The S&P 500 marched higher for a seventh consecutive week, though sentiment was clearly different on Monday versus Friday. The initial AI-led melt-up ultimately gave way to a broader realisation that equity markets can only decouple from the bond market for so long. A sharp global selloff in duration pushed US 30-year Treasury yields above 5%, driving long-end rates to levels not sustainably seen since before the GFC. Markets are now being forced to reckon with the idea that elevated yields may not be a temporary volatility shock, but a more structural feature of the macro environment.

Earnings helped sustain momentum in the semiconductor complex for much of the week, with investors increasingly treating any short-term weakness as a buying opportunity rather than the beginning of a broader unwind. Q1 has shown that semiconductor earnings strength is fundamentally different from the late-1990s revenue mirage.

Geopolitics added another layer of pressure. During his visit to China, President Trump’s remark that the US did not need the Strait of Hormuz open triggered a sharp rebound in oil prices, reinforcing the view that even if active hostilities in the Middle East fade, energy markets are unlikely to return quickly to pre-war normality.

The final pressure point came from abroad. Political instability (“The Starmer Drama”) in the UK triggered a disorderly selloff in gilts, particularly in the long end, which spilt directly into global bond markets. The combination of higher inflation prints, elevated oil prices, and fiscal concerns abroad created a toxic mix for duration. Treasury yields accelerated sharply higher into Friday’s open, with the move in long-end rates finally becoming too large for equities to comfortably ignore.

