Global Primer Series: Private Credit

Mapping the system behind the boom and the software fault line now being tested.

Private credit used to sit at the edge of institutional portfolios. It now sits much closer to the centre, and increasingly, at the centre of the debate. The US private credit market is approaching $1.3 trillion1 and now accounts for roughly 30% of debt issued by below-investment-grade US companies, up from 13% immediately after the global financial crisis. On broader global definitions, BlackRock put private credit assets under management above $2.2 trillion as of March 2025, while other industry estimates now place the sector nearer $3.5 trillion. That spread in the numbers is a reminder that even the market’s basic outline depends on where one draws the boundary.

Most private loans are negotiated directly between a borrower and a small group of nonbank lenders, do not trade in a secondary market, and are typically held until maturity or refinancing. Price discovery is therefore episodic. Volatility appears lower, not necessarily because the underlying businesses are any safer, but because the loans are not forced through a public screen every second of the day. In calm periods, it looks resilient. In stressed periods, less so.

That dynamic explains why the first real tremors in private credit tend to show up outside the loans themselves. Commonly today, they are appearing in listed business development companies (BDCs), in discounts to net asset value, and in the share prices of listed alternative asset managers. Software stocks, which account for a larger sector weighting in private credit, fell almost 30% between October 2025 and February 2026 (SaaSpocalypse), while BDC shares fell about 10% on average, and discounts to NAV deepened. Public wrappers have started doing the price discovery that the private loans themselves do not.

It is also important to keep some restraint. Private credit is not a deposit-funded banking system. Nonbank private credit lenders generally have limited asset-liability mismatches and modest leverage compared with banks, while redemption gates and lockups can reduce the risk of fire sales. Even now, some large market participants argue that current strains are more liquidity- and rate-driven than evidence of a systemic default cycle.

The reason this debate has sharpened (and the purpose of this primer) is software. A growing share of private credit is now effectively exposure to sponsor-backed software businesses, concentrating risk in a sector whose assumptions are beginning to be tested.

What follows in the first part of this primer is as straightforward as we can make it. Strip private credit back to basics, map the money, and explain why the model looked so good for so long. Then we explore why software sits much closer to the centre of the story than many investors appreciated, and how the stress travels if conditions worsen.

