If you spend long enough in the ring, you’ll come out with a few bruises. The AI trade is starting to bruise after its latest round.

US equities ended lower after a rough week for tech stocks, with the Nasdaq suffering the bulk of the damage as markets reassessed the valuations, positioning, and durability of the AI rally. A warning shot from Asia carried across to US equities, an upside surprise from Micron couldn’t hold for long, and by the end of the week, the sector breakdown looked much more defensive.

Leverage is very much at play here. Highly leveraged semiconductor ETFs create a messy gamma backdrop, forcing dealers to hedge aggressively as volatility picks up — and it has. Pressure transmits from derivatives into cash equities, which amplifies the moves in sectors which have become crowded after aggressive moves higher. The volatility spread between Nasdaq and the S&P is at its highest since 2020.

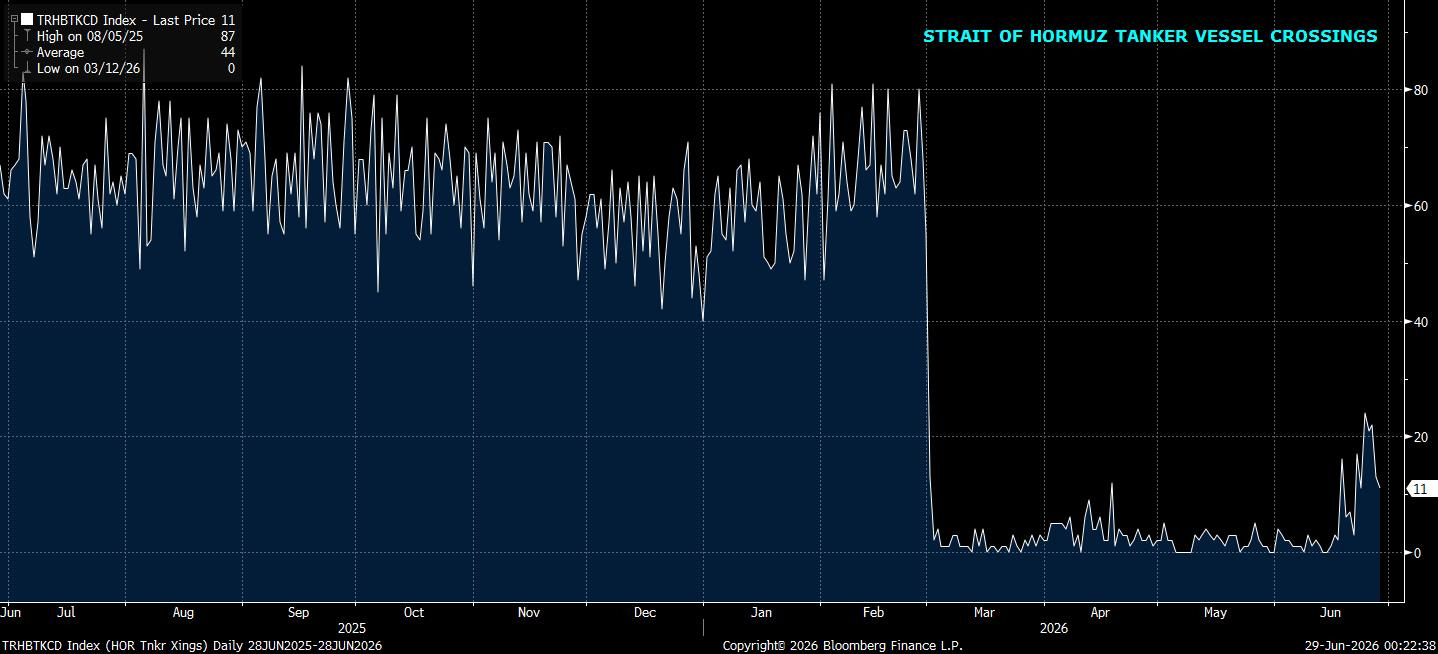

The rotation away from tech was softened by falling oil prices. Traffic through the Strait of Hormuz continued to increase, helping crude extend its decline and giving airlines, especially, a major boost. Lower fuel costs do not solve every consumer problem, but do help offset some of the pressure from higher rates and elevated prices. Without that move in oil, the equity selloff would have looked more severe last week.

