Three conversations are coming up more and more when it comes to positioning in the equity space:

Where to allocate capital on the basis of global rates either remaining elevated for longer or simply moving higher.

Where the better areas of the market are, from a valuation perspective, to rotate some profit from AI/tech names.

And defensive angles to portion some funds to help hedge or protect against an expensive market.

In our view, the common area that addresses all three points is financials. We believe bank equities have a credible case as a 12-month thematic. As with anything, it’s not simply as easy as saying “all banks benefit from higher rates,” or that “all banks trade on a low book multiple.” But there are plenty of options for finding likely winners among banks with the right balance-sheet structure (especially asset-sensitive franchises), sticky deposit bases, effective hedging, and manageable credit risk.

There are three drivers to consider: higher global rates, relative value, and defensives in an expensive market. We’ll start with the former ahead of the Fed this evening and the BOE tomorrow.

1) Higher Global Rates

The current policy backdrop is directionally supportive for global bank stocks, but it is not the same story everywhere.

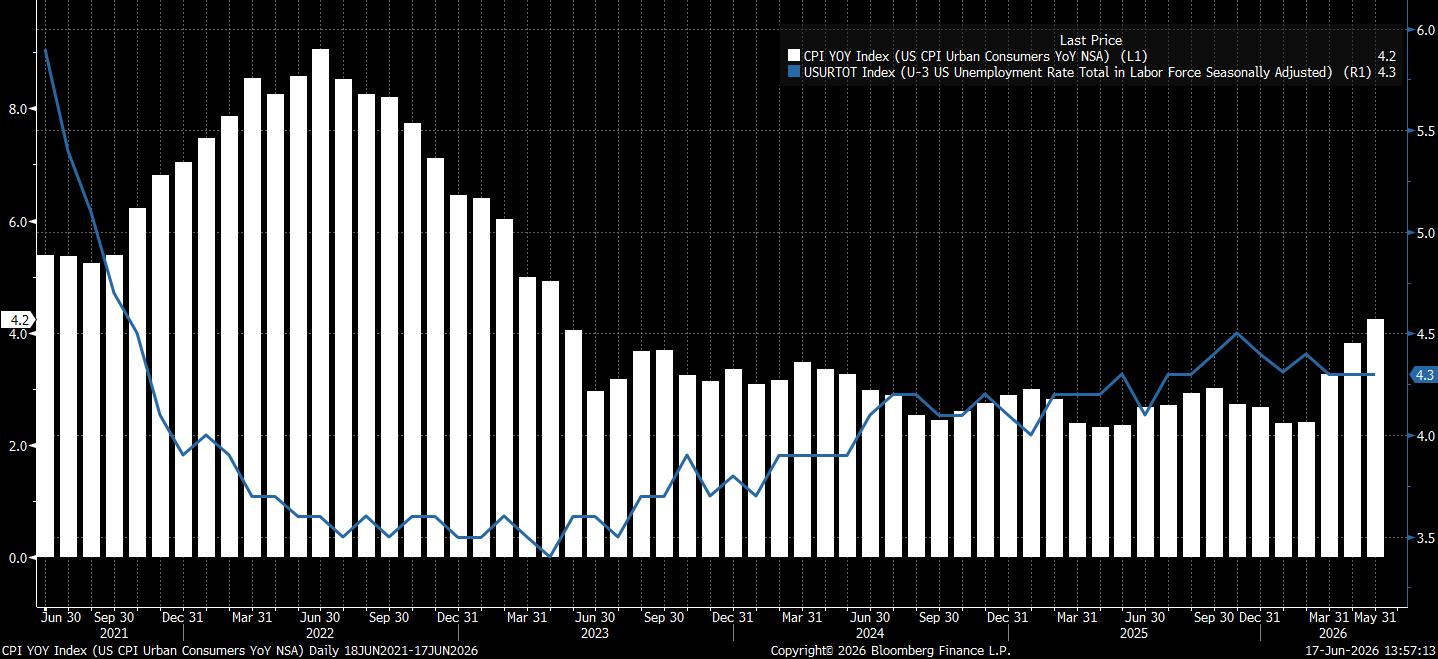

In the US, we pivoted our view earlier this month and now expect the Fed to hike rates this year. The move came after the strong employment report, with labour market conditions now tighter rather than deteriorating. At the same time, growth has remained resilient, and that’s before we start talking about inflation.

The economy is not overheating in a crude sense, but the policy stance is now too easy relative to the data. We think it plausible that the unemployment rate will fall gradually toward 4.0% by year-end, but see the headline CPI staying in the 3.5-4% range over the same period — a “higher-for-longer” backdrop for US banks.

