Markets Run To Extremes

And they do so much more often than they theoretically should.

There is a reason markets run to extremes more often than coin flips.

Think back to financial crashes in history: The panic in 1907, the crash in 1929, Black Monday in 1987, LTCM’s fall in 1998, and the global financial crisis in 2008. Prior to each event, statisticians and risk managers would have said that they were impossible.

Yet, they happened.

Why does the “impossible” happen so frequently across market history?

The Bell Curve

A bell curve is a common type of distribution for a variable, also known as the normal distribution. The term “bell curve” originates from the fact that the graph used to depict a normal distribution consists of a symmetrical bell-shaped curve.

The highest point on the curve, or the top of the bell, represents the most probable event in a series of data (its mean, mode, and median in this case), while all other possible occurrences are symmetrically distributed around the mean, creating a downward-sloping curve on each side of the peak, known as the tail. The width of the bell curve is described by its standard deviation.

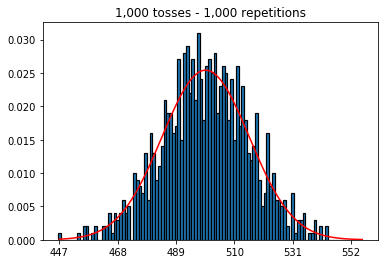

The easiest explanation can be given using a coin flip example. If you were to flip a coin 1,000 times and repeat this exercise 1,000 times, you would see a distribution of results similar to the one below.

The bell curve represents the normal distribution of outcomes and the corresponding probability density (on the y-axis). The x-axis measures the standard deviation from the average at zero. In this case, 500 is our zero (500 flips of heads and 500 of tails would be the standard).

If we increase the repetitions to 100,000, the data falls even more in line with the standard distribution (the bell curve).

Each coin flip is independent of the previous one. At every new coin flip, the probability is 50/50. You may flip heads five times in a row, but the probability of the sixth coin toss is still 50/50.

Therefore, the distribution of results will always fall as the above chart.

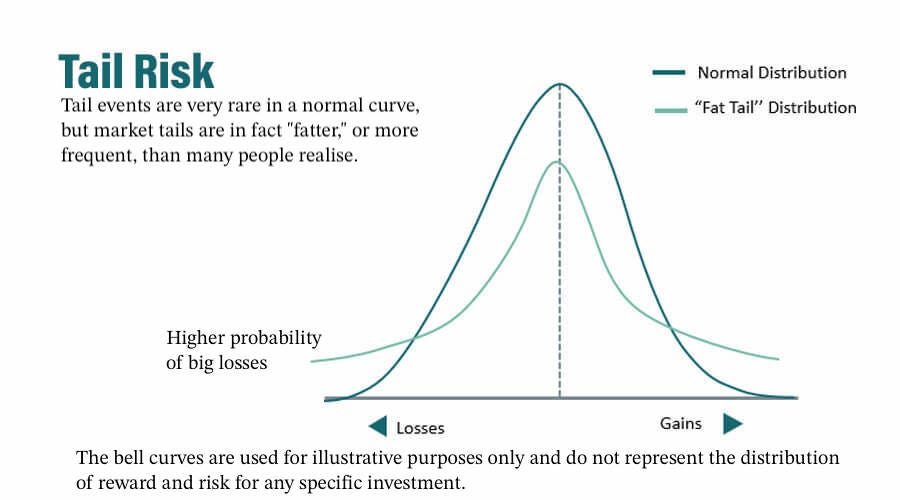

“Fatter” Tails

However, markets have memories. This causes the “impossible” to happen much more often.

Market tails will be fatter than normal bell curves. The unexpected is much more likely to happen than most realise.

In a normal probability distribution (blue curve), the odds of risky outcomes (bad stuff happening) are thin at the extremes. In fat-tailed distributions, such outcomes have a greater chance of occurring (the green curve).

Traditional portfolio strategies assume that market returns follow a normal distribution. However, the concept of tail risk suggests that the distribution of returns is not normal but skewed and has fatter tails.

The fat tails indicate that there is a probability, which may be larger than otherwise anticipated, that an investment will move beyond three standard deviations. Distributions that are characterised by fat tails are often seen when looking at hedge fund returns, for example.

When a portfolio of investments is put together, it is assumed that the distribution of returns will follow a normal distribution. Under this assumption, the probability that returns will move between the mean and three standard deviations, either positive or negative, is approximately 99.7%. This means that the probability of returns moving more than three standard deviations beyond the mean is 0.3%.

Why Consider This?

The assumption that market returns follow a normal distribution is key to many financial models, such as Harry Markowitz’s modern portfolio theory (MPT)1 and the Black-Scholes-Merton option2 pricing model. However, this assumption does not properly reflect market returns and tail events have a large effect on them.

It’s something to keep in mind, not necessarily for your own portfolio, but for the bigger picture.

When markets start to run to the extremes, it is easy to think to yourself, “Surely, the trend will change soon.”

Just this month, the S&P 500 had eight green days in a row. That nears a record stretch. However, as we learned earlier, markets are independent of random results because they have memories. Just because you have had eight “flips” going one way doesn’t mean the next flip is more likely to be different.

After three “bad” or “good” flips in the market, the fourth flip may no longer be completely random.

Sometimes, a trend will continue just because traders expect (or fear) that it will. Investors will follow a trend for no other reason than that they think enough others will do likewise.

Momentum trading has nothing to do with logically appraising securities. It doesn’t fit the ideal of rational investors in efficient markets.

But it’s human.

https://www.math.hkust.edu.hk/~maykwok/courses/ma362/07F/markowitz_JF.pdf

https://www.cs.princeton.edu/courses/archive/fall09/cos323/papers/black_scholes73.pdf

I try to look for a symmetric trades that benefit from ignoring tail risks.

It also serves as a hedge for my portfolio.

For example, I bought a out of the money put debit spread on SPY with a risk reward of 15 to 1. Looking at market returns, the probability is about 17%.

It's what Nassim Nicholas Taleb calls Antifragile, things that gain from disorder. I wrote a post about it.

Nice write-up. Financial markets always overshoots on expectation basis. That's how the term 'Buy on Rumour, Sell on Fact' came about.