On the macro side, May PCE came in slightly softer than expected and triggered a dovish cross-asset reaction. That reaction shows how sensitive markets have become to any sign of disinflation now that the FOMC is focused almost entirely on one side of the dual mandate. Fed speakers didn’t give investors any extra comfort. Goolsbee, Williams, and Kashkari all reinforced the message that inflation is too high, risks remain elevated and further tightening is still possible.

Goolsbee: Core inflation is too high and is trending the wrong way

Williams: Substantial risks to inflation remain; sees level at 3.5% at the end of 2026

Kashkari: Sees need to hike this year due to elevated inflation

Bloomberg’s Fedspeak index shows continued hawkish language, despite Z6 pricing easing.

The Treasury curve rallied as markets smoothed out the path of expected hikes rather than pricing a more urgent tightening cycle. Monday may have been peak hawkish sentiment, but given how the rates trade has played out this year, that view may come back to bite us. The move helped fade some of the prior bear flattening, but it did not change the broader policy picture. The Fed remains live from July onward, and the next payrolls report now carries extra weight after Warsh’s recent hawkish reset.

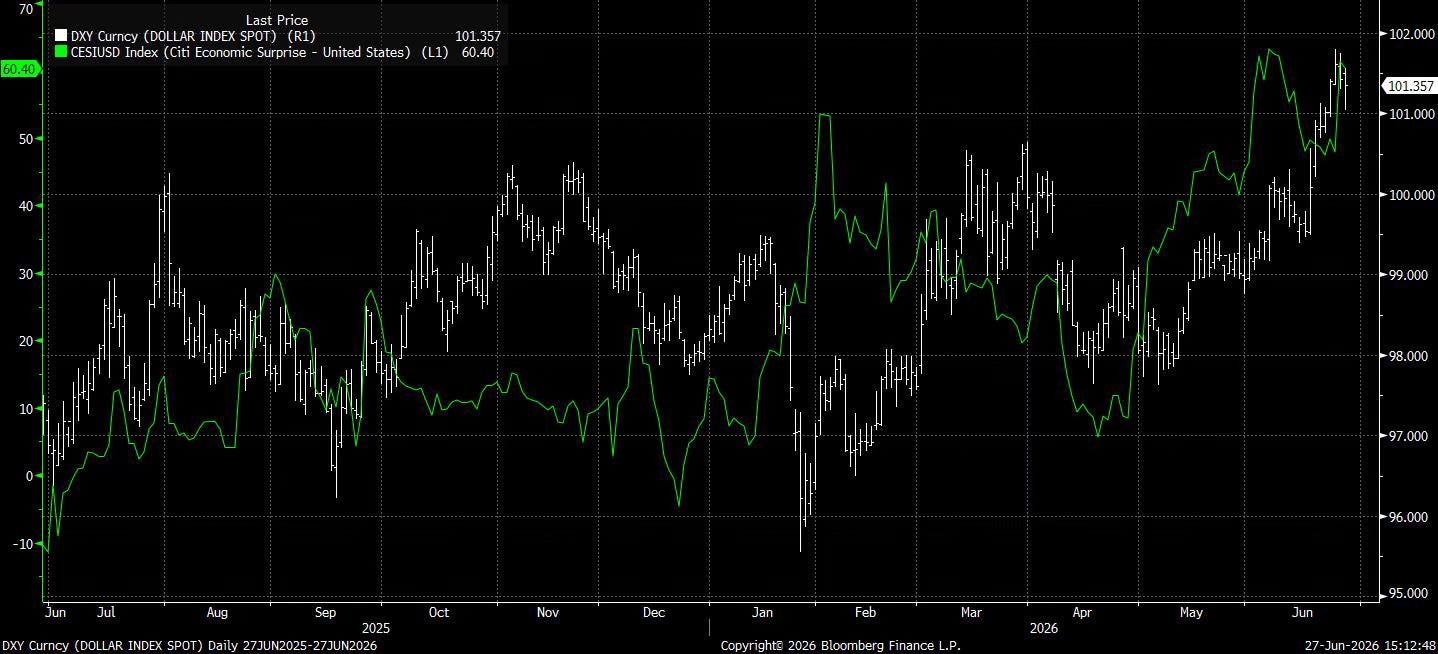

The dollar continued to benefit from the macro backdrop. Institutional positioning has shifted more bullish as solid US data, the prospect of medium-term Fed hikes, and still-resilient equity inflows make the dollar attractive against lower-yielding currencies. The rally was limited by falling oil prices and month-end flows, but the structural tone is firmer than it was earlier in the year.

Elsewhere, Starmer is gone. Burnham is set to be next in command, but in hock to the bond market. We’ll have a specific note out on the UK in due time.

Lower oil and resilient earnings are keeping the broader equity market supported, but the leadership is becoming more fragile. In thinner summer liquidity, we see that as a caution to pay attention to.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“Putting Debasement Through the Warsh”

“A Bruising Round for the AI Trade”

“Dollar Haven”

“Defensive Allocation (portfolio update)”

Putting Debasement Through the Warsh

The gold trade, or the debasement trade as it became known in more excitable corners of the market, took another leg lower last week.

What began as a fundamentally driven thesis morphed last year into something more speculative. It then ran into a sharp selloff in late January, before facing fresh pressure as oil soared and dollar demand refused to roll over. Sell your gold pieces for dollar bills (more on this later).