In the euro area, the story is even cleaner for the theme. The ECB raised all three key rates by 25 basis points on 11 June, taking the deposit rate to 2.25%. The ECB’s own statement said euro-area headline inflation is expected to average 3.0% in 2026, and Eurostat’s May flash estimate put current euro-area inflation at 3.2%, up from 3.0% in April.

The tone of the presser was hawkish. Even though Lagarde did not pre-commit to further hikes, the updated inflation figures (and downgraded growth projections) clearly shifted the burden of proof. With inflation revised higher, core inflation above target through 2028, and adverse scenarios indicating a meaningful risk of second-round effects, the GC has effectively told markets that today’s hike won’t fix all of that and, therefore, more tightening is needed. We spoke about this factor specifically in our note last week, “After You, Christine.”

In the context of today’s equity focus, European banks have been among the main beneficiaries of post-2022 margin normalisation, and we expect this to continue into H2 2026.

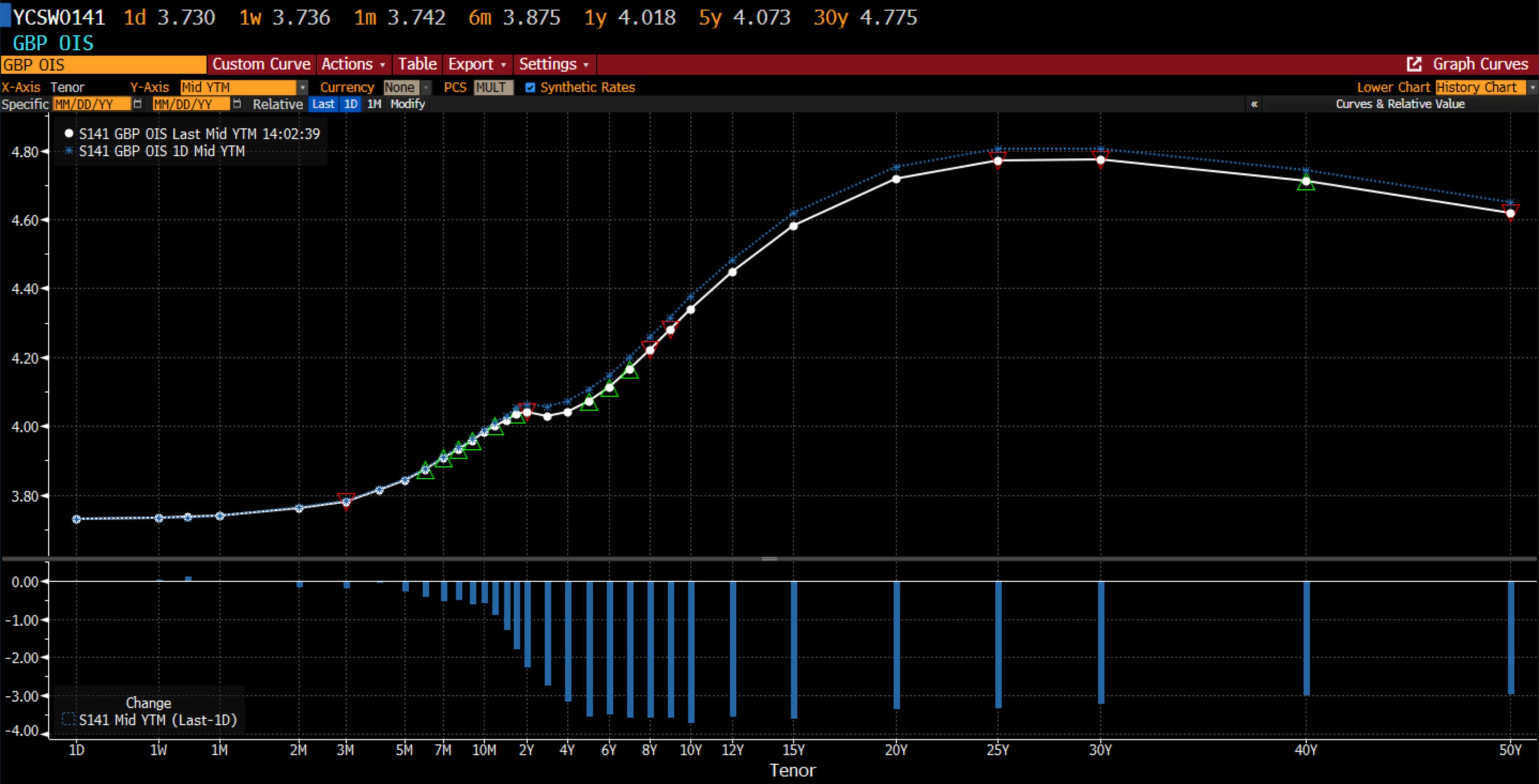

The UK sits between those two cases. Headline May CPI out today held at 2.8% YoY, defying consensus expectations of a rise to 3.0% and coming in at the low end of the forecast range (2.8%–3.2%). The ONS attributed the softer reading in part to lower food costs, particularly meat and dairy products, which offset other upward pressures. Money markets trimmed BOE rate-hike bets, with swaps implying ~27bps of hikes for the year versus ~29bps the prior day.