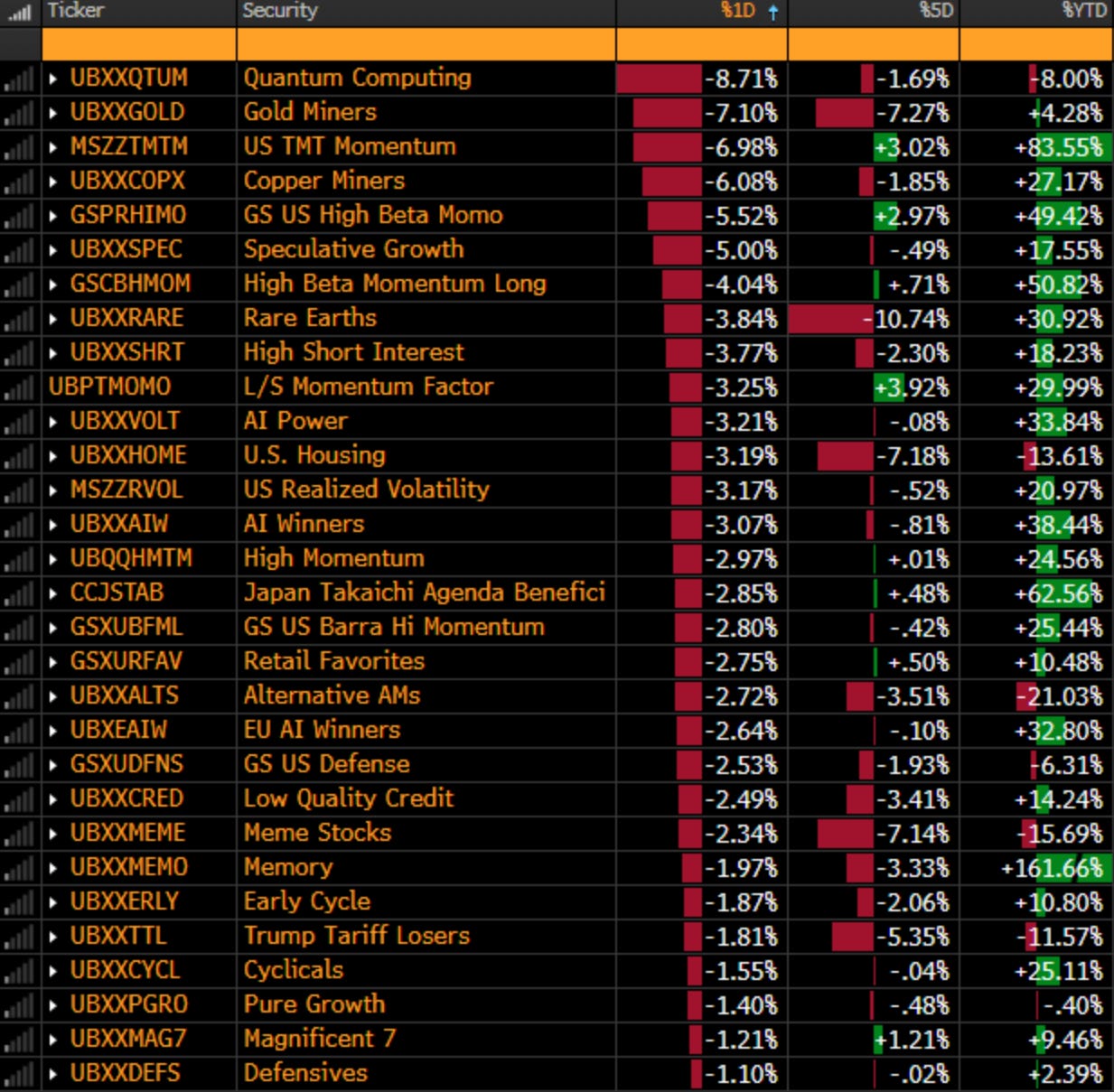

That dynamic was particularly visible in the market leadership reversal late in the week. High-duration growth equities, especially speculative technology and non-profitable tech names, came under renewed pressure as real yields rose.

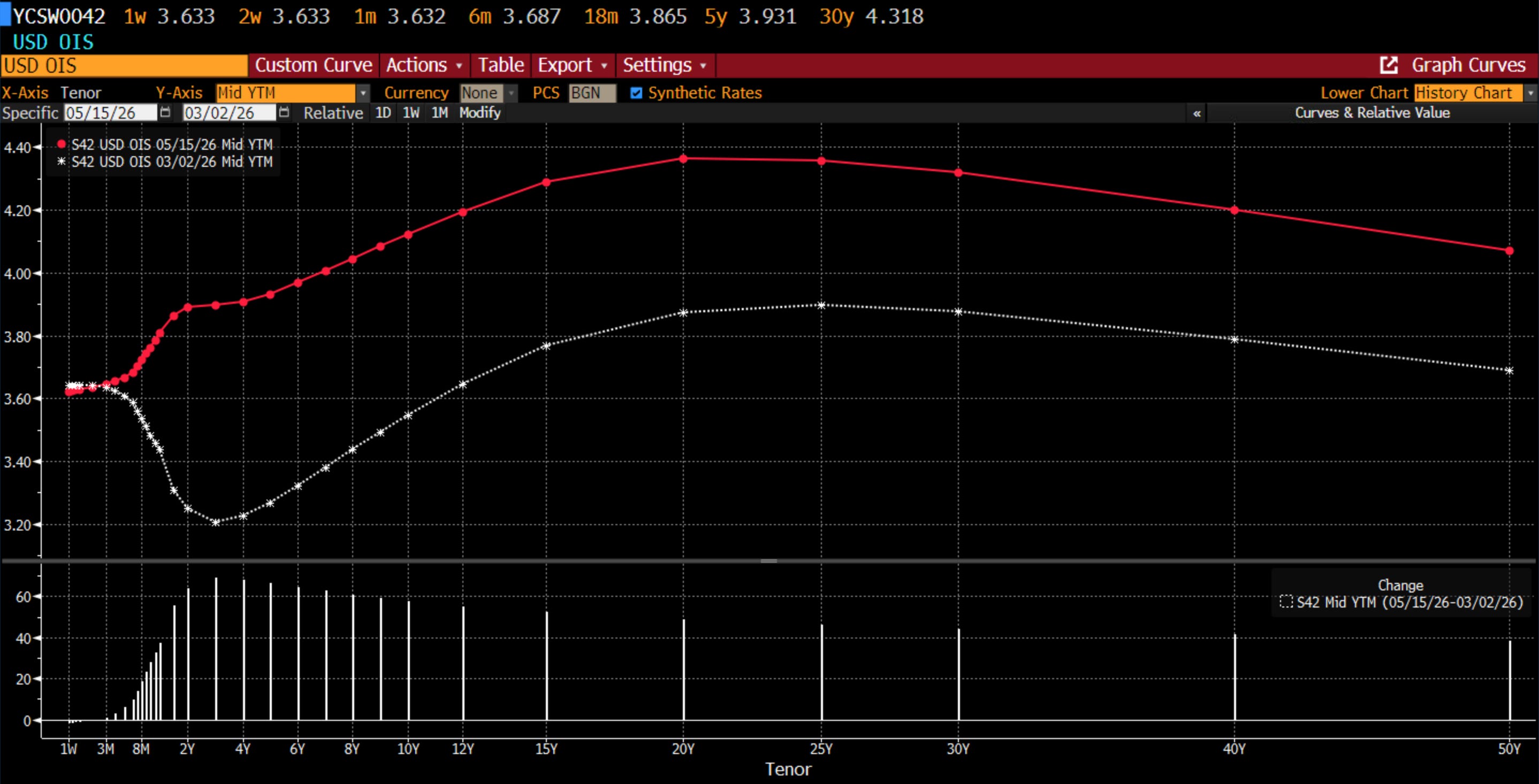

On policy, OIS markets now fully price a 25bp hike by March 2027, a remarkable shift from early March, when traders were still pricing cuts for late 2026. The direction of travel matters as much as the level itself.