That is not to say there is no perfectly good rationale for central banks to hoard gold. There clearly is. But at the height of debasement-trade thinking, gold was being bought not only as protection against US financial warfare, fiscal deterioration, or the slow erosion of fiat credibility. A meaningful slice of demand for gold (silver and Bitcoin were speculative, too) was bolstered by the sense that the Federal Reserve was moving out of sync with a broader tide of central bank tightening.

In late March, we laid out why we still believe in the trade over the medium- to long-term, with a predominant focus on oil and dollar demand dynamics…

…However, gold now faces a fresh headwind to overcome before the upside case can reassert itself.

With new Fed Chair Kevin Warsh taking a more hawkish approach, the idea of the Federal Reserve being meaningfully out of step has been kicked into touch. Inflation expectations have fallen quickly enough to become a gift for long-end Treasuries, while the shift from expected rate cuts to expected rate hikes has pushed the Fed toward the more hawkish end of the central bank spectrum. That has supported the dollar. It has also made the short end of the Treasury curve look much more interesting, with 2-year yields now well above 4%.

Kevin Warsh’s reputation was already well known on Wall Street. Note the inflexion point across XAU, BTC, DXY, and 2s10s after his nomination.

For investors looking for something to speculate on, AI and chip stocks still offer the cleaner dopamine hit. Admittedly, that comment might sound off after last week’s price action, but the broader point holds. Precious metals and Bitcoin are no longer the obvious home for marginal speculative capital as they were when the market was convinced the Fed was about to turn dovish.

The sell-side has started to reflect that shift. Deutsche Bank cut its gold price forecast to $4,300 for the third quarter, down by more than a fifth from its prior outlook, and to $4,800 for the final three months of the year. That followed Goldman Sachs, which last week cut $500 from its year-end target to $4,900, as it now expects no rate cuts from the US central bank this year.

If the Fed has regained a hiking bias, it is hard to see how the debasement trade materially benefits in the short term. To be clear, the argument was never solely about monetary policy. Concerns over government borrowing, debt sustainability and the political incentives around inflation remain firmly in place. The US budget deficit is still running close to 6% of GDP, despite Treasury Secretary Scott Bessent’s pledge to halve it by the end of Trump’s term.

The debasement narrative is structural, and has not disappeared altogether. But structural stories still have to survive cyclical pressure, and right now the cyclical pressure is running in the wrong direction for gold.

A Bruising Round for the AI Trade

The AI trade had its first proper wobble in a while last week.