China's Bazooka

The slump, the stimulus and the stock market.

There were glimmers of hope in the early stages of 2024 for China equities. However, the equity rally from fiscal stimulus was short-lived. Here we are in September, and global concerns regarding China persist.

The nation’s economy, plagued by property market challenges and sluggish economic indicators, is experiencing prolonged repercussions from the pandemic. The enduring impact of extensive lockdown measures implemented since 2020 is evidenced by a weakened GDP, a struggling stock market, and elevated unemployment rates, shattering expectations of a swift post-pandemic recovery.

While everyone is so down on China, there may not be much more in the way of a downside surprise, but another stimulus from the government may be the tailwind needed for a rally in this market.

The slump

With concerns mounting over economic growth, particularly following August data that cast doubt on China’s ability to achieve its targeted growth rate of around 5% this year, there is increasing pressure on the government to take additional measures to support the economy.

At the heart of China’s problems is the real estate sector, which has led to an estimated $18 trillion reduction in household wealth. The knock-on effects of this slump have resulted in widespread job losses, weakened consumer confidence, and reduced demand for commodities such as steel.

The real estate crisis has also pushed China into its longest streak of deflation since 1999. That means real interest rates (which are adjusted for changes in prices) have stayed high, weakening the impact of any moderate easing.

While US households have ~23% of assets in property, China’s population have ~62%. Hence, the consumer is feeling some pain from this drawdown.

The stimulus

Calls for greater stimulus in the world’s second-largest economy are rising. The urgency behind this call is led by the importance of China not missing its 5% GDP target, which leaders reiterated in July. Earlier this month, Goldman Sachs joined other institutions in cutting their annual growth forecast for China, reducing it to 4.7% from 4.9% estimated earlier.

China generally wants a weaker yuan as it’s better for exports. When the Fed cut rates last Wednesday, USD/CNH moved lower, threatening to break below 7.00 for the first time since May 2023. Therefore, we thought the People’s Bank of China (PBoC) would have followed suit last week, cutting its loan prime rates the day after the Fed’s move. In doing so, it would have the ability to offset the USD weakness, with a rate cut that would act to neutralise the rate differential. Yet, it made no such move.

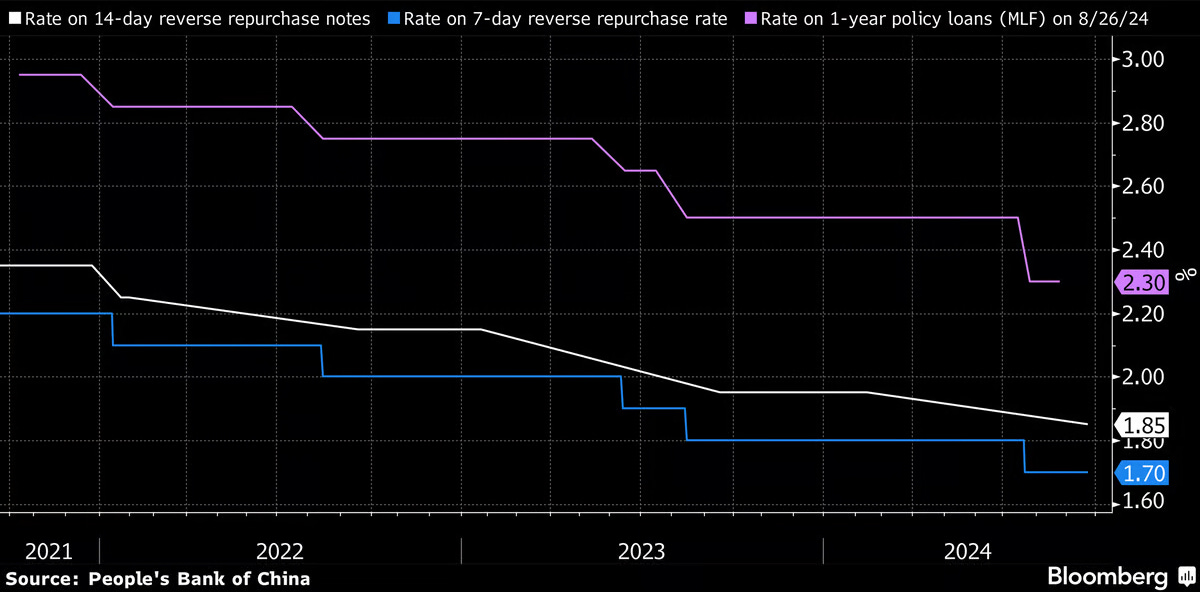

Instead, it was only at the start of this week that they made a move. On Monday, the PBoC lowered the 14-day reverse repurchase rate by 10bps, catching up with reductions initiated in July and pumping 74.5 billion yuan ($10.6 billion) of liquidity into the financial system.

