All Happening on the Everything Front II

A weekly look at what matters and how to trade it. (March 9th)

The week of March 2, 2026, may be remembered as the moment the market’s favourite refrain, “Nothing Ever Happens,” finally went to die.

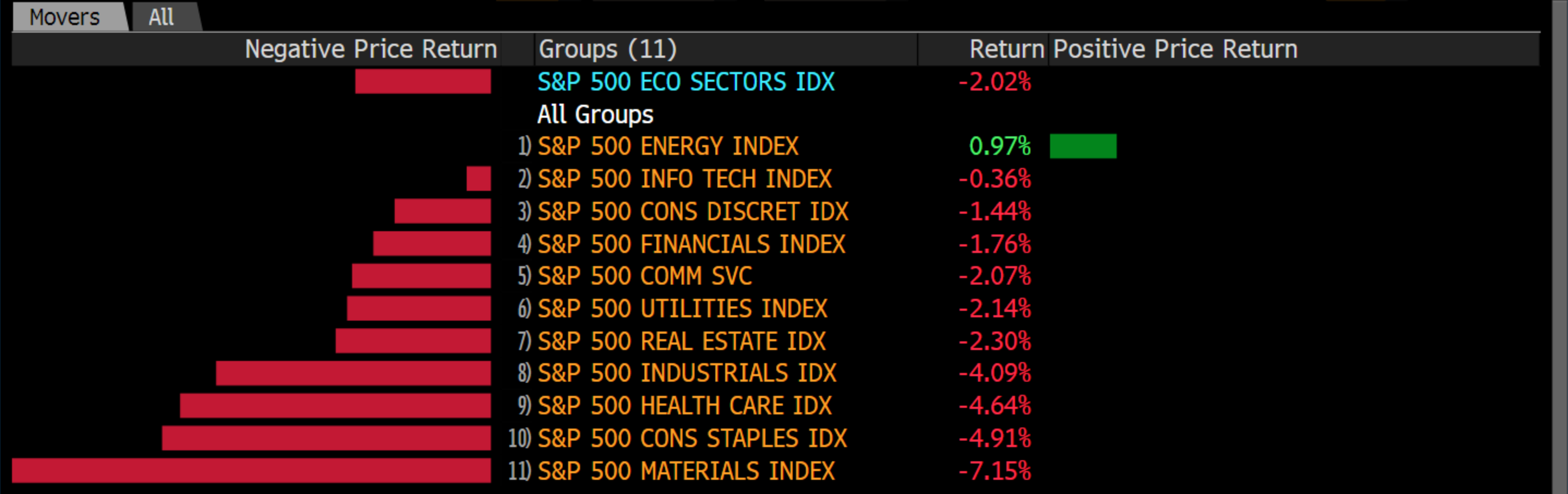

War in the Middle East dominated markets this week, sending volatility higher across asset classes and pushing investors toward a defensive posture. The VIX closed near 30, its highest level since April, while WTI crude surged above $90 per barrel for the first time since 2023 after gaining more than 30% on the week. The move reshaped sector leadership immediately. Energy and defence stocks benefited from the spike in oil prices. Still, most other parts of the market struggled as investors grappled with the inflationary implications of a sustained energy shock.

The macro narrative quickly shifted toward stagflation. A weak non-farm payrolls report reinforced concerns that economic momentum is cooling just as oil prices surge, an uncomfortable combination for risk assets. Consumer-facing sectors came under particular pressure as markets began to consider the effect of higher fuel costs on household spending. Materials, consumer staples, and health care were among the hardest-hit groups.

Financial stocks were pulled into the same wave of uncertainty while also facing renewed concerns in private credit markets. BlackRock reportedly wrote down a previously fully valued $25 million private loan to zero only three months after assigning it a full valuation, and subsequently restricted withdrawals from its $26 billion HPS Corporate Lending Fund after redemption requests accelerated. The developments reinforced a broader narrative that liquidity mismatches within the $1.8 trillion private credit market are beginning to surface more visibly, adding another layer of fragility to an already uncertain macro backdrop.

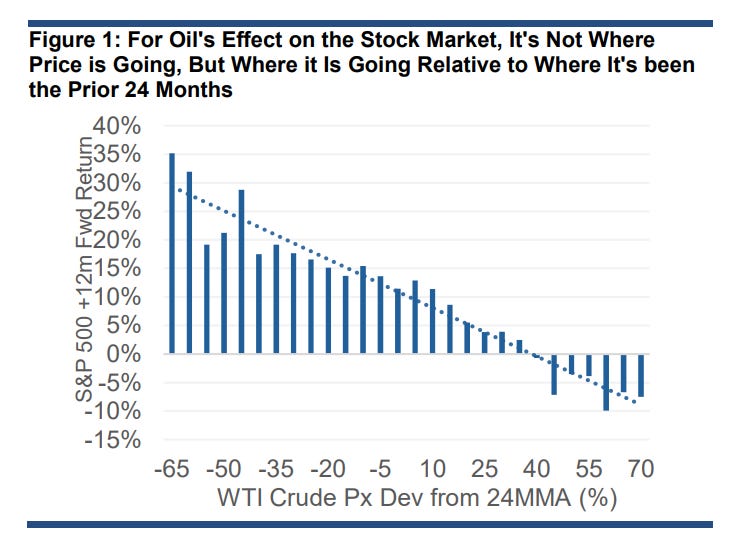

The rise in oil prices now sits at the centre of the market outlook. Crude prices sustained in the $90–$100 range tend to weigh on equity performance over the following year, largely due to their inflationary effect on the broader economy. With tensions in the Middle East escalating and the risk of supply disruptions through the Strait of Hormuz still present, markets remain highly sensitive to any headlines that could shift the trajectory of energy prices.