Table of Contents

Private Credit Primer

1.1 What Private Credit Actually Is

1.2 Who the Players Are and How the Money Flows

1.3 Why It Worked

1.4 The Bridge to the Fault LineSoftware Stress Test

2.1 This Is No GFC Call

2.2 The Market Is Already Speaking

2.3 Why Software Is the Pressure Point

2.4 Plumbing Matters More Than the Headline

2.5 How the Stress Travels

2.6 A Banking Spillover Looks Limited But Real

2.7 What to Actually Worry About

What Private Credit Actually Is

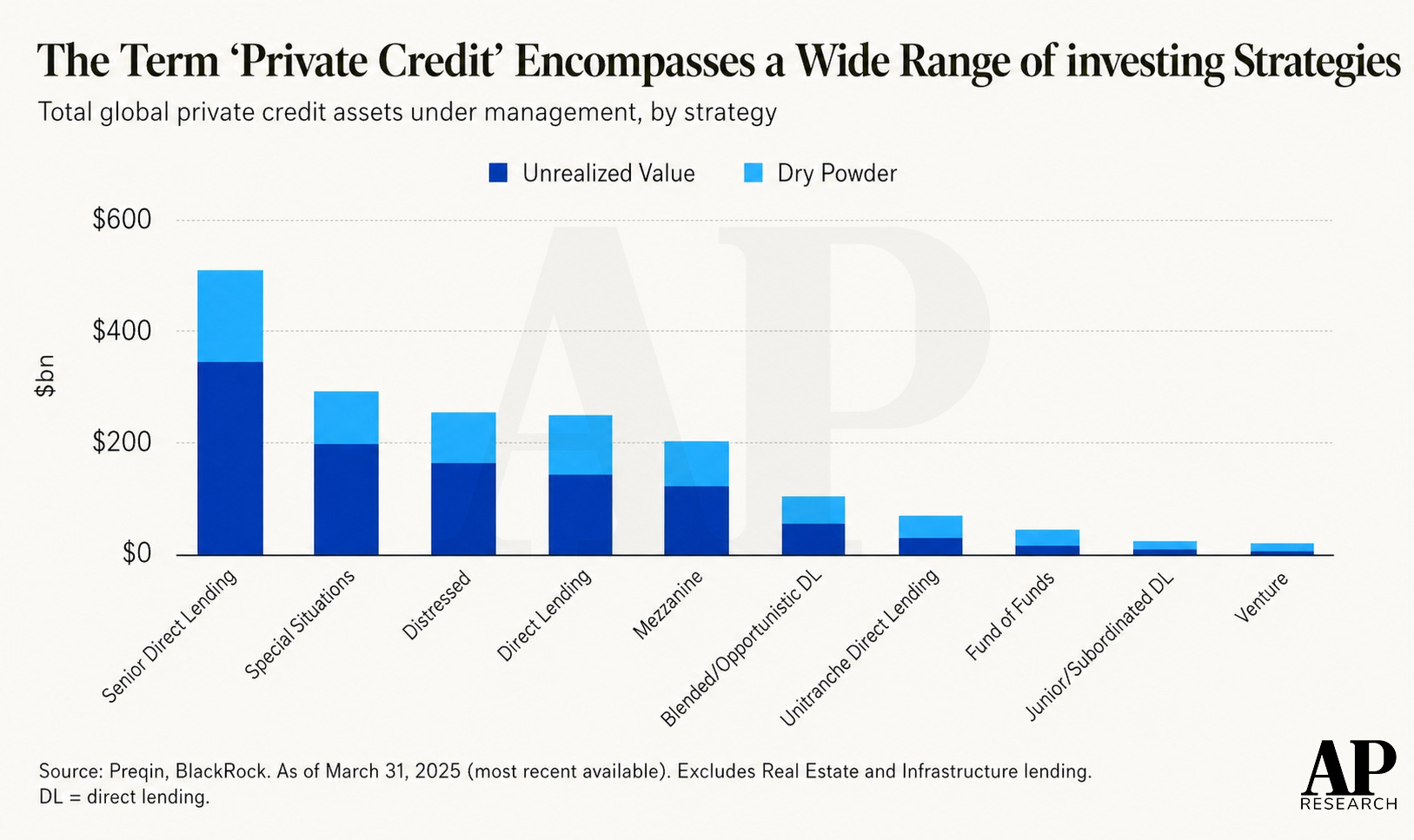

The cleanest way to define private credit is functionally rather than academically. It is credit that is originated, structured and held by lenders. It is debt-like, non-publicly traded instruments provided by nonbank entities such as private credit funds and BDCs. In practice, when most investors talk about private credit, they usually mean direct lending: a nonbank lender makes a loan (or a small club of lenders makes a loan) directly to a company and keeps that exposure on its balance sheet rather than distributing it across a broad syndicated market. Direct lending is also the dominant sleeve of the asset class, accounting for roughly 54% of global private credit AUM2.

That sounds simple, but the distinction from public credit is important. A broadly syndicated loan or a high-yield bond must be marketed to a wider investor base, often with ratings, fuller disclosure, a syndication timetable, and the risk that market conditions change before a deal clears. Direct lenders sell something else: speed, confidentiality, certainty of execution, bespoke terms, and a smaller lender group on the other side of the table. Borrowers are willing to pay a premium for that. In short, fewer disclosure requirements and far fewer lenders.

The instruments themselves are fairly recognisable. Almost all private credit loans are senior secured and floating-rate, usually priced at a spread over a benchmark such as SOFR. Direct lending loans are typically senior in the capital structure and often built around financial covenants. The point, from the lender’s perspective, is to sit high in the capital stack, collect current income, and avoid unnecessary duration risk.

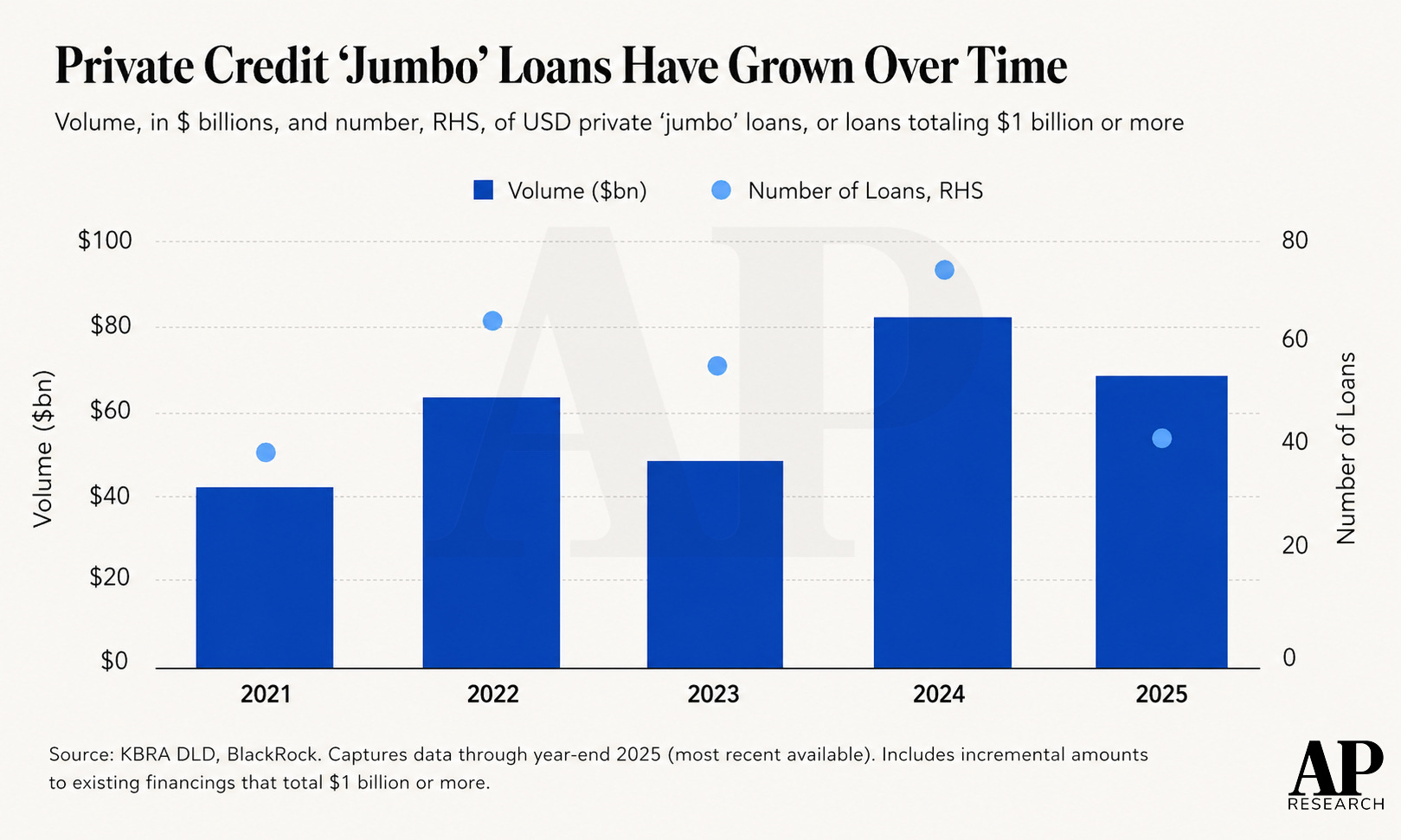

Historically, the core borrower was a middle-market company (EBITDA between $25 million and $100 million), though the borrower profile continues to evolve alongside the broader growth of the asset class, with some companies above $100 million in EBITDA and loan sizes above $1 billion (jumbo loans). Among the growth in borrower type has been an increase in these “jumbo” loans, and, in recent years, the count of sponsor-backed direct lending deals in US dollars has exceeded that of the broadly syndicated loan market. Private credit has moved from a niche funding source for undersized companies to increasingly compete with public leveraged finance markets for mainstream sponsor-backed deals.