The data reinforces expectations that the BOE will hold the benchmark rate steady at 3.75% at its meeting tomorrow, but the consensus view of one hike for this year still makes complete sense. The services inflation beat, and broader inflationary pressures already in the system, are likely to push CPI higher into year-end.

For UK banks, that makes the coming period less a pure hiking story than a higher-for-longer plus structural-hedge story.

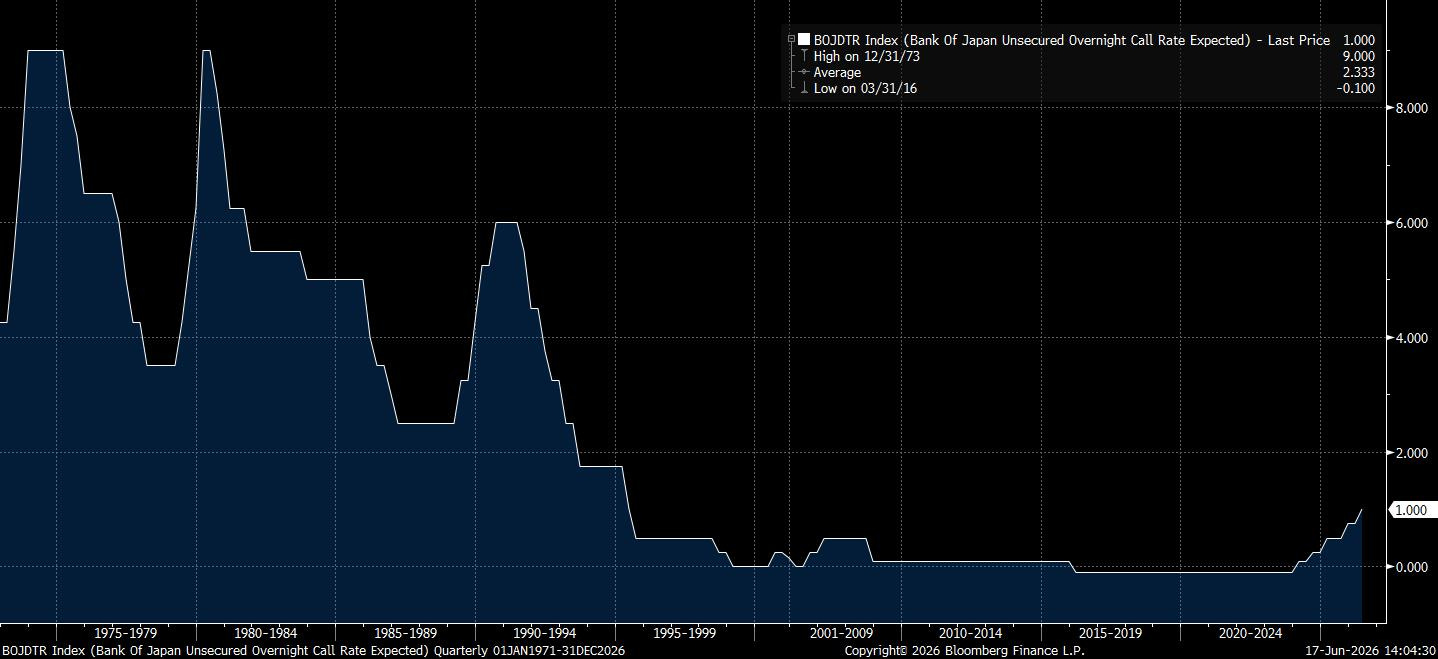

Japan is the smallest absolute-rate market in this set, but arguably one of the most important in directional terms because it is coming off decades of ultra-loose policy. For Japanese banks, the thematic is therefore about normalisation from a very low base, which can have an outsized effect on margins and investor perception.

TLDR: The thematic is strongest in Europe and Japan, where policy direction is still moving towards tighter conditions, constructive but more selective in the UK, and more valuation-driven in the US, where the benefit comes less from fresh hikes already delivered and more from the market’s retreat from rate-cut expectations.

2) Relative Value

Cheap sectors are only interesting if they are cheap for no good enough reason. Other than that, they’re cheap for a reason.