ahead

U.S. jobs data will be the highlight of the economic calendar as concerns grow about weakening economic growth due to the impact of uncertainty over tariffs.

In Europe, flash estimate eurozone inflation figures could prove key for judging the pace of future European Central Bank interest-rate cuts. In Asia, highlights include an interest-rate decision by the Reserve Bank of Australia, economic data from Japan and PMIs across the region, including from China.

Industries in the Crosshairs

United States

The auto industry remains the epicentre of tariff-related turmoil. Following last week’s 25% levies, companies like General Motors and Ford face mounting cost pressures. While Ford’s domestic production footprint offers some insulation, the broader sector remains vulnerable, with an index of automakers and suppliers down 34% since Trump took office.

Semiconductors are another key risk area. With global supply chains already under strain, potential tariffs on chips could further pressure an industry grappling with slowing data centre expansion and capital spending. Nvidia, AMD, and Intel will be in focus.

Pharmaceuticals are also under scrutiny. Tariffs could disrupt drug sourcing and distribution for giants like Pfizer, Johnson & Johnson, and Merck.

The administration’s rumoured tariffs on copper have put mining stocks on edge. Freeport-McMoRan and Southern Copper could see volatility even if the levies aren’t unveiled immediately. Meanwhile, the near-doubling of duties on Canadian softwood lumber to 27% threatens companies like Weyerhaeuser.

Beyond these sectors, industrials and consumer-facing firms with global supply chains remain at risk. Boeing, Caterpillar, Walmart, and Deere have historically been proxies for trade tensions and economic uncertainty.

Europe

The European Union is scrambling to negotiate concessions, but officials have reportedly been told that new U.S. auto tariffs are unavoidable. The Stoxx Auto & Parts Index is already down 12% from its peak this year, and German automakers face a particularly tough road ahead. Porsche and Mercedes-Benz, which export high-margin vehicles to the U.S., could see a 30% hit to 2026 operating earnings, according to Bloomberg Intelligence.

The beverage industry is also in the spotlight, with Trump threatening a 200% tariff on EU alcoholic products. Davide Campari-Milano has warned that even a 25% tariff would shave at least €50 million off earnings.

Meanwhile, European aluminium and steel producers are bracing for further trade friction. Rio Tinto, a major aluminium supplier to the U.S., is one to watch. And with pharmaceuticals among the industries targeted, Novo Nordisk—one of the region’s largest listed companies—could be exposed.

Asia

While China remains a key U.S. trade adversary, its exposure to tariffs has declined. The country’s share of U.S. goods imports has fallen nearly eight percentage points since 2017, per U.S. Census Bureau data. However, certain stocks remain at risk, such as Hong Kong-listed Techtronic Industries, which derives a significant share of revenue from the U.S.

Japanese automakers are another major flashpoint. The U.S. is a critical market for Toyota and Honda, and any escalation in trade tensions could pressure their stocks.

The semiconductor giants of Taiwan and South Korea are also in focus. Taiwan Semiconductor Manufacturing Co. (TSMC), which generates nearly 70% of its revenue from the U.S., has made massive investment commitments in American chip production. Meanwhile, South Korea’s Hyundai and Kia are watching Trump’s 25% auto tariffs with concern.

Thailand, with its heavy reliance on agricultural and transportation exports, also stands out as a potential casualty.

The Road Ahead

April 2 could set the tone for markets in the second quarter. If Trump opts for broad, aggressive tariffs, expect renewed selling pressure in equities, particularly in trade-sensitive sectors. But if the package includes significant exemptions or delays, risk assets could stage a relief rally.

Beyond the immediate reaction, investors will need to gauge the potential for retaliation from trading partners, which could trigger a prolonged period of uncertainty. With inflation already a concern, policymakers and money managers alike will be closely watching whether tariffs exacerbate price pressures.

As the deadline approaches, markets are on high alert. The outcome will shape not just global trade but the broader trajectory of inflation, economic growth, and monetary policy in the months ahead.

After a general rundown of market impacts, let’s focus on a few conviction trades for the week ahead.