Sponsor backing3 is central to the machine, which accounts for roughly 80% of the direct lending market. Private credit is especially well-suited to leveraged buyouts, add-on acquisitions, recapitalisations and refinancings, where a sponsor values certainty and a lender values control. Put differently, private credit finances more than just organic corporate capex, and can often finance ownership structures, too. The borrower may be a company, but the real counterparties are frequently the sponsor and the lender.

So, what problem is private credit solving that banks no longer want to?

The answer is not mysterious. A large part of post-crisis nonbank lending reflects regulatory constraints on banks’ ability to lend to unprofitable and highly leveraged borrowers. US commercial banks have halved in number since 1998; the top 25 now hold more than half of all C&I loans (commercial and industrial), and balance-sheet priorities have shifted away from smaller, riskier corporates. Private credit stepped into that financing gap, then discovered it could do much more than fill it.

Who the Players Are and How Money Flows

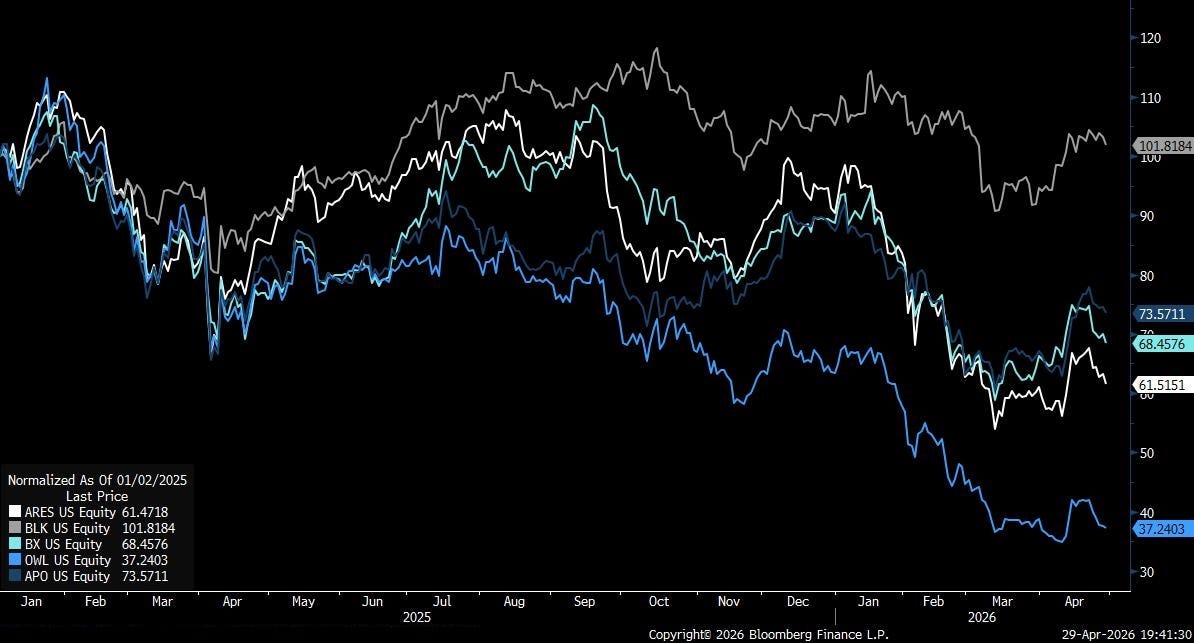

There is a tendency to treat private credit as a single pool of capital. It is better understood as a chain. At the centre sits a relatively concentrated group of managers. Some estimates state the top 10 US private debt managers hold roughly 40%–45% of industry dry powder4. That helps explain why public sentiment around the asset class often concentrates in a handful of listed names (Ares Management, Apollo Global Management, Blackstone, Blue Owl Capital, BlackRock) when software concerns or redemption fears spill into equity markets. A market that looks private at the asset level still has very public transmission channels.

Behind those managers sits the LP base. The classic closed-end private credit fund still draws most of its capital from institutional allocators: pension funds, insurers, sovereign wealth funds, family offices, and high-net-worth investors. Private credit investment funds represent about $800 billion of the US market and are typically structured so that LP capital is locked up until loans are repaid, often over five to seven years. The attraction is floating-rate income, diversification, and lower observed volatility than public bonds.

One example of this came during the March 2023 episode of banking stress and public credit market volatility, when an increasing number of large companies and their private equity sponsors preferred to borrow from private credit lenders, given the certainty of loan execution.

Then there are BDCs, which matter disproportionately because they bring retail capital into an otherwise opaque market. BDC assets are roughly $500 billion of the US private credit market. These companies must distribute at least 90% of income to shareholders, most of whom are retail and high-net-worth investors. Non-traded BDCs raise equity, pair it with leverage and then lend mainly to mid-sized companies, while offering investors periodic liquidity windows that are usually capped (5% per quarter). That makes BDCs both a funding channel and a pressure point, and they are one of the clearest ways for public market sentiment to force itself onto private credit.

