All Quiet On The Volatility Front

Preparing for 2025.

Periods of calm are often interrupted by spikes in volatility. Excluding August’s “Yenmagedon” spike in cross-asset vol (a slight overreaction, to put it lightly), things have been too quiet for too long.

Equity markets have been in cruise mode for the best part of 16 months. Bond markets have been whipsawed by Newton’s cradle of rate expectations, as have commodity markets as a whole, for that matter, with the exception of gold’s casual ascent higher.

Continued growth paired with the rising popularity of volatility selling strategies should support a structurally low-volatility environment in Europe and the U.S. These quantitative investment strategies sell options to juice returns but add supply to the market, keeping dealers long gamma. This typically mitigates price fluctuations, as dealers need to buy more futures or shares when the market drops and sell into rallies to maintain balanced positions.

However, as with popular strategies, there can always be a quick change of tides. In these very complacent times, it makes sense to be aware of the shocks that could come, how volatility is likely to impact markets, and how to trade a scenario in which a volatility pickup does occur.

What To Consider

There is a slew of factors that could be major factors in 2025.

The first would be U.S. tariff policies, which will have global implications. Geopolitical tensions have been on the rise this year.

We’ve seen a continuation of the two wars in Ukraine and Gaza, political fallout in Europe, and events such as South Korea’s martial law. Who’s to say if these increase or decrease in the following months?

Overstretched concentration among the U.S. indices and valuation chatter seems to never go away. Maybe that’s an indication that this may not weigh in on any vol event to come, but one to highlight regardless.

Then, there is the labour/inflation dynamic that will continue to grip investors as the world’s major central banks continue a monetary policy easing cycle.

That’s just a few to name. Plenty of events will occur in 2025 that will catch markets completely off guard without any consideration. The 2024 example would be the USD/JPY carry unwind.

Preparing For A Pickup

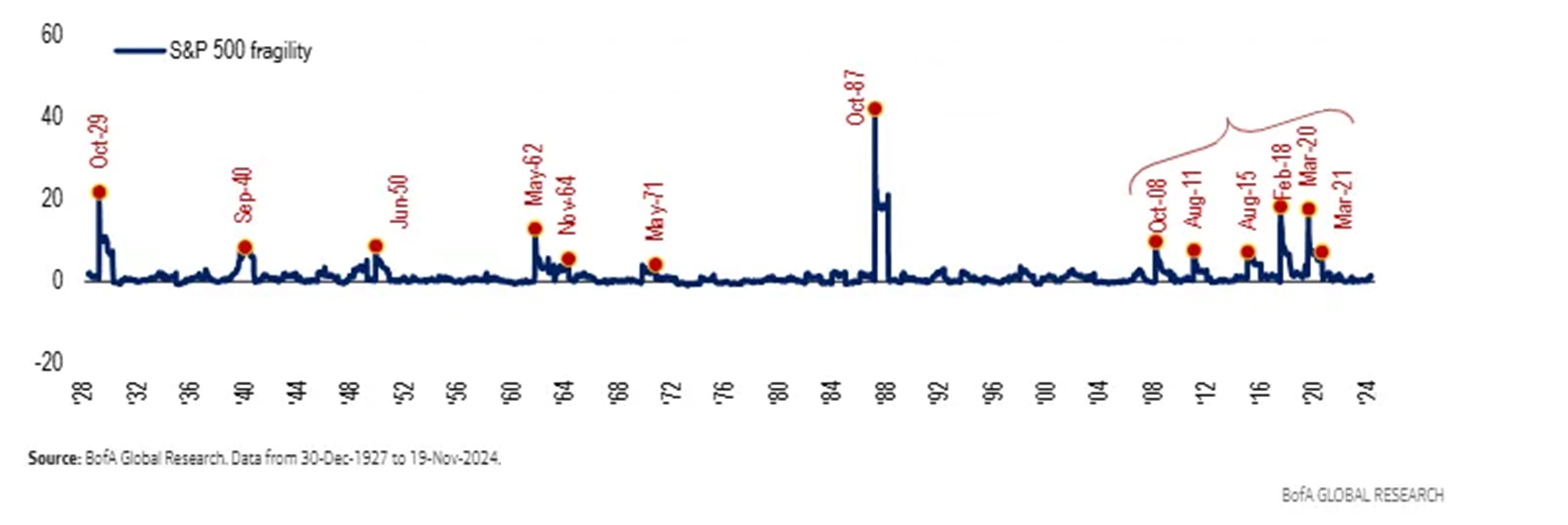

The market can be characterised by long periods of calm followed by “fat tails” (large, sudden, extreme swings).

BofA expects the frequency of fragility shocks in the S&P 500 Index to increase fivefold compared with the prior 80 years and says another index-wide major shock event may be overdue.

Pre-GFC, returning to the 20s, high-fragility1 events were sparsely distributed, occurring roughly once a decade.

In the post-GFC era, these events have been far more common (five in the last 16 years), with February ‘18 and March ‘20 the third and fourth largest, respectively, in almost 100 years.

If you are not yet a premium reader, you can manage your account to get full access to all research.

Trading A Change In Regime

With the post-GFC era seeing heightened quantities of vol spikes and the current stretch lasting longer than usual, do the catalysts of 2025 present an interruption to the calm, or is this the new normal?