There are few cleaner signals that a market is cheap than when outsiders start buying it.

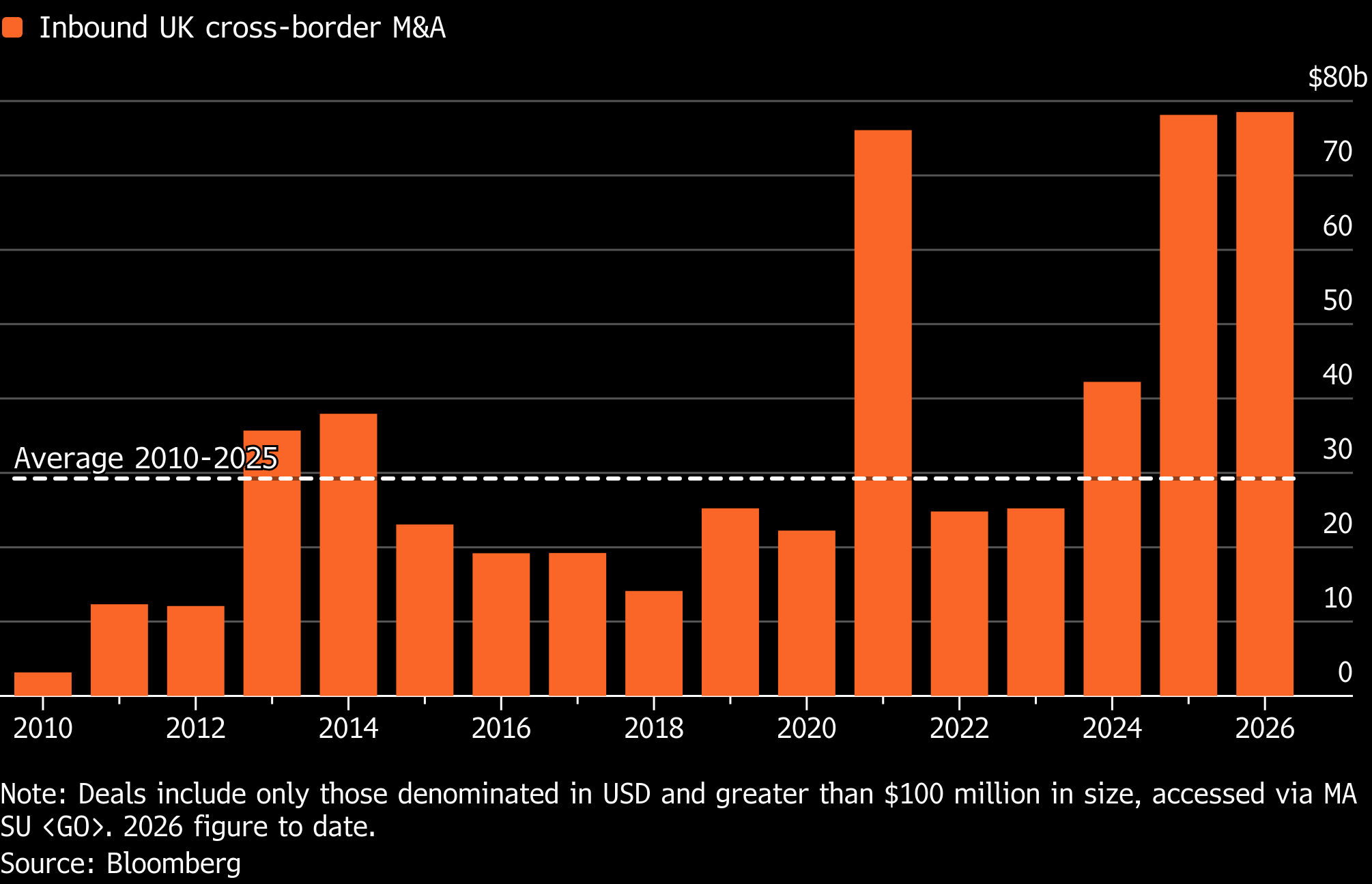

That is increasingly the story in our home base of the UK. For years, the equity market has been described in the language of polite dismissal: too old-economy, too low-growth, too politically messy, too easy to ignore. But neglect has a habit of creating value. British takeovers are up 250% year-on-year, with overseas buyers rediscovering that one of the most unloved corners of global equities still contains real assets, cash flows, brands, and strategic value that public markets have been reluctant to price properly.

EasyJet (EZJ LN) is the latest example from our Master Fund of that cheapness being tested in public. Castlelake, the US investment firm, made a series of approaches for the airline, initially at levels the board rejected as opportunistic and undervaluing the group. On Monday, however, easyJet agreed in principle to a sweetened 690p-per-share offer, a meaningful premium to the prevailing 603p share price.

The market had already started to close the gap. EasyJet shares have risen almost 100% over the past two months as investors have gradually come around to the value proposition. At the beginning of June, Citi argued that the airline’s fleet alone could be worth double the share price. When the aeroplanes are worth more than the equity market’s view of the company, maybe it’s not such a surprise when a financial buyer starts circling.