At the borrower end, the ecosystem is dominated by sponsor-backed mid-sized companies using debt for buyouts, acquisitions, and refinancing. Increasingly, a meaningful share of those borrowers are in software or software-adjacent sectors. Around one-third of private credit funds have extended loans to SaaS firms, on top of their rising exposure to big US tech firms and other artificial intelligence (AI) companies, while another estimate measures broader direct lending to software and technology as around a fifth of total debt exposure. That is why the asset class cannot be properly analysed by talking about “middle market” in the abstract. Much of the collateral is actually exposure to a specific ownership model (private equity) and a specific business model (recurring-revenue software).

Even the risk is not fully warehoused outside the banking system. Activities and related risks of banks and private credit funds are intimately interwoven5, such that under an extreme economic scenario, stress in the private credit industry could affect the banking system. In some cases, banks now fund the funds, warehouse the leverage, or provide the lines and financing infrastructure around the loans rather than the loans themselves.

Why It Worked

Private credit’s golden decade was not an accident. It was built on an unusually powerful alignment of macro and market structure. The footprint of private credit is larger in countries with lower policy rates and more stringent banking regulation, and the post-GFC regulation accelerated banks’ retreat from smaller and riskier borrowers. When policy rates were low for years, and bank balance sheets became more selective, private credit could offer borrowers speed and certainty while offering investors incremental yield. It was exactly the right product for exactly the right regime.

The LP side of the story is just as important. Fundraising demand is explicitly linked to a period of historically low interest rates and the associated search for higher returns. Pension funds, insurers, and other institutional investors were drawn to an appeal of higher expected returns and lower observed volatility than public bonds. In plain English, ZIRP (zero interest rate policy) created a shortage of income, and private credit looked like a way to manufacture it without taking public-market mark-to-market pain.

The operating environment then helped the model look even better. Low default rates over most of the past decade reflected low interest rates, regular covenant monitoring, and the ability to renegotiate flexibly with a relatively small lender group when borrowers came under pressure. That last point is key. A small club of lenders can amend, extend, or restructure far more quietly than a dispersed public market. A period of cheap money, therefore, did not merely reduce defaults mechanically but also gave sponsors and lenders time and optionality.

There was also a structural pull from the public markets themselves. High-yield bonds and leveraged loans increasingly serve larger borrowers, with average new issue sizes often too large for most middle-market firms, while companies have stayed private for longer and private equity hold periods have lengthened. As private credit funds grew, their average fund sizes rose too, allowing them to write larger cheques and compete for bigger deals. The result was a natural expansion from a niche lender to undersized borrowers to a third major funding channel alongside banks and public credit markets.

Software was almost the perfect borrower for that world. From a lender’s perspective, the pitch was compelling: recurring revenue, sticky customers, high gross margins, low capital intensity, strong sponsor backing, and products embedded in enterprise workflows. The most resilient software businesses tend to be mission-critical systems of record with long sales cycles, proprietary data, and high switching costs. In a low-rate world, that translated into a seductive kind of collateral: businesses that felt more stable than cyclical industrials, cleaner than consumer names, and easier to value on growth plus retention metrics.

But this is where the regime has changed.

Pressure is already building in parts of the market, with lenders tightening terms and becoming more selective. AI makes software economics more contestable. Slower growth, longer sales cycles, pricing pressure, and weaker exit multiples do not need to produce instant insolvency to make a highly levered capital structure feel much tighter than it did under the assumptions of 2021.

The Bridge to the Fault Line

The danger in private credit is not usually that fundamentals deteriorate on a Tuesday and the market collapses on a Wednesday. It is that the signs of deterioration surface first in public proxies (BDC discounts, asset manager equities, software valuations) while the private loan book remains comparatively still. The mark lags the market, and the refinancing test arrives later. By the time a quarterly valuation fully admits the problem, the question of whether a borrower is weak is stale, and the new question is whether the system can still roll the loan on terms that preserve the illusion of stability.

Private credit repackaged credit risk into a slower-moving, more bespoke, less transparent form. That was enormously attractive in its golden age. There is no question about whether that model ever worked. It clearly did. The issue is whether a market built to look steady can stay steady once one of its favourite borrower cohorts starts repricing faster than the loans written against it.

This Is No GFC Call

The right way to frame this section is not “private credit will be the next 2008.” That’s too lazy, and it misses the shape of the problem. The more useful framing is that private credit is finally being tested in a new regime, and one that it never really had to underwrite for at scale: weaker software valuations, stickier refinancing risk, more sceptical investors, and public proxies that now move faster than private marks. There may be pain, contagion, and some losses, but that is not the same thing as saying the asset class is about to detonate into a system-wide event.

That said, the fact that this is probably not a classic banking crisis does not make it any less important. What changes the tone in 2026 is that regulators no longer treat private credit as a niche corner of the market. The US Securities and Exchange Commission (SEC) is explicitly warning that opacity, valuation, transparency, and credit quality matter amid elevated redemptions and rising default projections.

“The SEC is closely monitoring both the lending gap that private credit has filled and the emerging pressures that it has experienced, including elevated redemption requests and rising default-rate projections.”6

More so, the Bank of England (BOE) has launched a system-wide stress test to understand how banks, insurers, and non-banks active in private markets behave in a downturn. The European Central Bank (ECB) has begun flagging private credit as a financial stability concern. And the Financial Conduct Authority (FCA) has already warned that private markets require stronger valuation governance, as much depends on judgment rather than continuous price discovery.

Whether an asset class built on infrequent marks and patient capital can absorb a shock is a far more interesting debate than simply saying the whole thing explodes.