On Tuesday, China delivered the so-called “bazooka,” by far the broadest push year-to-date from Chinese authorities.

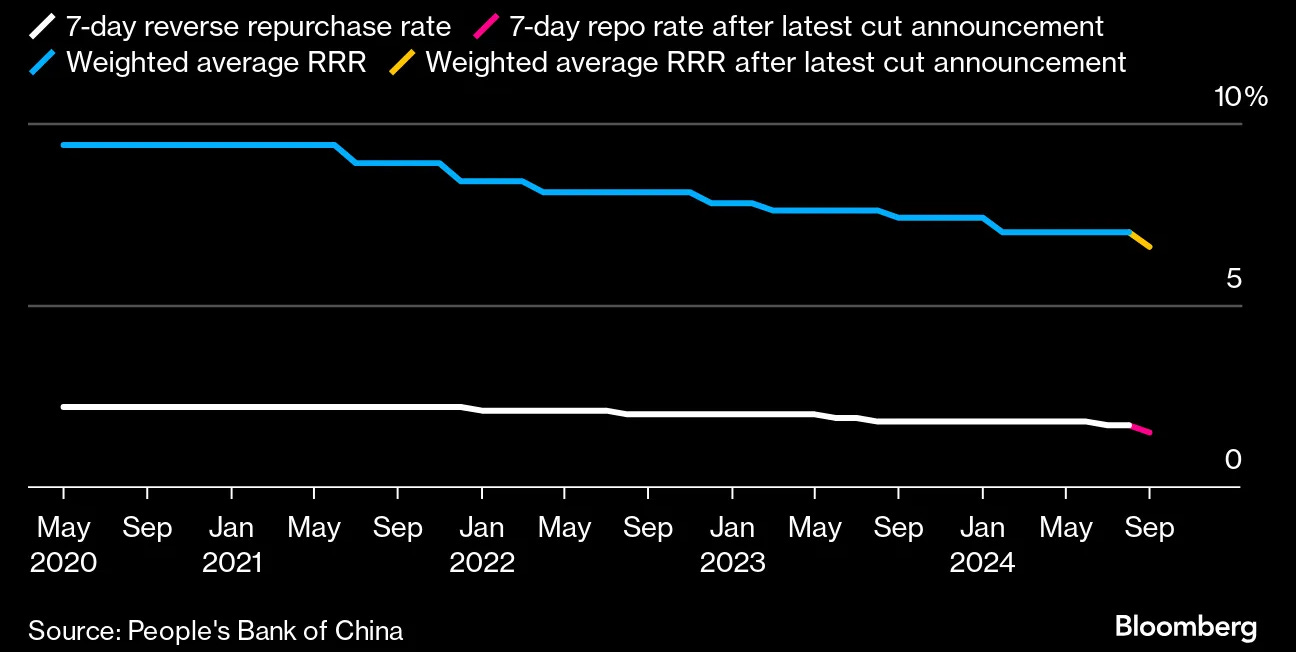

PBoC Governor Pan Gongsheng announced a cut in the RRR1, seven-day policy rate, and existing mortgage rates in a bid to boost lending and reduce the existing loan burdens. He also said further RRR cuts are possible.

Outstanding mortgage rates for individual borrowers were cut by an average of 0.5 percentage points. The minimum down-payment ratio on second home purchases will be lowered to 15% from 25%. This is in an effort to both encourage buying in a falling property market and loosen the burden of the consumer.

Pan also announced at least 500 billion yuan ($71 billion) of liquidity support for stocks. Securities, funds, and insurance companies will be able to tap the PBoC to buy stocks through a swap facility, and told reporters that authorities are studying setting up a stock stabilisation fund.

This is probably the most aggressive sentiment booster that the PBOC and market regulators can introduce before the US election. These measures were thoughtfully orchestrated, providing valuable guidance for potential future easing.

One standout was Governor Pan saying, “If 500bn is not enough, then we can do another 500bn.” The market may finally be back to life.

For investors, the initial shot is good. Now, it’s a game of figuring out if China has aimed their bazooka accurately enough to make the right mark.

We called up a good friend, Le Shrub, to chat about the matter.

Mandatory Shrub meme before moving into the trade plan…

The stocks (and other asset ideas)

Maybe it’s time to start thinking about an upside trade with a policy apparatus that came through with more significance than expected—or at least, it didn’t disappoint.