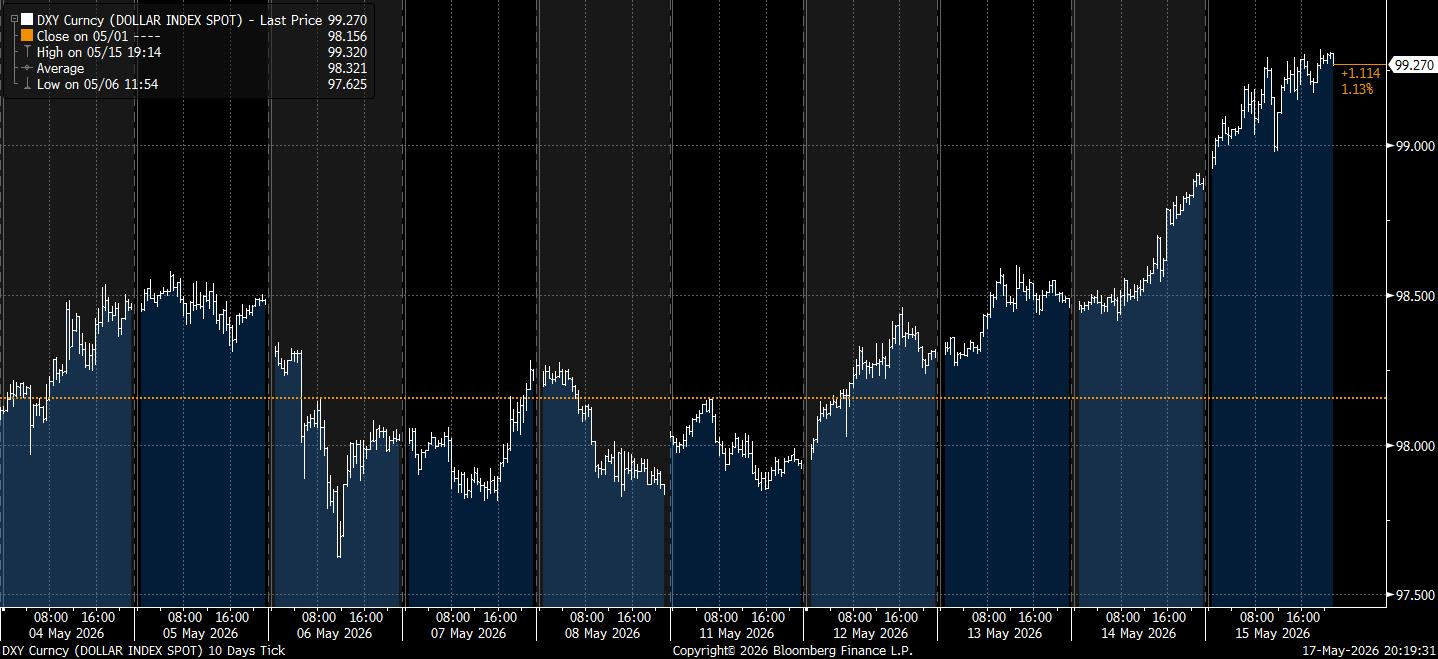

In FX, the dollar benefited from almost every major macro theme simultaneously: higher oil prices, stronger rate differentials, geopolitical uncertainty, and weakness in sterling.

For months, AI enthusiasm, resilient earnings, and systematic inflows have been able to overwhelm macro concerns. Friday served as a reminder that there are still limits. As long-end yields move toward cycle highs and inflation remains sticky, the market’s tolerance for expensive duration-sensitive assets becomes increasingly fragile. The AI trade remains intact. The question now is whether it can continue carrying the broader market alone in a world where the cost of capital is structurally moving higher.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“Inflation, Inflation, Inflation”

“Semi’s: 2000 vs. 2026”

“You Win Summ(it), You Lose Summ(it)”

“Nvidia Earnings, Same Old Story?”

Inflation, Inflation, Inflation

UK

The week ahead for the UK promises a lot to digest for markets, both on the political front and in the economic data.