The Market Is Already Speaking

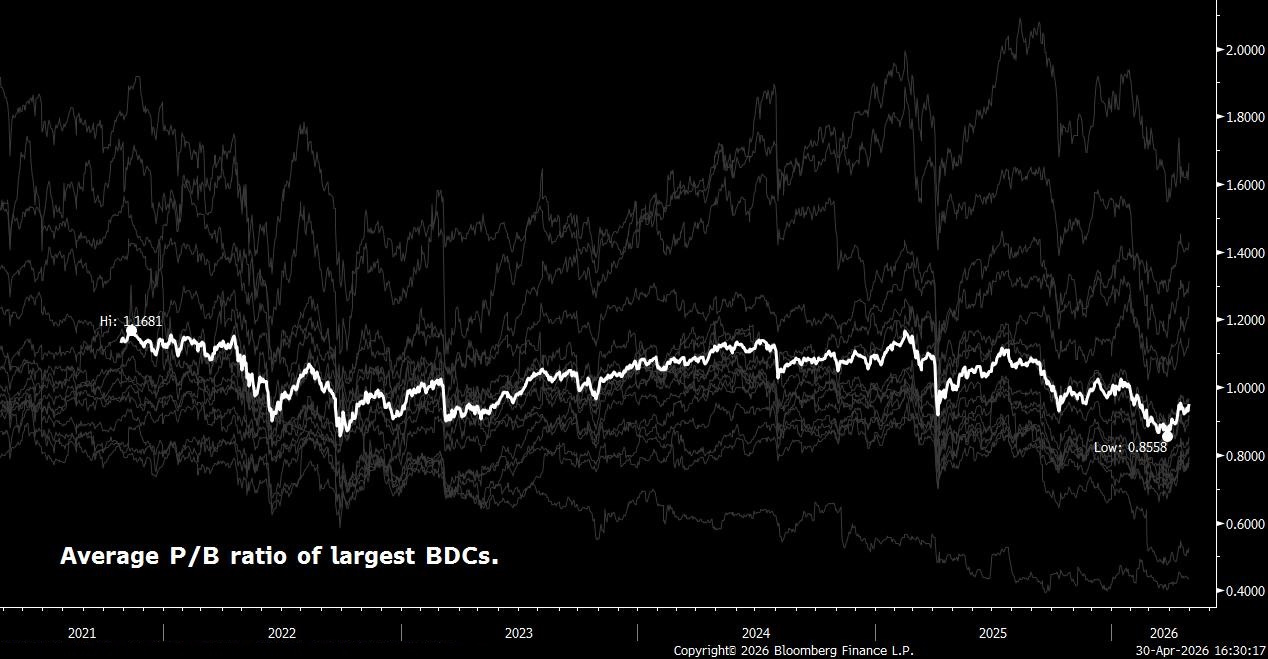

If you want to know where the stress is showing up first, don’t begin with default data. Begin with the public wrappers. Listed BDCs recently traded at their deepest discounts to net asset value in more than five years, with the average ratio around 0.856 at the end of March.

At the same time, Moody’s has shifted its outlook on US BDCs to negative, citing redemption pressure, higher leverage and weakening access to funding markets. That is all before you get to flows. Direct lending fundraising fell to $10.7 billion in the first quarter, the weakest quarterly number in three years, while new money into private credit funds aimed at wealthy individuals fell 45% year on year.

The loans themselves don’t trade every hour, but the equity around them does. So when investors have concerns, the first real price discovery happens in the discount to book and share prices of listed managers.

There is also a structural reason that this matters more now than it would have a decade ago. Some of the largest managers have made retail and high-net-worth fundraising a central growth engine, and some estimates put retail assets at around a quarter to two-fifths. A market that was sold as institutional and relatively insulated from mood swings becomes more exposed to investor behaviour. That in itself is not automatically dangerous. But it does mean that sentiment can now tighten conditions for the asset class even before credit losses force the issue.

Why Software Is the Pressure Point

The critical fault line is software, not because every software company is suddenly broken, but because private credit ended up with more software exposure than much of the rest of the sub-investment-grade universe.