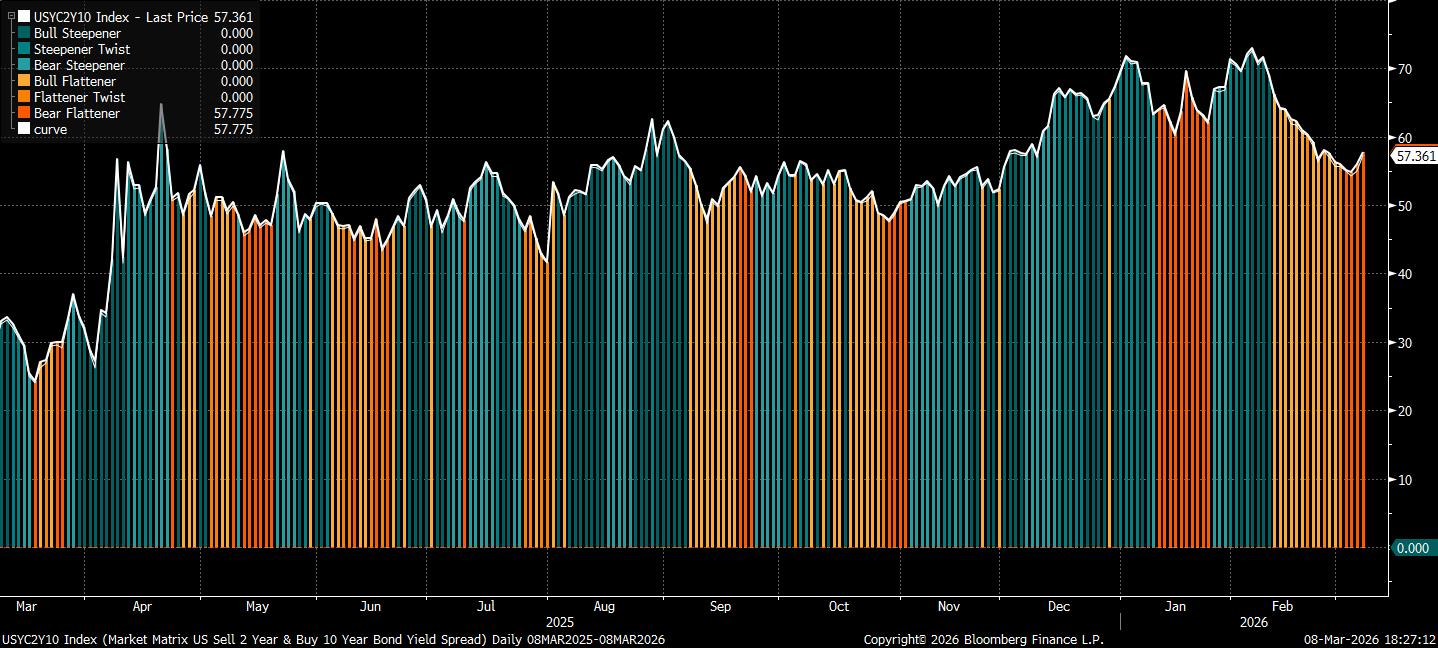

Cross-asset moves reflected this dynamic throughout the week. The US dollar strengthened as the inflationary impulse from higher oil prices supported demand for the currency. At the same time, the weak payrolls report only briefly interrupted the broader trend of USD buying. In rates markets, yields rose sharply in the five- to ten-year sector as investors priced a more inflationary near-term outlook and scaled back expectations for policy easing, bear flattening the curve in the process.

Taken together, markets are now navigating an increasingly difficult macro mix. Growth indicators are weakening while energy prices are pushing inflation expectations higher, leaving the Federal Reserve with little room to move in the near term. For investors, the result is a market that remains highly sensitive to geopolitical developments, with oil prices likely to remain the key variable determining the direction of risk assets in the weeks ahead.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“The Strait is Closed, the Reserves Are Open”

“The Private Credit Stress Test Begins”

“Misallocated Moves in Rates”

“The Last Mile Problem (US Inflation Preview)”

The Strait is Closed, the Reserves Are Open

Part I of our All Happening on the Everything Front is now free for all readers. Part II continues below:

The surge in crude prices following the escalation in the Middle East is already large enough to begin reshaping the macro outlook for inflation, growth and asset prices. Investors spent much of the past year assuming that energy would remain broadly contained, an anchor that allowed central banks to cautiously move toward easing policy without reigniting inflation. That assumption is now under pressure.