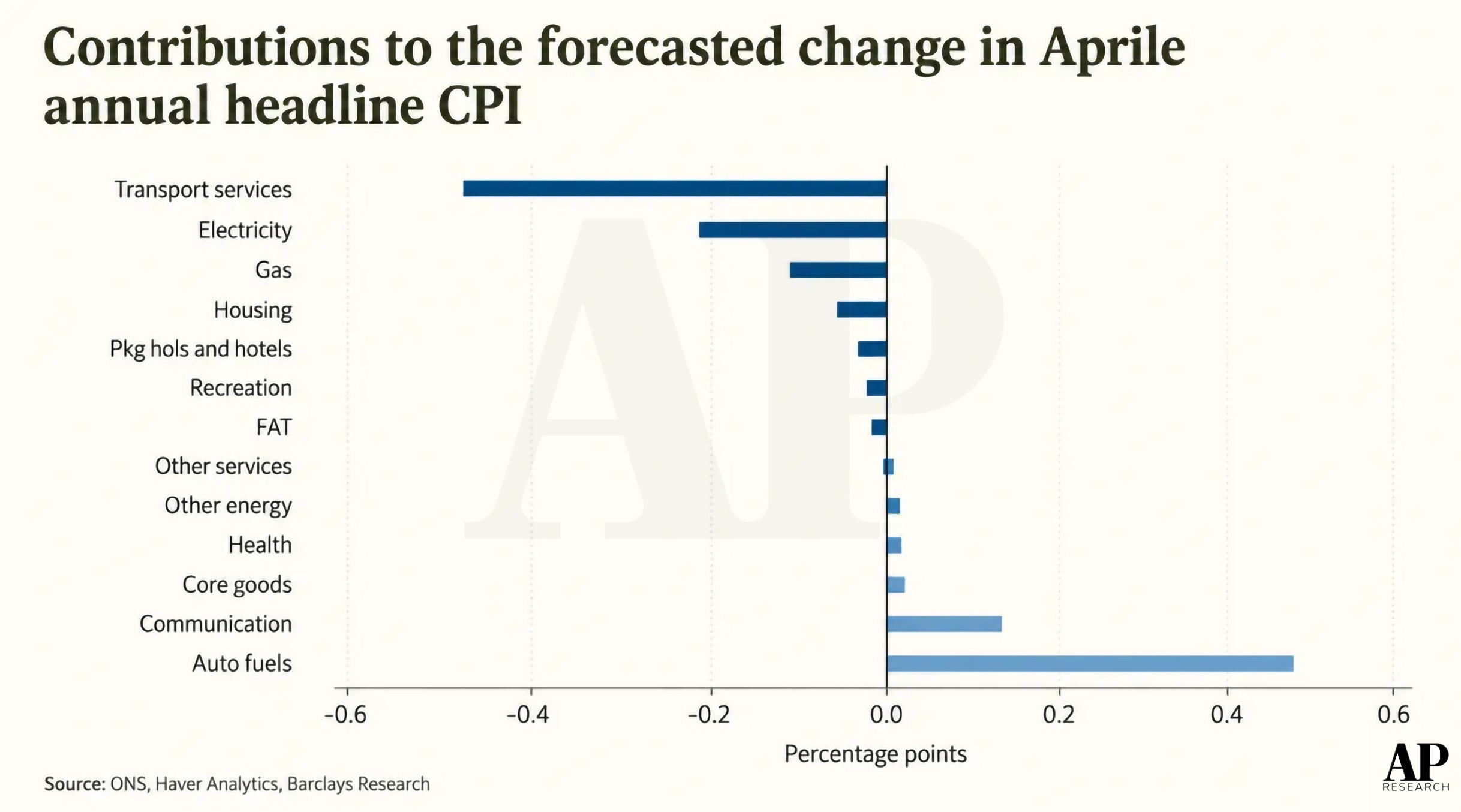

Let’s start on the data side. April UK inflation is expected to deliver a modest fall, with headline CPI forecasted to slow 0.3% to 3.0% y/y, broadly in line with the Bank of England’s April MPR forecast, while core CPI is expected to fall more sharply, down 0.5% to 2.6% y/y.

This might surprise some, given the UK economy’s sensitivity to the energy spike. Yet if we look below the surface, the headline print should be restrained by softer services inflation, even as the energy complex moves higher. Pump prices are expected to rise materially as the shock continues to feed through to petrol and diesel, but this is partly offset by the fall in the Ofgem dual-fuel cap following measures announced in last autumn’s Budget.

If we had to summarise what the inflation print is likely to show us, it’s that services disinflation is doing the heavy lifting, energy is moving in the wrong direction, and food remains sticky but not accelerating. However, this print shouldn’t be treated with much slapping on the back from politicians or even from MPC members. There’s still plenty of work to be done on price levels, and the caution is not to get lulled into a false sense of security here.

Now let’s pivot to politics, which has been the main driver behind the spike in Gilt yields, particularly at the long-end.