There is also a wider macro footnote here. The strength of inbound UK M&A may help explain one of the more surprising moves in FX this year: sterling’s resilience. The pound has had to digest geopolitics, domestic political noise, and shifting rate expectations, yet it has remained one of the better performers in G10. Deal flow will never dominate a market as deep as sterling, where daily turnover dwarfs even the largest transactions. But cross-border acquisitions do create real currency demand, hedging flows, and corporate activity.

With the bulk of the profit from our easyJet long position now locked in, the focus turns to sniffing around for other cheap UK purchases that could be ripe for a move higher.

Why the UK Remains Attractive

Before moving into the more speculative part of the exercise (which UK-listed companies might be next?), it is worth stepping back and asking why the bid for UK assets has returned at all.

There are three reasons private equity firms and overseas strategics keep circling London: the valuation gap remains wide, the domestic buyer base has withered, and the market is full of cash-generative companies that public investors have deemed too unfashionable to own.

The UK is cheap for reasons that are both structural and self-reinforcing. The market has the wrong sector mix for the current cycle, too little technology, too much exposure to banks, energy, staples and healthcare, and a domestic investor base that has spent decades walking away. Although the discount has become embedded, it does not mean it is justified.

The Valuation Gap Remains Wide

Start with the obvious point. UK equities are still cheap. The FTSE 100 trades on roughly 16x earnings, compared with 27.7x for the S&P 500, and remains at a discount to most European and Asian markets as well. Some of that discount is deserved. The UK does not have the same technology weighting as the US, nor the same earnings momentum from AI. But the size and persistence of the discount has created a clear arbitrage for strategic buyers.

For public-market investors, a UK-listed company can remain cheap forever. For a buyer with a longer time horizon, a balance sheet and a willingness to act, that same company becomes something different: a decent global asset trading at a local-market discount.

That is the essential appeal. Buy real assets in London at UK multiples, then own them privately, restructure them, or fold them into a larger global group where the same cash flows may be valued more generously.

Domestic Ownership Has Collapsed

The second issue is ownership. The UK market no longer has a strong domestic buyer standing behind it. Pension fund allocation to UK equities has fallen from more than 50% around 25 years ago to roughly 4.4% today. LSEG has estimated that more than £1.9tn has exited UK equities since 2000 as pension funds and wealth managers shifted capital toward global markets, especially the US.

Valuation is not only about earnings. It is also about who is willing to take ownership of those earnings.

The answer in the UK has been “not enough people.” Persistent domestic selling has kept valuations depressed, liquidity thin in parts of the market, and boards more exposed when a credible bidder turns up offering a 30–40% premium.

London Is Cash-Generative But Unfashionable

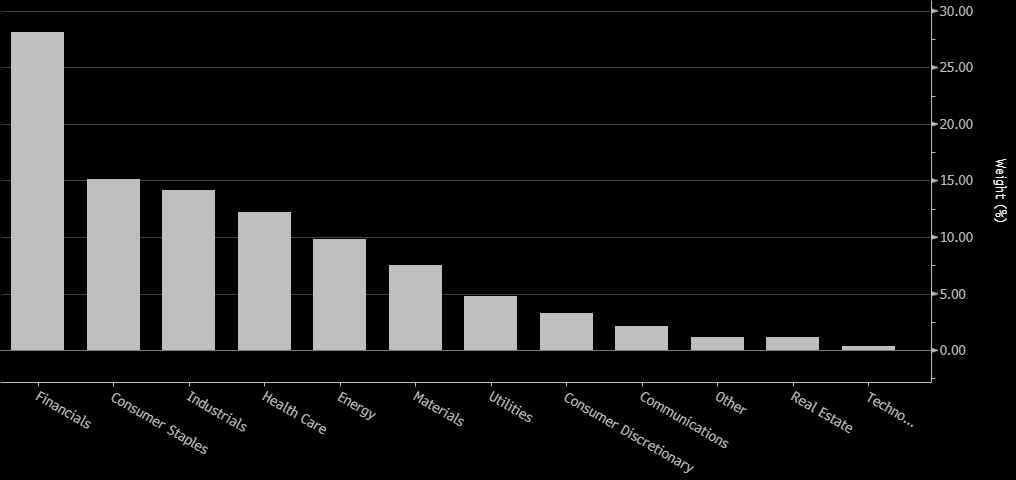

Third is composition. The UK’s discount is not a mystery. The market looks the way it does because of what it owns. The FTSE 100 is roughly 28.1% financials, 15.1% consumer staples, 14.2% industrials, 12.2% healthcare, 9.8% energy, and only about 0.4% technology.

That is almost the opposite of what global investors have wanted to own over the last decade. The FTSE 100 is dominated by banks, miners, insurers, energy companies, consumer staples, and healthcare names rather than Big Tech, software platforms, or AI infrastructure winners. A market built this way can look optically cheap for a very long time.

But that is also why it keeps attracting buyers.

For public investors chasing growth and narrative, many UK-listed companies look dull. For private equity firms and overseas corporates, “dull” can be another word for “useful”. These businesses often have real assets, steady cash flows, defensible market positions, and underappreciated strategic value. They may not deserve US-style multiples, but they don’t need to. When the starting valuation is low enough, the upside can come from someone else deciding the asset is worth more than the London market is willing to pay.