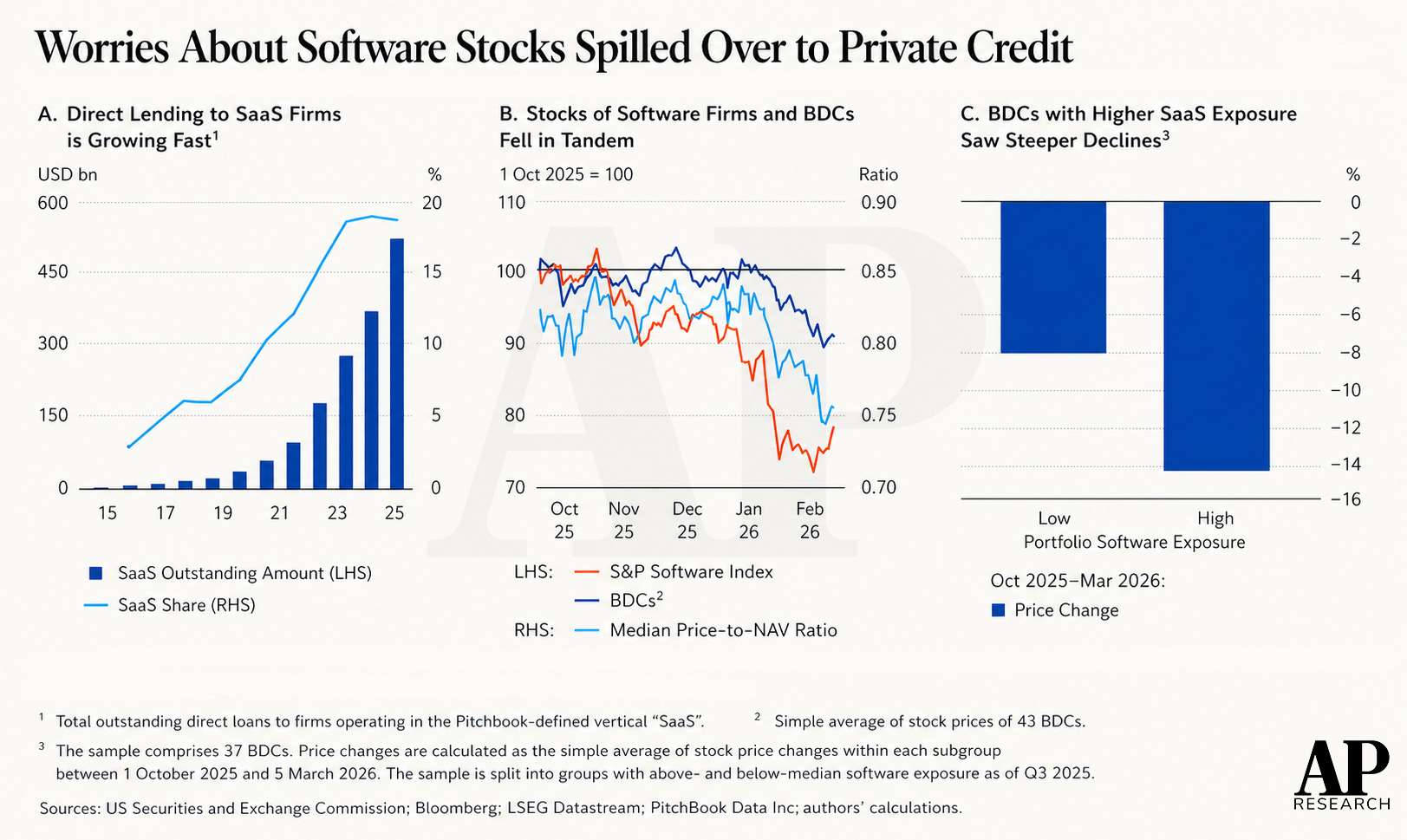

Lending by private credit funds to SaaS firms rose from almost $8 billion in 2015 to more than $500 billion by the end of 2025, equivalent to 19% of total direct loans (chart below). Even that may understate the true exposure, as classification can blur the picture. A software company selling into healthcare may be reported as healthcare exposure; one serving financial services may sit under financials. The result is that “software risk” is often larger than headline sector buckets suggest.

BDCs extended over 15% of their loans to SaaS firms in 2025, and firms with greater software exposure underperformed peers by around five percentage points last year. Analysis of more than 2,400 sponsor-backed middle-market borrowers shows software accounts for roughly 17% of borrowers and 22% of total debt exposure.

A concentration of that size was not irrational in the old regime because of the business model that software offered. But the same characteristics that made software look safe also encouraged aggressive underwriting. Much of direct lenders’ exposure to software originated at elevated valuations and leverage, and a meaningful slice consists of annual recurring revenue loans to companies with little or no positive free cash flow. Software-heavy deals have tended to cluster in the upper middle market, precisely where covenant protection and underwriting discipline have weakened the most.

The AI angle should also be kept in proportion. We do not buy into the interpretation that “AI kills software, therefore software kills private credit.” AI risk is likely to be diffuse and manageable overall, and most software-adjacent borrowers still have time and flexibility to adapt. But sponsor-backed borrowers with near-term maturities and structural exposure to disruption may come under real pressure. The risk falls in two channels: obsolescence, where customers build or buy cheaper functionality elsewhere, and margin compression, where incumbents have to spend more and price lower to defend their position.

This debate is no longer theoretical. In the week of publication, several of the largest private credit managers moved to reassure investors on this point. Ares, Blackstone and Blue Owl have begun running AI vulnerability reviews across their software books, using internal scorecards, external consultants, and refreshed underwriting work to separate potential beneficiaries from genuinely exposed borrowers. The message was deliberately calming (talk your book, so to speak). They state the risk is present, but most senior loans are presented as insulated, with only a limited share of exposures deemed high-risk. Blackstone said less than 5% of its flagship private credit fund investments faced AI headwinds, while Ares said 85% of its software-oriented investments were low risk and only 1% were high risk.

We would treat that as useful, but not conclusive. The exercise itself tells you the market has moved from abstract concern to active portfolio triage. The fact that managers are now producing AI scorecards is encouraging from a transparency perspective, but it also reinforces the broader point: software exposure is a meaningful risk. It is now something investors are actively trying to measure and stress-test.

Plumbing Matters More Than the Headline

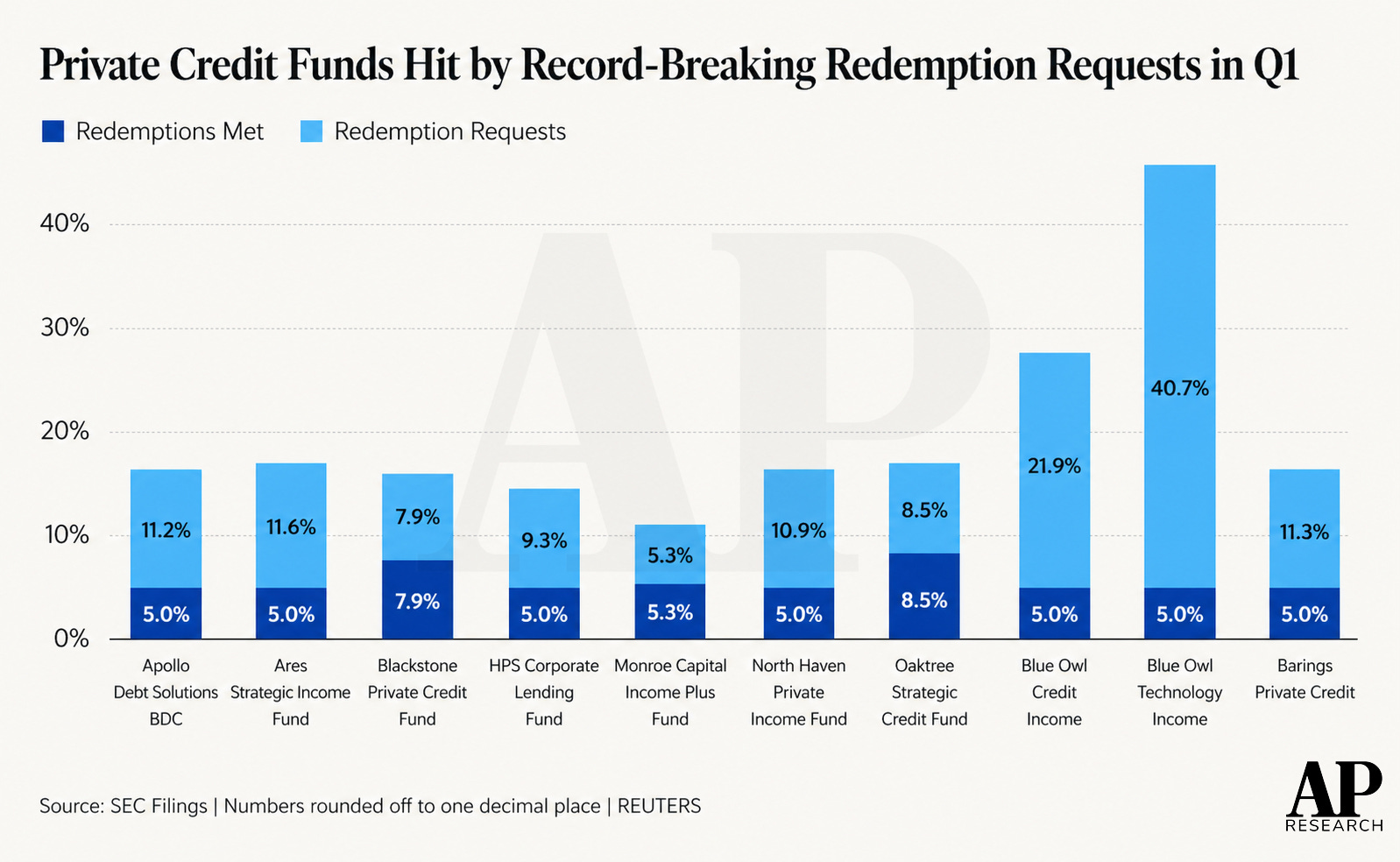

The next fault line is liquidity structure. Semi-liquid private credit vehicles generally offer quarterly repurchases capped at about 5% of NAV, and those limits are now being tested. Gates are not evidence of collapse so much as a contractual mechanism to manage cash flow when the underlying assets are less liquid and must be held to maturity. Private-loan drawdowns in stress are more a function of wider spreads than sudden fundamental impairment, and portfolio cash flows through 2025 still ran above standard quarterly and annual redemption maximums. Redemption limits appear to have worked as designed by reducing the risk of fire-sale liquidation in recent months.

But it would be a mistake to stop there and declare everything fine. Once investors learn that liquidity is conditional rather than instinctively available, and if that change in expectations persists, the consequence is not necessarily an immediate run. The feed-through would more likely be slower fundraising, more cautious deployment, and a higher hurdle for new money. That is already evident in the drop in retail-oriented fundraising and in the broader scepticism towards non-traded BDCs.

How the Stress Travels

The most plausible stress path is mechanical rather than dramatic. It begins with weaker software equity values and more uncertainty around terminal value. That makes sponsors less willing to support marginal borrowers, makes EBITDA add-backs look more heroic, and raises doubts around whether old marks still deserve to be carried where they are. Investors then express that doubt in the places they can actually trade: listed BDCs, alternative asset managers, public software equities and the financing exposures of banks to private credit funds. This first part is already underway. It would be hard for anyone to argue against that.

JPMorgan Chase has already re-marked some loans to private credit funds with software exposure, and banks have become tighter and more selective in lending against the sector.

The next stage (sorry if this is not sexy or doomer enough for a Substack post) is not a wave of defaults. It is a worsening in the refinancing environment. As this year’s market has shown, private credit funds can cap redemptions and avoid forced liquidation. But a manager facing slower inflows, scarcer warehouse financing, and more cautious investors will also be less eager to extend and support every marginal software name on borrower-friendly terms. That is where the public and private feedback loop begins. Discounts in listed vehicles raise the cost of equity, wider bond spreads raise the cost of liabilities, banks re-mark or tighten facilities, and the marginal borrower discovers that the old assumption of endless maturity extension was a feature of the previous regime, not a permanent right.

A Banking Spillover Looks Limited But Real

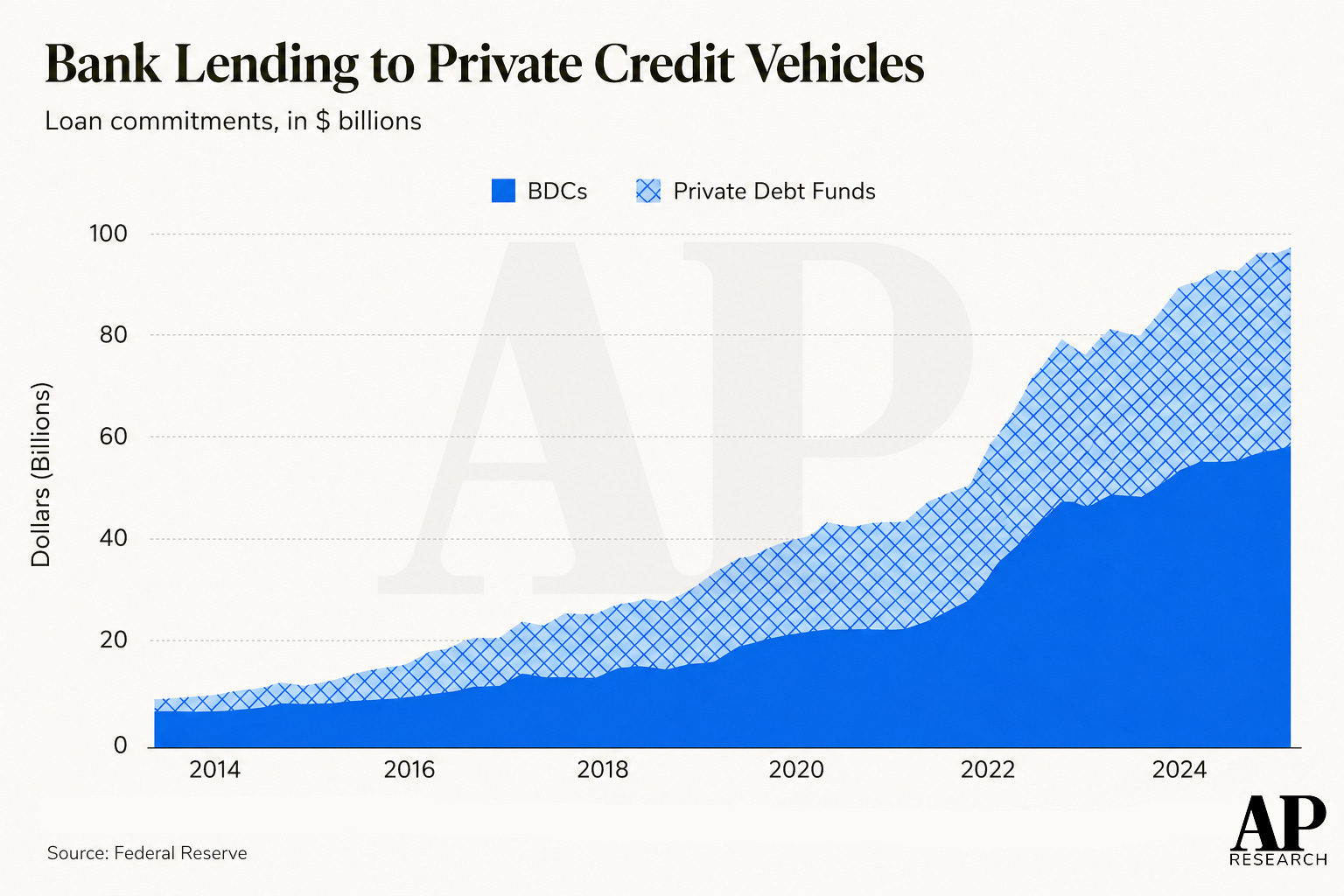

This is also where the “not 2008” point needs to be held carefully rather than used as a comfort blanket. Bank commitments to private credit vehicles rose from around $8 billion in 2013 to about $95 billion by late 2024, and to roughly $322 billion when private equity and private credit vehicles are combined. Financial-stability implications appear limited so far, as exposures remain relatively small and the credit quality of bank loans is high. As we discussed in the previous section, banks and non-banks are not separate but interwoven, with risks transformed and repackaged rather than cleanly migrating outside the system.

Recent headlines support this middle-ground view. The Fed has asked major banks for details on their exposure to private credit firms, and the Treasury is consulting insurance regulators about fund-level leverage, ratings consistency, and liquidity. Several regional banks have now disclosed more than $230 billion in loans to non-bank financial institutions while insisting their books remain sound. Regulators can clearly see the transmission channels: bank credit lines to funds, leverage against loan portfolios, insurer demand for credit risk, and the possibility that tighter conditions in one part of the ecosystem reduce credit supply elsewhere.

So is the right conclusion “contained, therefore harmless”? Probably not. The answer is more “contained for now, but increasingly relevant.”

What to Actually Worry About

Our base case is not a sudden unravelling, although that would make for a catchy title. We’ll likely see a wider gap between good and bad underwriting. The era of uniformly strong, low-dispersion direct lending returns to an end, with outcomes increasingly driven by manager quality and sector selection. The primary transmission of AI risk is likely to be greater differentiation in returns rather than a wholesale ratings event (there will be software winners from AI, too).

The bear case is still easy to sketch, however. If AI pressure on software coincides with a more general slowdown, the weak cohort is obvious. In that world, BDC discounts stay wide, unsecured funding costs travel higher, and sponsors triage portfolios more aggressively. Today’s valuation problem becomes tomorrow’s refinancing problem. And none of that requires a banking panic, just enough borrowers to discover that the private market will not keep extending time on yesterday’s assumptions.

That, to us, is the real fault line. Private credit has not abolished the credit cycle. It has concentrated the lender group and shifted risk into vehicles that appear calm until they are forced to explain themselves. Software and AI matter because they accelerate the repricing of one of the asset class’s favourite borrower cohorts. Private credit is not the next crisis, but whether it can remain stable enough once the repricing reaches the refinancing calendar remains to be seen.

If you enjoyed this dive into the world of private credit and the stress test markets are currently facing, please leave a like to show your support. As always, comments and opinions are welcome. If you want to read more primers, you can check out our library here.

AP Research

Federal Reserve Bank of New York (Oct-2025), https://tellerwindow.newyorkfed.org/2025/10/17/nbfis-in-focus-the-basics-of-private-credit/

BlackRock (Jan-2026), https://www.blackrock.com/gls-download/literature/market-commentary/private-credit-primer-january-2026.pdf

Sponsor “backing” refers to funds owning equity in these companies, typically through leveraged buyouts. Since sponsors control the equity in the firm, they are generally involved in making strategic decisions related to the company's management, operations, and capital structure.

This calculation is based on a 25-30% dry powder assumption and a 61% market share of US-based funds, which is sourced from Pitchbook.

Federal Reserve Bank of New York (Jun-2024), https://libertystreeteconomics.newyorkfed.org/2024/06/banks-and-nonbanks-are-not-separate-but-interwoven/

Keynote Remarks at The Economic Club of Washington (Apr-2026), https://www.sec.gov/newsroom/speeches-statements/atkins-keynote-remarks-economic-club-washington-042126

what a great read Boss!!

Great read!